- Australia

- /

- Auto Components

- /

- ASX:SFC

What To Know Before Buying Schaffer Corporation Limited (ASX:SFC) For Its Dividend

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Is Schaffer Corporation Limited (ASX:SFC) a good dividend stock? How would you know? Dividend paying companies with growing earnings can be highly rewarding in the long term. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

A high yield and a long history of paying dividends is an appealing combination for Schaffer. It would not be a surprise to discover that many investors buy it for the dividends. The company also bought back stock during the year, equivalent to approximately 1.2% of the company's market capitalisation at the time. There are a few simple ways to reduce the risks of buying Schaffer for its dividend, and we'll go through these below.

Explore this interactive chart for our latest analysis on Schaffer!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Schaffer paid out 34% of its profit as dividends, over the trailing twelve month period. This is a middling range that strikes a nice balance between paying dividends to shareholders, and retaining enough earnings to invest in future growth. One of the risks is that management reinvests the retained capital poorly instead of paying a higher dividend.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. Schaffer paid out a conservative 29% of its free cash flow as dividends last year. It's positive to see that Schaffer's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

We update our data on Schaffer every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

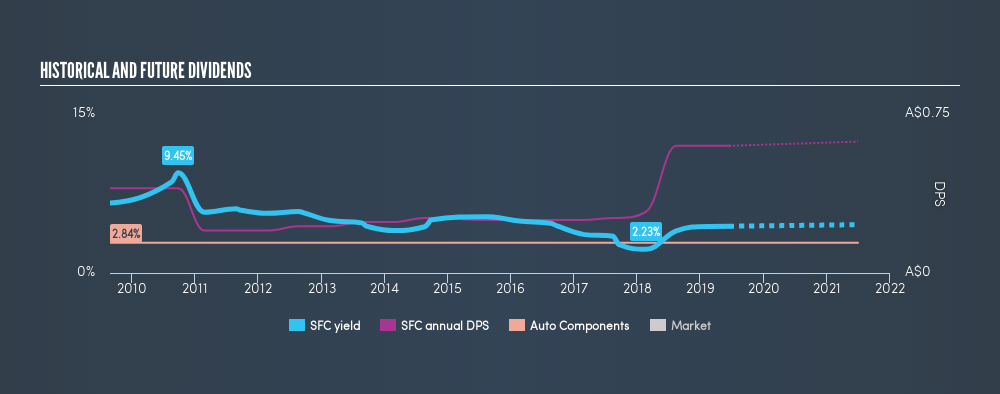

One of the major risks of relying on dividend income, is the potential for a company to struggle financially and cut its dividend. Not only is your income cut, but the value of your investment declines as well - nasty. For the purpose of this article, we only scrutinise the last decade of Schaffer's dividend payments. This dividend has been unstable, which we define as having fallen by at least 20% one or more times over this time. During the past ten-year period, the first annual payment was AU$0.40 in 2009, compared to AU$0.60 last year. This works out to be a compound annual growth rate (CAGR) of approximately 4.1% a year over that time. The dividends haven't grown at precisely 4.1% every year, but this is a useful way to average out the historical rate of growth.

We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments, we don't think this is an attractive combination.

Dividend Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share (EPS) are growing. Why take the risk of a dividend getting cut, unless there's a good chance of bigger dividends in future? It's good to see Schaffer has been growing its earnings per share at 27% a year over the past 5 years. With high earnings per share growth in recent times and a modest payout ratio, we think this is an attractive combination if earnings can be reinvested to generate further growth.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Firstly, we like that Schaffer has low and conservative payout ratios. We were also glad to see it growing earnings, but it was concerning to see the dividend has been cut at least once in the past. Overall we think Schaffer scores well on our analysis. It's not quite perfect, but we'd definitely be keen to take a closer look.

Now, if you want to look closer, it would be worth checking out our free research on Schaffer management tenure, salary, and performance.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ASX:SFC

Schaffer

A diversified industrial and investment company, engages in the manufacture and sale of automotive leather and building materials primarily in Australia, Asia, and Europe.

Flawless balance sheet average dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)