Advertisement

- Australia

- /

- Hospitality

- /

- ASX:FLT

Asian Market's Top 3 Undervalued Small Caps With Insider Action

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with inflation concerns and trade uncertainties, Asian small-cap stocks present a compelling area of interest, particularly as these companies often demonstrate resilience and growth potential in dynamic economic environments. In this context, identifying small-cap stocks that exhibit strong fundamentals and insider activity can provide valuable insights into opportunities within the Asian market.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.7x | 1.1x | 32.17% | ★★★★★★ |

| Atturra | 26.6x | 1.1x | 42.18% | ★★★★★☆ |

| Hansen Technologies | 282.9x | 2.7x | 28.34% | ★★★★★☆ |

| Viva Energy Group | NA | 0.1x | 21.62% | ★★★★★☆ |

| Hong Leong Asia | 9.1x | 0.2x | 45.50% | ★★★★☆☆ |

| Dicker Data | 19.5x | 0.7x | -46.57% | ★★★★☆☆ |

| Sing Investments & Finance | 7.3x | 3.7x | 36.22% | ★★★★☆☆ |

| Collins Foods | 20.0x | 0.7x | -2.01% | ★★★☆☆☆ |

| Integral Diagnostics | 154.9x | 1.8x | 40.97% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.6x | 39.72% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

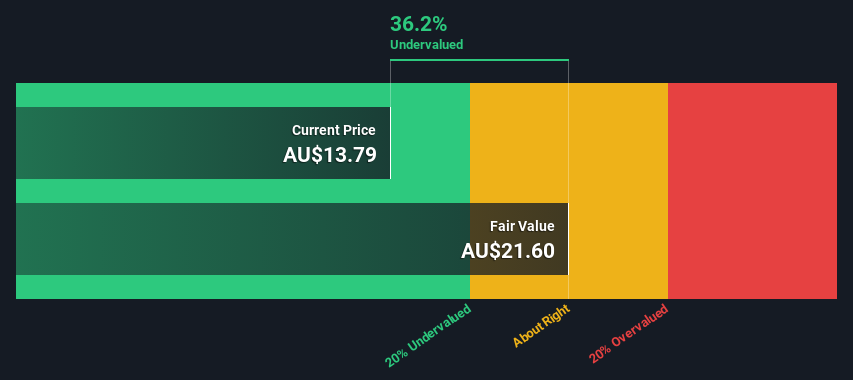

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Flight Centre Travel Group is a global travel agency company that operates through its leisure, corporate, and other travel services segments with a market capitalization of A$4.5 billion.

Operations: The company generates revenue primarily from its Leisure and Corporate segments, with the Leisure segment contributing A$1.38 billion and the Corporate segment A$1.13 billion. Over recent periods, gross profit margin has shown a gradual improvement, reaching 43.20% by December 2024. Operating expenses include significant allocations to sales and marketing as well as general and administrative functions, impacting overall profitability.

PE: 27.6x

Flight Centre Travel Group, a smaller player in the Asian market, shows potential as an undervalued stock. Recent insider confidence is evident with share purchases over the past six months. Despite a dip in net income to A$60.47 million for the half-year ending December 2024, sales increased slightly to A$1.33 billion from A$1.29 billion year-over-year. The company announced a dividend of A$0.11 per share, reflecting steady shareholder returns amidst external borrowing challenges and growth forecasts of 23% annually.

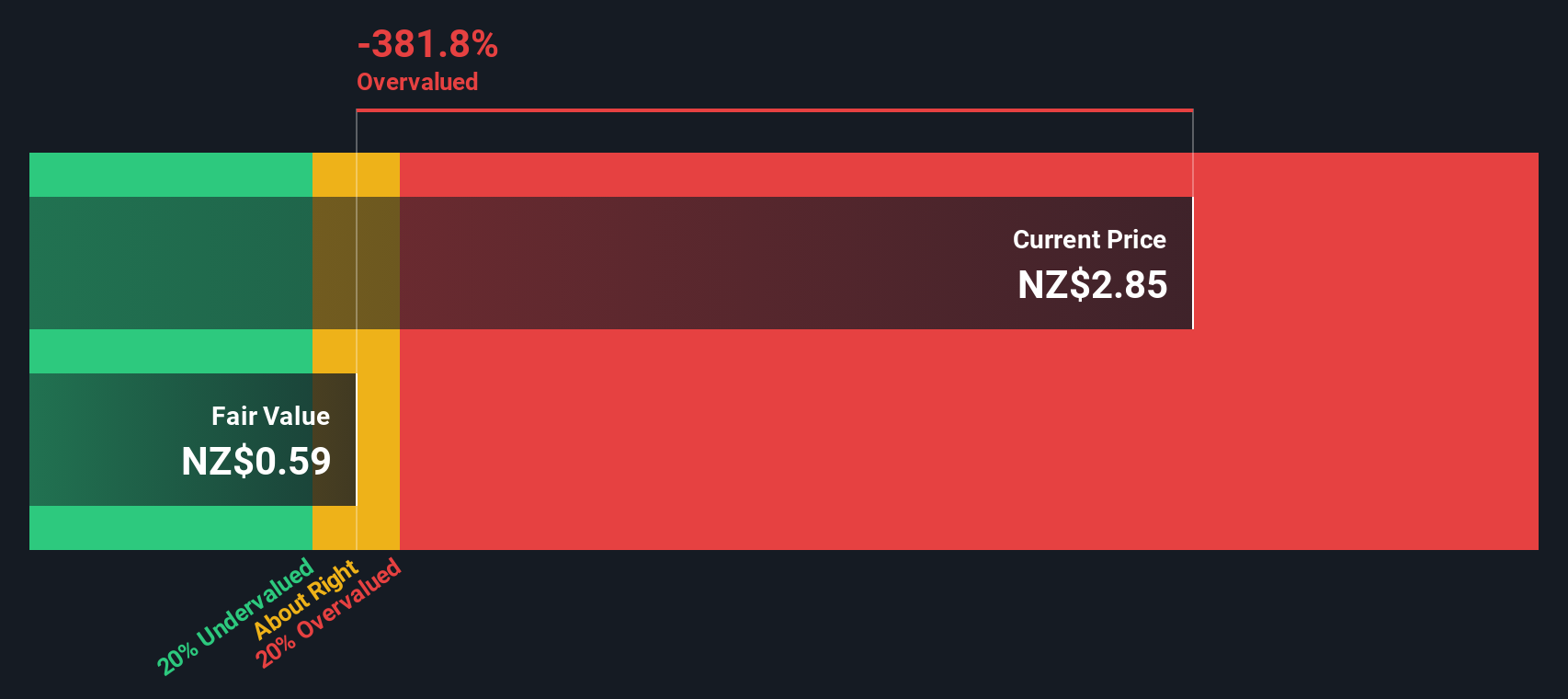

Ryman Healthcare (NZSE:RYM)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Ryman Healthcare operates integrated retirement villages for older people and has a market cap of approximately NZ$5.86 billion.

Operations: Ryman Healthcare's primary revenue stream is derived from the provision of integrated retirement villages, with recent revenue reaching NZ$720.35 million. The company's gross profit margin has seen a decline over time, standing at 2.37% in the latest period. Operating expenses and non-operating expenses have significantly impacted net income, resulting in a net loss of NZ$87.94 million for the same period.

PE: -21.8x

Ryman Healthcare, a prominent player in the healthcare sector, recently completed a follow-on equity offering worth NZ$1 billion. Despite its high debt levels and reliance on external borrowing, the company anticipates earnings growth of 35% annually. Insider confidence is evident with recent share purchases, suggesting optimism about future prospects. The stock's volatility over the past three months contrasts with its potential for growth amidst strategic financial maneuvers aimed at stabilizing and expanding operations.

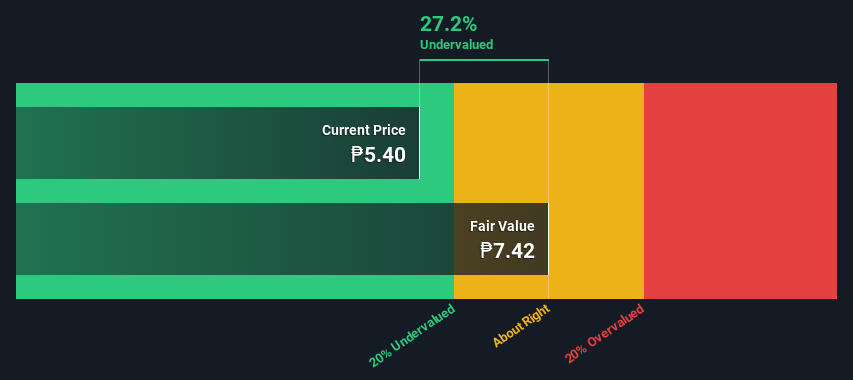

D&L Industries (PSE:DNL)

Simply Wall St Value Rating: ★★★★☆☆

Overview: D&L Industries is a diversified manufacturer specializing in food ingredients, oleochemicals, and specialty plastics with a market capitalization of approximately ₱62.42 billion.

Operations: D&L Industries generates revenue primarily through its operations with a notable focus on managing costs, as evidenced by the cost of goods sold (COGS) consistently comprising a significant portion of expenses. Over recent periods, the company's gross profit margin has shown variability, peaking at 21.39% in Q3 2019 and more recently at 17.33% in Q3 2023. Operating expenses include sales and marketing as well as general and administrative costs, which together reflect strategic investments to support business activities.

PE: 16.5x

D&L Industries, a small company in Asia, recently reported significant growth with 2024 sales reaching PHP 40.6 billion from PHP 33.4 billion the previous year, and net income rising to PHP 2.3 billion. Demonstrating insider confidence, Co-Founder Dean Lao purchased 100,000 shares valued at approximately ₱630K in early March 2025. While reliant on external borrowing for funding, D&L's earnings are projected to grow by over 13% annually, indicating potential for future expansion despite its current financial structure challenges.

- Take a closer look at D&L Industries' potential here in our valuation report.

Gain insights into D&L Industries' past trends and performance with our Past report.

Summing It All Up

- Dive into all 58 of the Undervalued Asian Small Caps With Insider Buying we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|16.6% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|9.6% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|80.9% undervalued

NO

Community Contributor