Advertisement

- Australia

- /

- Professional Services

- /

- ASX:CUP

Count's (ASX:CUP) Shareholders Will Receive A Bigger Dividend Than Last Year

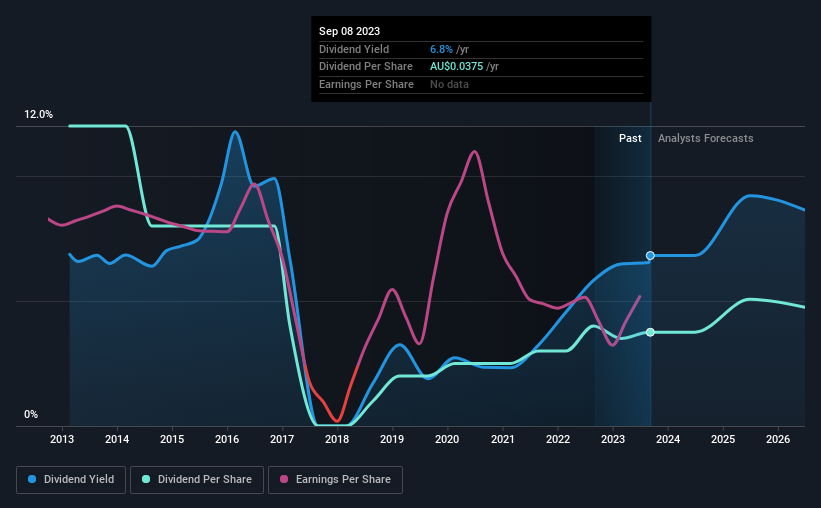

Count Limited (ASX:CUP) will increase its dividend on the 11th of October to A$0.0225, which is 13% higher than last year's payment from the same period of A$0.02. This takes the dividend yield to 6.8%, which shareholders will be pleased with.

See our latest analysis for Count

Count's Payment Has Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Prior to this announcement, Count's dividend was making up a very large proportion of earnings, and the company was also not generating any cash flow to offset this. Generally, we think that this would be a risky long term practice.

Over the next year, EPS is forecast to expand by 22.0%. Under the assumption that the dividend will continue along recent trends, we think the payout ratio could be 54% which would be quite comfortable going to take the dividend forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The dividend has gone from an annual total of A$0.12 in 2013 to the most recent total annual payment of A$0.0375. The dividend has fallen 69% over that period. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Could Be Constrained

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS is growing. Count has impressed us by growing EPS at 32% per year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which Count hasn't been doing.

Count's Dividend Doesn't Look Sustainable

In summary, while it's always good to see the dividend being raised, we don't think Count's payments are rock solid. Strong earnings growth means Count has the potential to be a good dividend stock in the future, despite the current payments being at elevated levels. We would be a touch cautious of relying on this stock primarily for the dividend income.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 3 warning signs for Count that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CUP

Count

Provides accounting, business advisory, and financial planning services in Australia.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor