- Australia

- /

- Trade Distributors

- /

- ASX:EHL

Undiscovered Gems In Australia To Explore This November 2024

Reviewed by Simply Wall St

As the Australian market experiences modest gains with the ASX200 up 0.21% at 8,135 points, investors are closely watching sector performances, particularly as utilities and information technology lead the charge while energy and materials lag behind. In this dynamic environment, identifying promising small-cap stocks requires a keen eye for companies that demonstrate resilience and potential amidst shifting economic indicators and sector-specific challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Fiducian Group | NA | 9.94% | 6.48% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Bisalloy Steel Group | 0.95% | 10.27% | 24.14% | ★★★★★★ |

| Lycopodium | NA | 17.22% | 33.85% | ★★★★★★ |

| Red Hill Minerals | NA | 75.05% | 36.74% | ★★★★★★ |

| BSP Financial Group | 7.53% | 7.31% | 4.10% | ★★★★★☆ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| AMCIL | NA | 5.16% | 5.31% | ★★★★★☆ |

| Hearts and Minds Investments | 1.00% | 18.81% | 20.95% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

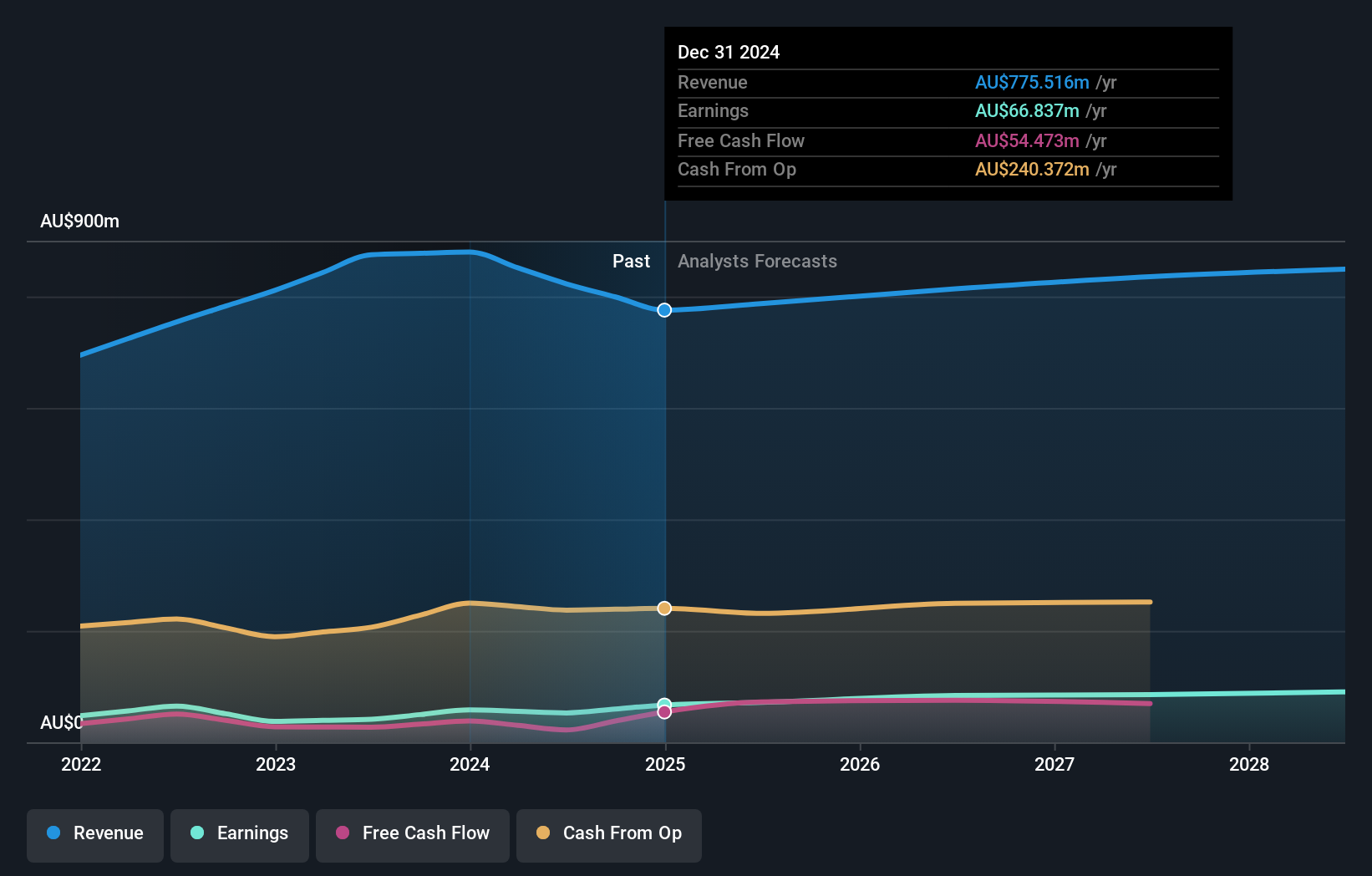

Emeco Holdings (ASX:EHL)

Simply Wall St Value Rating: ★★★★★☆

Overview: Emeco Holdings Limited is an Australian company that offers surface and underground mining equipment rental, along with complementary equipment and mining services, with a market capitalization of approximately A$390.90 million.

Operations: Emeco generates revenue primarily through its Rental segment, contributing A$544.75 million, followed by Workshops at A$282.41 million and Pit N Portal at A$111.77 million.

Emeco Holdings, a notable player in the equipment rental industry, is trading at 68.6% below its estimated fair value, presenting an intriguing opportunity. Over the past year, earnings surged by 27.4%, outpacing the industry average of 19.6%. The company's net debt to equity ratio stands at a satisfactory 32%, down from a hefty 231% five years ago, indicating improved financial health. With interest payments well covered by EBIT at 4.7 times and positive free cash flow, Emeco seems to be on solid ground financially. Recent leadership changes may further bolster strategic direction in this dynamic sector.

- Get an in-depth perspective on Emeco Holdings' performance by reading our health report here.

Assess Emeco Holdings' past performance with our detailed historical performance reports.

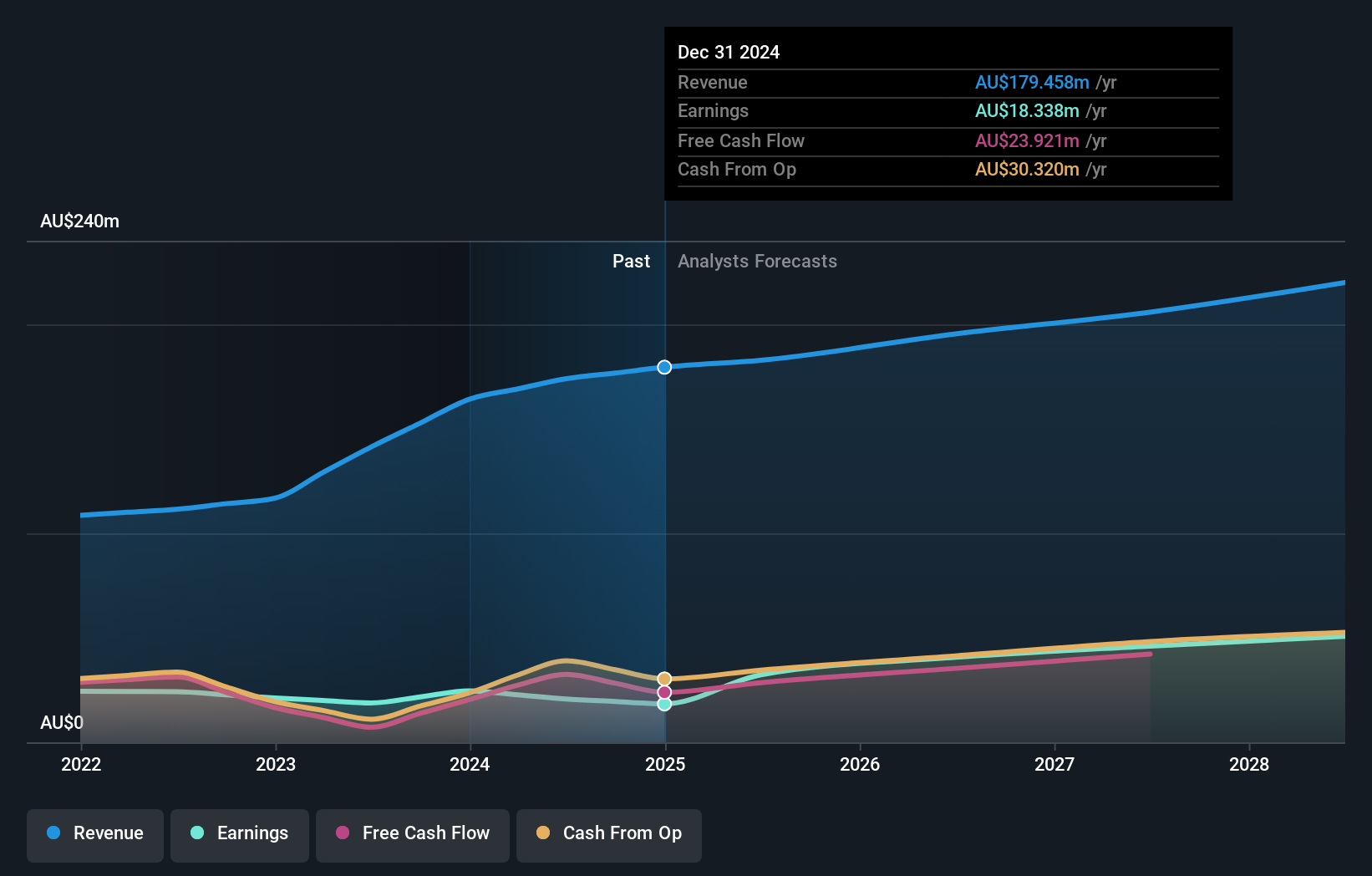

EQT Holdings (ASX:EQT)

Simply Wall St Value Rating: ★★★★★☆

Overview: EQT Holdings Limited, along with its subsidiaries, offers philanthropic, trustee executor, and investment services in Australia and has a market capitalization of approximately A$821.23 million.

Operations: EQT Holdings generates revenue primarily from its Trustee & Wealth Services segment, contributing A$99.08 million, and Corporate & Superannuation Trustee Services, adding A$71.51 million. The company also earns from its Corporate Trustee Services in the UK/Ireland with a revenue of A$3.52 million.

EQT Holdings, a notable player in the Australian market, has seen its debt to equity ratio rise from 4.6% to 18.3% over five years, indicating increased leverage. Despite this, earnings have grown modestly at 1.2% annually over the same period and are forecasted to grow by 22.69% per year moving forward. The company reported an increase in net income to A$20.71 million for the year ending June 2024, up from A$18.8 million previously, showcasing resilience amidst industry challenges with a net profit margin of approximately 11%. Additionally, EQT's interest payments are well covered by EBIT at a ratio of 9.6x.

- Unlock comprehensive insights into our analysis of EQT Holdings stock in this health report.

Evaluate EQT Holdings' historical performance by accessing our past performance report.

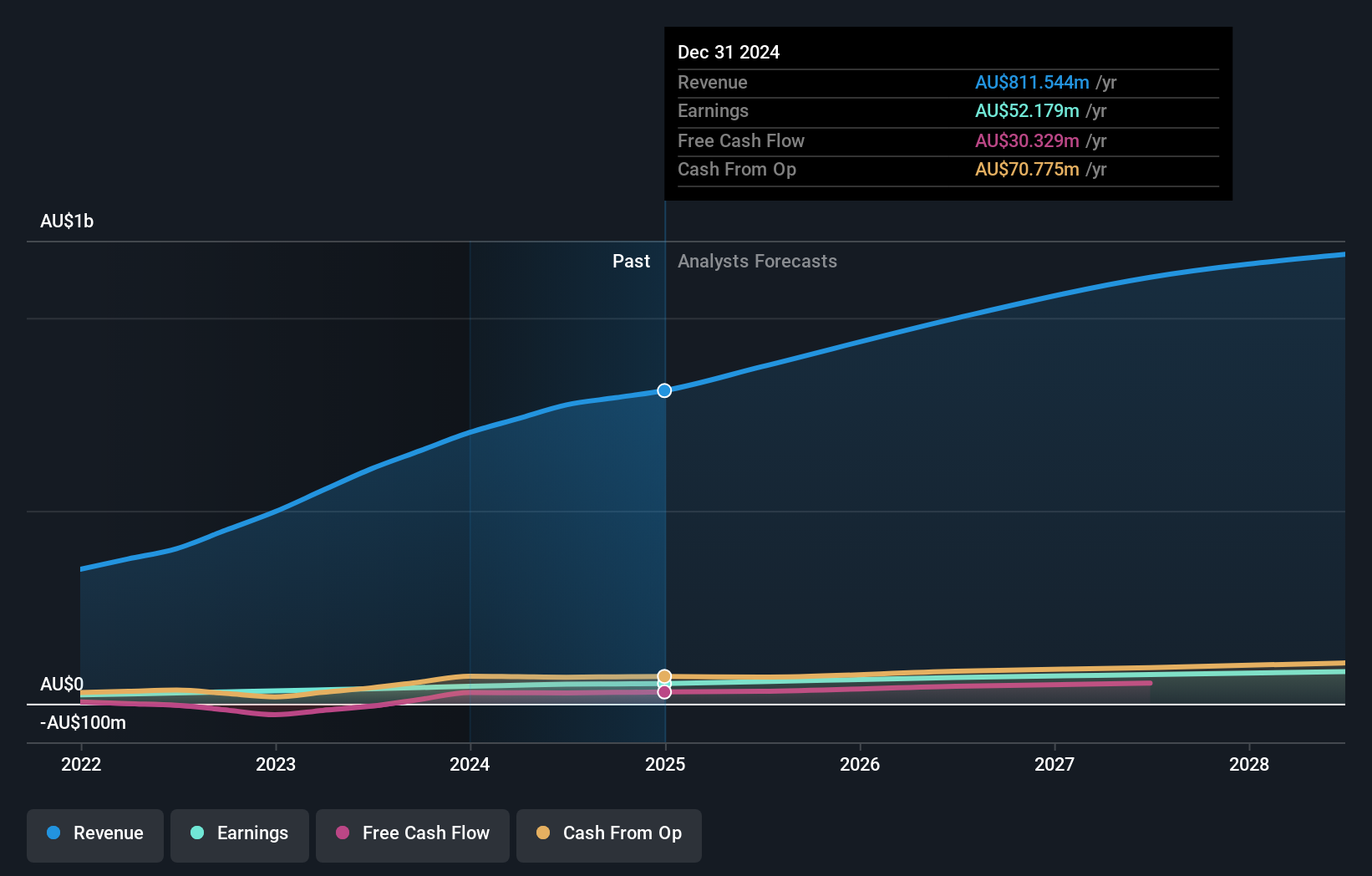

Mader Group (ASX:MAD)

Simply Wall St Value Rating: ★★★★★★

Overview: Mader Group Limited is a contracting company that offers specialist technical services in the mining, energy, and industrial sectors both in Australia and internationally, with a market cap of A$1.25 billion.

Operations: Mader Group generates revenue primarily from its Staffing & Outsourcing Services segment, which contributed A$774.47 million. The company's financial performance is reflected in its market capitalization of approximately A$1.25 billion.

Mader Group, a nimble player in the Commercial Services sector, has seen its debt to equity ratio shrink from 70.9% to 38.2% over five years, reflecting prudent financial management. Their earnings surged by 30.9% last year, outpacing the industry’s growth of 11.4%, and they trade at a significant discount of about 53% below estimated fair value. Despite recent insider selling, Mader's interest payments are comfortably covered with EBIT at nearly 20 times interest obligations. With net income rising to A$50 million from A$39 million and dividends increasing by 34%, their financial health appears robust as they join the S&P Global BMI Index.

- Take a closer look at Mader Group's potential here in our health report.

Explore historical data to track Mader Group's performance over time in our Past section.

Seize The Opportunity

- Take a closer look at our ASX Undiscovered Gems With Strong Fundamentals list of 58 companies by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Emeco Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EHL

Emeco Holdings

Provides surface and underground mining equipment rental, complementary equipment, and mining services in Australia.

Undervalued with solid track record.