David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Orbital Corporation Limited (ASX:OEC) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out the opportunities and risks within the AU Aerospace & Defense industry.

What Is Orbital's Net Debt?

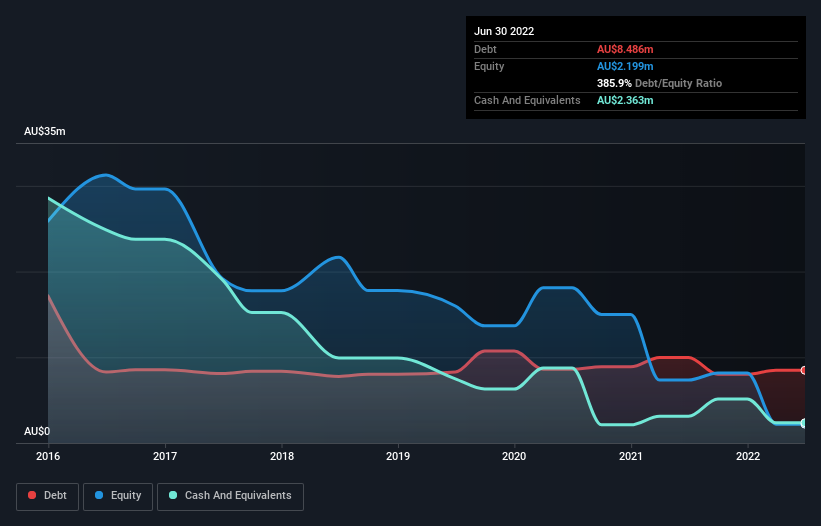

You can click the graphic below for the historical numbers, but it shows that Orbital had AU$8.49m of debt in June 2022, down from AU$9.99m, one year before. On the flip side, it has AU$2.36m in cash leading to net debt of about AU$6.12m.

How Healthy Is Orbital's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Orbital had liabilities of AU$20.4m due within 12 months and liabilities of AU$48.0k due beyond that. Offsetting this, it had AU$2.36m in cash and AU$1.19m in receivables that were due within 12 months. So it has liabilities totalling AU$16.9m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of AU$15.2m, we think shareholders really should watch Orbital's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Orbital will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Orbital made a loss at the EBIT level, and saw its revenue drop to AU$16m, which is a fall of 50%. To be frank that doesn't bode well.

Caveat Emptor

Not only did Orbital's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable AU$9.5m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it had negative free cash flow of AU$6.3m over the last twelve months. So suffice it to say we consider the stock to be risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 5 warning signs we've spotted with Orbital (including 2 which shouldn't be ignored) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:OEC

Orbital

Provides integrated propulsion systems and flight critical components for tactical unmanned aerial vehicles primarily in Australia and the United States.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives