As the Australian market enjoys a positive upswing with the ASX200 reaching a seven-week high, investors are buoyed by favorable trade outcomes and strategic AI investments. In this environment of optimism, discovering promising small-cap stocks that align with current trends in IT and Industrials can offer intriguing opportunities for those seeking to explore Australia's undiscovered gems.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 9.94% | 6.48% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Bisalloy Steel Group | 0.95% | 10.27% | 24.14% | ★★★★★★ |

| Lycopodium | NA | 17.22% | 33.85% | ★★★★★★ |

| Djerriwarrh Investments | 1.14% | 8.17% | 7.54% | ★★★★★★ |

| Red Hill Minerals | NA | 75.05% | 36.74% | ★★★★★★ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| AMCIL | NA | 5.16% | 5.31% | ★★★★★☆ |

| K&S | 16.07% | 0.09% | 33.40% | ★★★★☆☆ |

| Hearts and Minds Investments | 1.00% | 18.81% | 20.95% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Cuscal (ASX:CCL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cuscal Limited, along with its subsidiaries, offers payment and regulated data products and services to financial and consumer-focused institutions in Australia, with a market cap of A$503.81 million.

Operations: Cuscal generates revenue through its payment and regulated data services tailored for financial and consumer-focused institutions in Australia. The company has a market cap of A$503.81 million.

Cuscal, a financial services company in Australia, has recently completed an IPO raising A$336.8 million, offering 134.7 million shares at A$2.5 each with a slight discount per security. The company's earnings have grown by 21% over the past year and are expected to continue growing at 12% annually, which is impressive given its industry context where growth is lagging behind. Despite having high-quality past earnings and a reduced debt-to-equity ratio from 172.5% to 103.5% over five years, Cuscal's interest payments are not well covered by EBIT (1.4x coverage), indicating potential challenges in managing debt obligations effectively.

- Take a closer look at Cuscal's potential here in our health report.

Understand Cuscal's track record by examining our Past report.

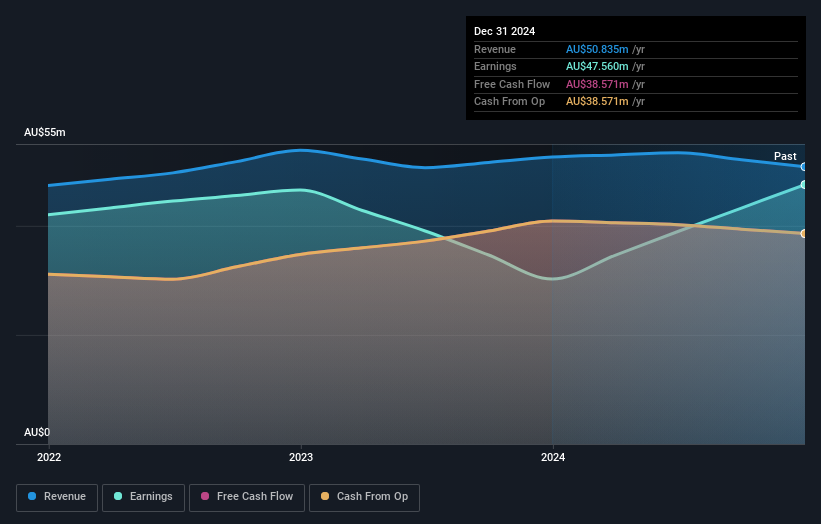

Djerriwarrh Investments (ASX:DJW)

Simply Wall St Value Rating: ★★★★★★

Overview: Djerriwarrh Investments Limited is a publicly owned investment manager with a market capitalization of A$843.89 million.

Operations: Djerriwarrh Investments generates revenue primarily from its portfolio of investments, totaling A$50.84 million.

Djerriwarrh Investments, a notable player in the Australian market, showcases robust financial health with its debt-to-equity ratio dropping from 9.7 to 1.1 over five years and earnings growth of 57% outpacing the industry average of 17%. The firm’s price-to-earnings ratio stands at a competitive 17.7x compared to the broader market's 19.3x, indicating potential value for investors. With interest payments well covered by EBIT at a multiple of 21 and recent dividend affirmations maintaining shareholder confidence, Djerriwarrh seems well-positioned within its sector despite not being widely recognized as an investment gem.

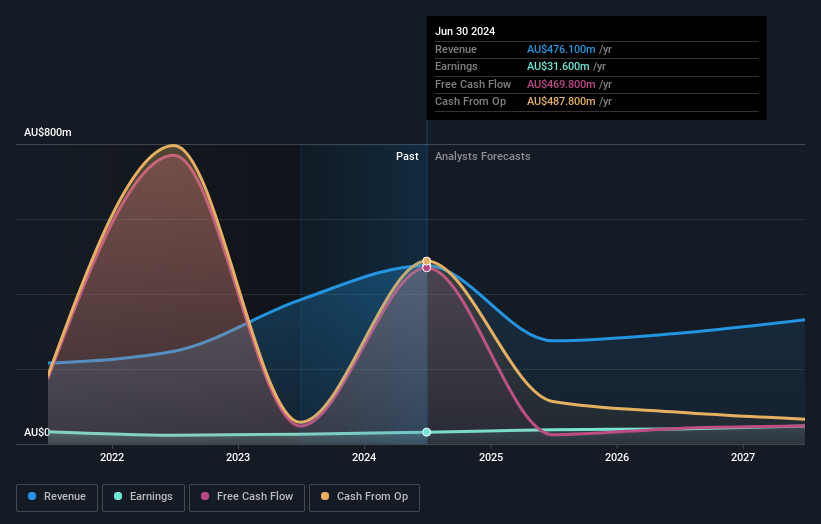

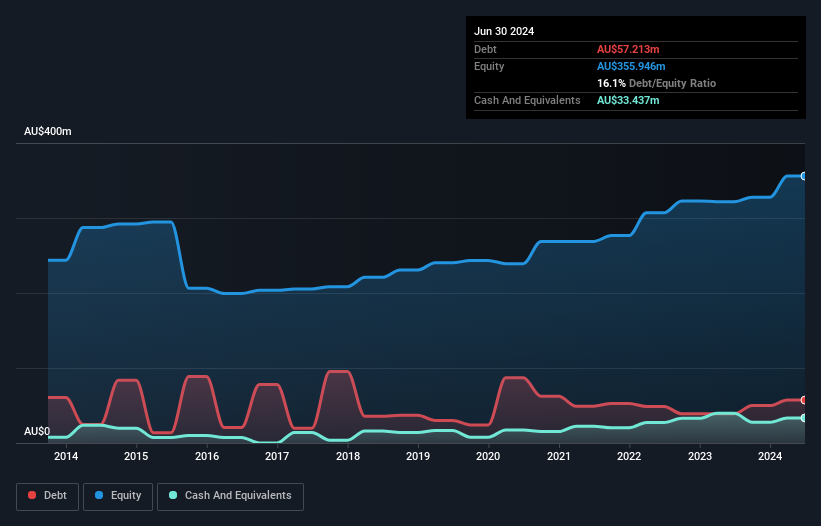

K&S (ASX:KSC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: K&S Corporation Limited operates in the transportation, logistics, warehousing, and fuel distribution sectors across Australia and New Zealand, with a market capitalization of approximately A$492.66 million.

Operations: K&S generates revenue primarily from its Australian transport segment at A$582.80 million, followed by fuel distribution at A$230.79 million, and New Zealand transport at A$72.93 million.

K&S, a notable player in the logistics sector, showcases robust financial health with its interest payments well covered by EBIT at 10.2 times. Over the past year, earnings grew by 9.1%, outpacing the broader logistics industry which saw a -7% change. Despite an increase in debt to equity from 12.5% to 16.1% over five years, their net debt to equity ratio remains satisfactory at 6.7%. Trading at A$12.9 below its estimated fair value suggests potential undervaluation, though free cash flow isn't positive currently, highlighting areas for improvement amidst high-quality earnings performance.

- Click here to discover the nuances of K&S with our detailed analytical health report.

Examine K&S' past performance report to understand how it has performed in the past.

Make It Happen

- Discover the full array of 51 ASX Undiscovered Gems With Strong Fundamentals right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if K&S might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:KSC

K&S

Engages in the transportation and logistics, warehousing and fuel distribution businesses in Australia and New Zealand.

Proven track record with adequate balance sheet.