Advertisement

The CEO of LaserBond Limited (ASX:LBL) is Wayne Hooper, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also assess whether LaserBond pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

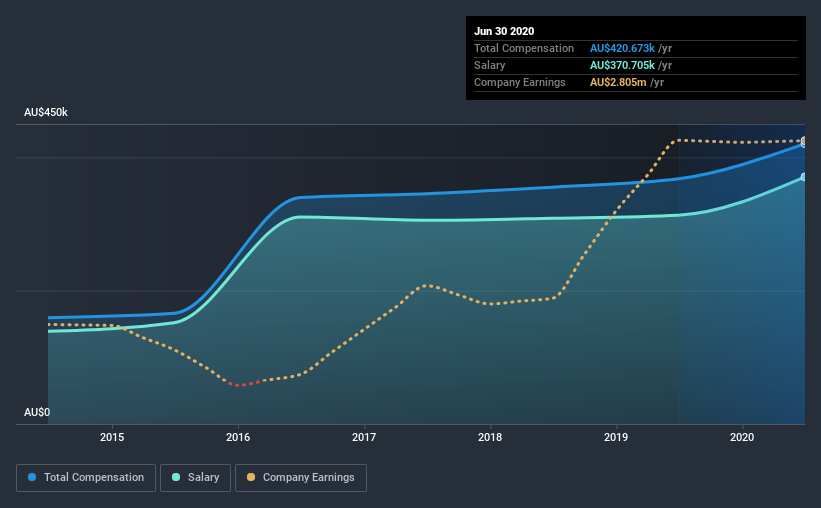

View our latest analysis for LaserBond

How Does Total Compensation For Wayne Hooper Compare With Other Companies In The Industry?

At the time of writing, our data shows that LaserBond Limited has a market capitalization of AU$57m, and reported total annual CEO compensation of AU$421k for the year to June 2020. That's a notable increase of 14% on last year. Notably, the salary which is AU$370.7k, represents most of the total compensation being paid.

On comparing similar-sized companies in the industry with market capitalizations below AU$259m, we found that the median total CEO compensation was AU$415k. This suggests that LaserBond remunerates its CEO largely in line with the industry average. Moreover, Wayne Hooper also holds AU$7.1m worth of LaserBond stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$371k | AU$313k | 88% |

| Other | AU$50k | AU$54k | 12% |

| Total Compensation | AU$421k | AU$368k | 100% |

Speaking on an industry level, nearly 80% of total compensation represents salary, while the remainder of 20% is other remuneration. LaserBond pays out 88% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at LaserBond Limited's Growth Numbers

Over the past three years, LaserBond Limited has seen its earnings per share (EPS) grow by 34% per year. It saw its revenue drop 2.2% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. While it would be good to see revenue growth, profits matter more in the end. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has LaserBond Limited Been A Good Investment?

We think that the total shareholder return of 381%, over three years, would leave most LaserBond Limited shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

As we touched on above, LaserBond Limited is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. The company is growing EPS and total shareholder returns have been pleasing. Indeed, many might consider that Wayne is compensated rather modestly, given the solid company performance! Stockholders might even be okay with a bump in pay, seeing as how investor returns have been so strong.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for LaserBond that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade LaserBond, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:LBL

LaserBond

A surface engineering company, engages in the development and application of materials, technologies, and methodologies to enhance operating performance and wear life of capital-intensive machinery components in Australia.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor