Asian Market's Top 3 Undervalued Small Caps With Insider Action

Reviewed by Simply Wall St

As global markets navigate through a period of economic uncertainty, Asian small-cap stocks present intriguing opportunities amidst broader market volatility. With key indices like the S&P MidCap 400 and Russell 2000 experiencing fluctuations, investors may find potential in identifying stocks that exhibit strong fundamentals and insider activity, suggesting confidence in their future prospects.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Infomedia | 32.0x | 3.6x | 34.80% | ★★★★★★ |

| Security Bank | 5.3x | 1.2x | 32.03% | ★★★★★☆ |

| Puregold Price Club | 9.0x | 0.4x | 25.55% | ★★★★★☆ |

| Autosports Group | 10.3x | 0.1x | 27.68% | ★★★★★☆ |

| Champion Iron | 19.6x | 1.7x | 41.20% | ★★★★☆☆ |

| Dicker Data | 19.0x | 0.7x | -22.40% | ★★★☆☆☆ |

| Fenix Resources | 15.4x | 0.8x | 15.77% | ★★★☆☆☆ |

| Yixin Group | 9.1x | 0.9x | -279.13% | ★★★☆☆☆ |

| HBM Holdings | 22.9x | 6.7x | 0.78% | ★★★☆☆☆ |

| Tabcorp Holdings | NA | 0.7x | -42.51% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

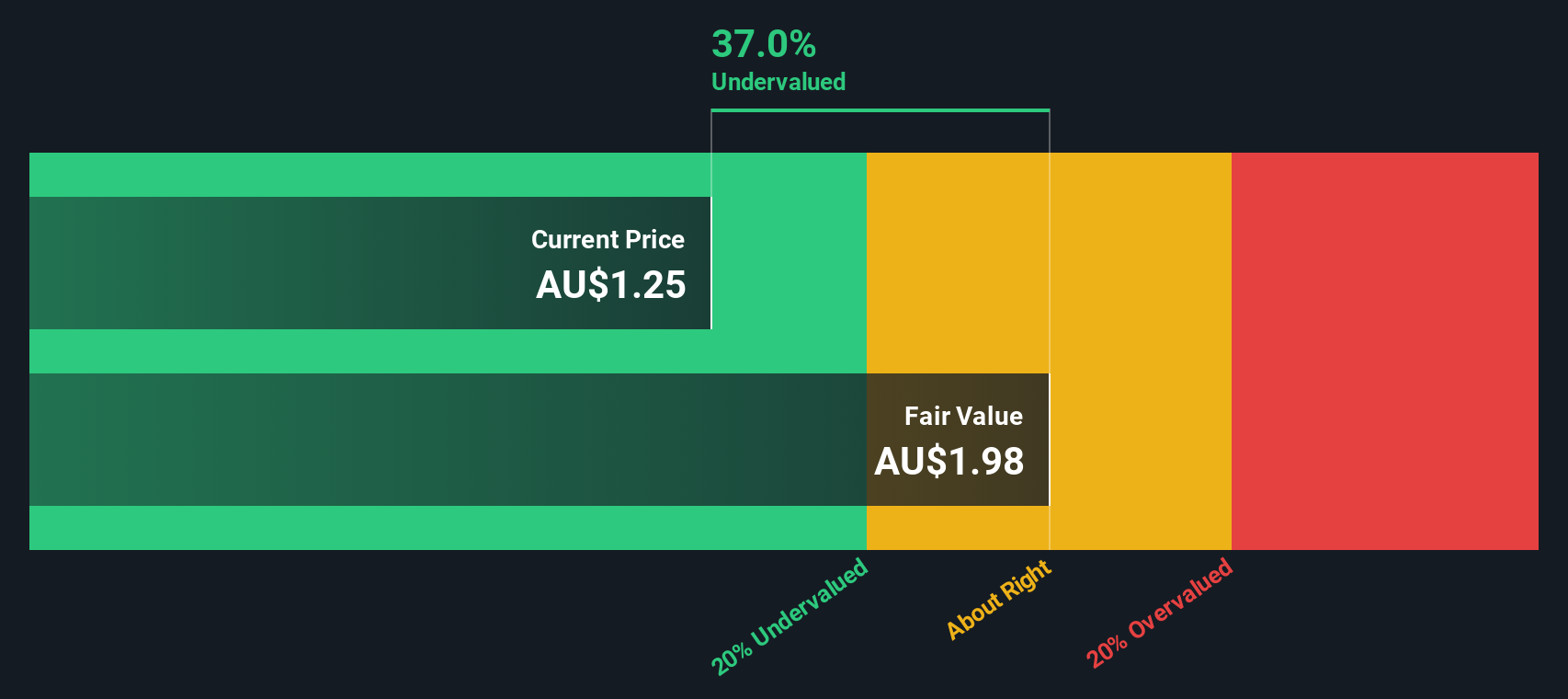

FleetPartners Group (ASX:FPR)

Simply Wall St Value Rating: ★★★★★★

Overview: FleetPartners Group is a company that specializes in vehicle leasing and fleet management services, with a market capitalization of A$1.2 billion.

Operations: FleetPartners Group derives its revenue primarily from its core operations, with a notable focus on managing costs. The company's gross profit margin showed an upward trend initially, reaching 42.28% by September 2017 before experiencing fluctuations and settling at 29.20% by March 2025. Operating expenses have been a significant component of the cost structure, with general and administrative expenses consistently being the largest portion within this category over time.

PE: 7.3x

FleetPartners Group, a small cap in Asia, is navigating financial challenges with its reliance on external borrowing, making it riskier compared to firms with customer deposits. Despite this, insider confidence is evident as they purchased shares from October 2024 to January 2025. The company has extended its buyback plan until March 31, 2025. However, earnings are expected to decline by an average of 5.2% annually over the next three years.

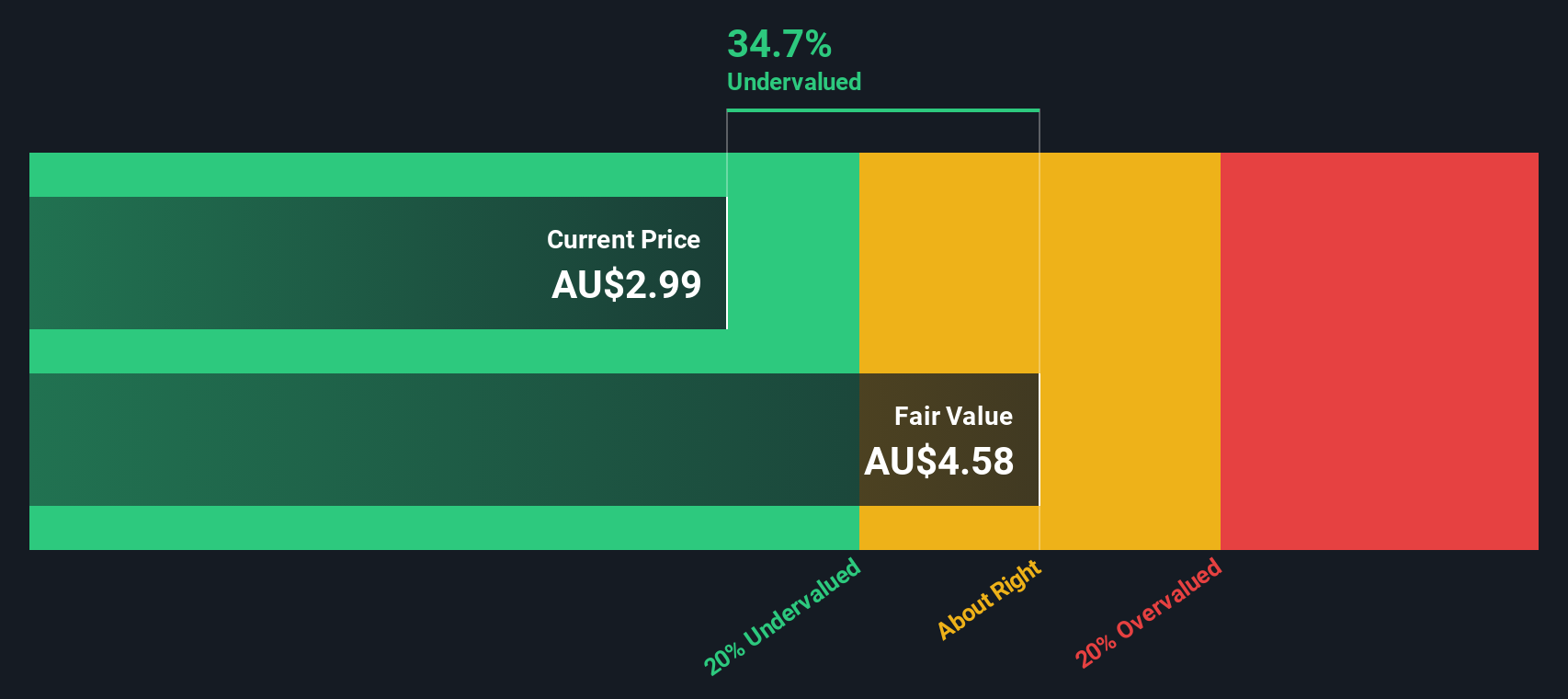

Infomedia (ASX:IFM)

Simply Wall St Value Rating: ★★★★★★

Overview: Infomedia is a company specializing in the publishing of periodicals, with operations generating A$142.41 million in revenue.

Operations: The company generates revenue primarily from publishing periodicals, with a reported revenue of A$142.41 million in the latest period. Operating expenses are significant, with general and administrative costs being a major component at A$71.36 million. The net income margin shows variability, reaching 11.16% recently, reflecting changes in profitability over time.

PE: 32.0x

Infomedia, a small cap in Asia, shows potential with earnings expected to grow 21.17% annually. Despite relying on external borrowing for funding, the company reported an increase in net income to A$8.33 million for the half year ending December 31, 2024. Insider confidence is evident from recent share repurchase plans announced on February 18, 2025, aiming to buy back up to 18.79 million shares by March 2, 2026. This strategic move could enhance shareholder value amidst its ongoing growth trajectory and acquisition discussions with Intellegam GmbH.

- Dive into the specifics of Infomedia here with our thorough valuation report.

Explore historical data to track Infomedia's performance over time in our Past section.

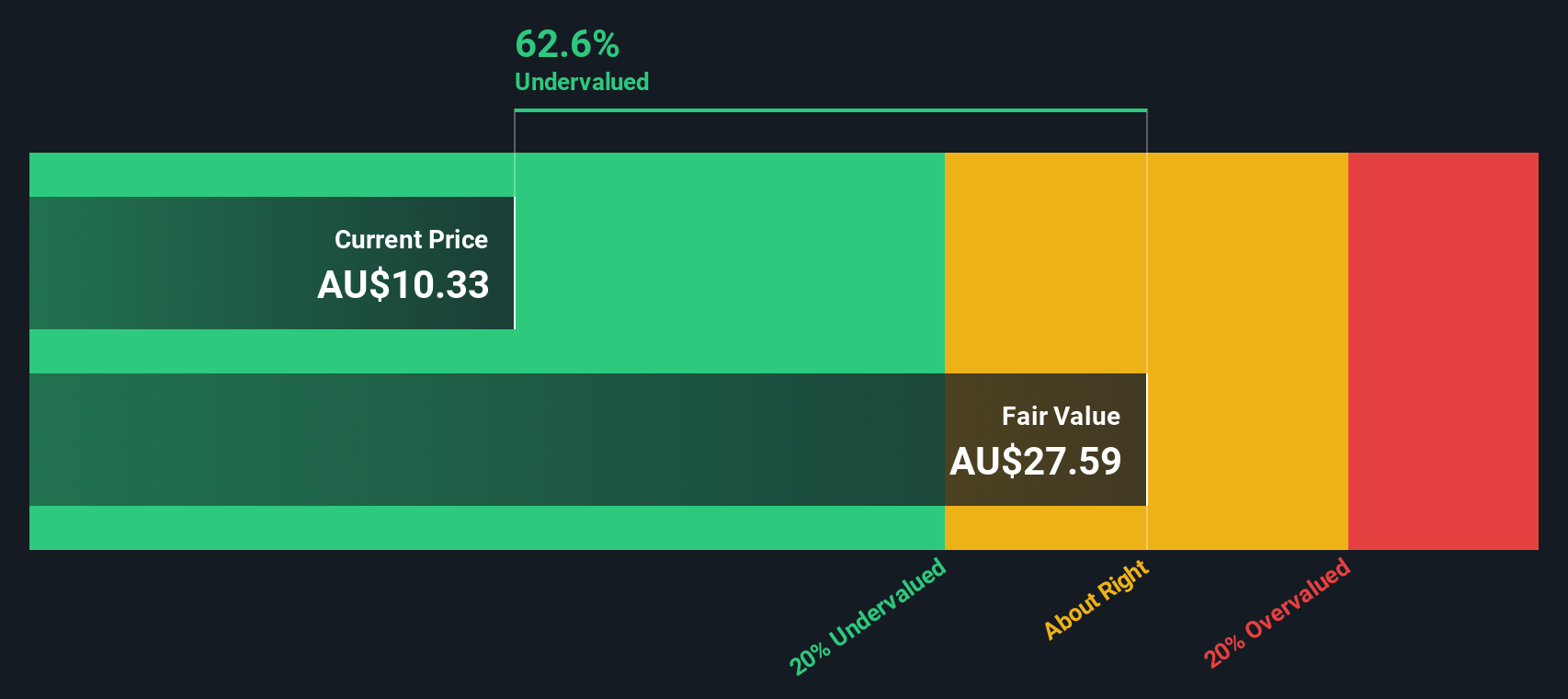

Jumbo Interactive (ASX:JIN)

Simply Wall St Value Rating: ★★★★★★

Overview: Jumbo Interactive is a company that operates in the lottery industry, providing services such as managed services, lottery retailing, and software-as-a-service (SaaS), with a focus on digital platforms; it has a market capitalization of A$1.31 billion.

Operations: Jumbo Interactive generates revenue primarily from Lottery Retailing (A$116.31 million), Managed Services (A$25.10 million), and Software-As-A-Service (SaaS) offerings (A$47.86 million). The company's gross profit margin has shown a decreasing trend, reaching 80.36% as of December 2024, while its net income margin was 27.08% in the same period.

PE: 17.4x

Jumbo Interactive, a player in the Asian small-cap space, is navigating through a period of strategic realignment. With an eye on acquisitions and investments, they're targeting B2C opportunities for growth. Despite reporting lower sales (A$66.13 million) and net income (A$17.86 million) for H1 2025 compared to last year, insider confidence is evident as founder Mike Veverka acquired 6,900 shares worth A$94,813 in February 2025. The company also maintains flexibility with its balance sheet while managing risks associated with external funding sources.

- Get an in-depth perspective on Jumbo Interactive's performance by reading our valuation report here.

Evaluate Jumbo Interactive's historical performance by accessing our past performance report.

Next Steps

- Access the full spectrum of 41 Undervalued Asian Small Caps With Insider Buying by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:IFM

Infomedia

A technology company, develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide.

Very undervalued with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives