Advertisement

- Italy

- /

- Basic Materials

- /

- BIT:BZU

Why Buzzi Unicem S.p.A. (BIT:BZU) Is A Buy When Markets Go Down

When everything is going down, the best mindset to have is a long term one. Longstanding stocks such as Buzzi Unicem S.p.A. has fared well over time in a volatile stock market, which is why it’s my top pick to invest in. Below I take a look at three key characteristics of what makes a strong defensive stock investment: its size, financial health and track record.

Check out our latest analysis for Buzzi Unicem

Buzzi Unicem SpA, together with its subsidiaries, manufactures, distributes, and sells cement, ready-mix concrete, and aggregates. Started in 1907, and led by CEO , the company provides employment to 9.88k people and with the company's market capitalisation at €3.7b, we can put it in the mid-cap category. Generally, large-cap stocks are well-resourced and well-established meaning that a bear market will cause it to rejig some short-term capital allocations, but stock market volatility is hardly detrimental to its financial health and business operations. Therefore large-cap stocks are a safe bet to buy more of when the wider market is going down and down.

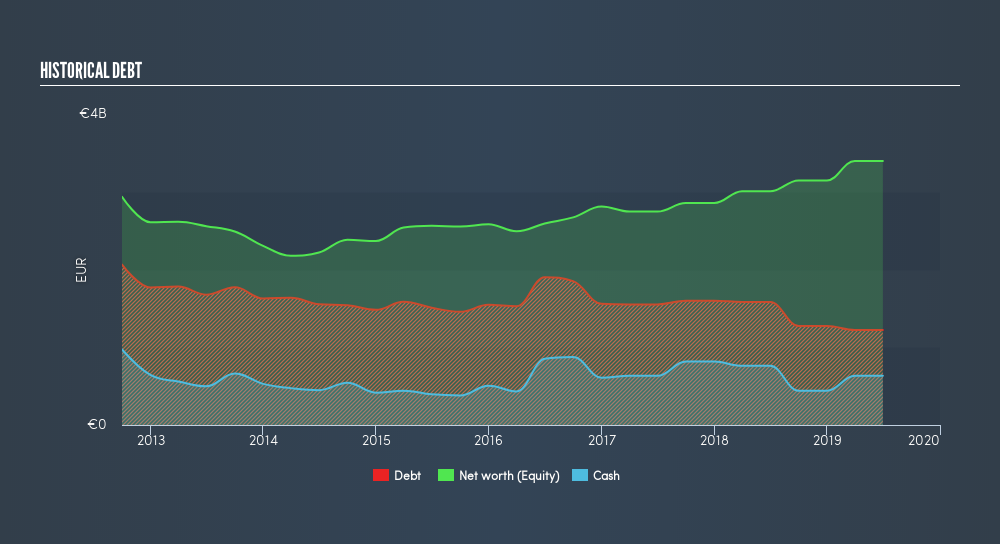

With €1.3b debt on its books, Buzzi Unicem has to pay interest periodically. This means it needs to have enough cash on hand to meet these upcoming expenses. Buzzi Unicem generates enough earnings to cover its interest payments, more specifically, its interest coverage ratio (EBIT/interest) is 5.97x, which is well-above the minimum requirement of 3x. Furthermore, its operating cash flows amply covers its total debt by 32%, which is higher than the bare minimum requirement of 20%. Its cash and short-term investment is also sufficient to cover other upcoming liabilities, which means BZU is financially robust in the face of a volatile market.

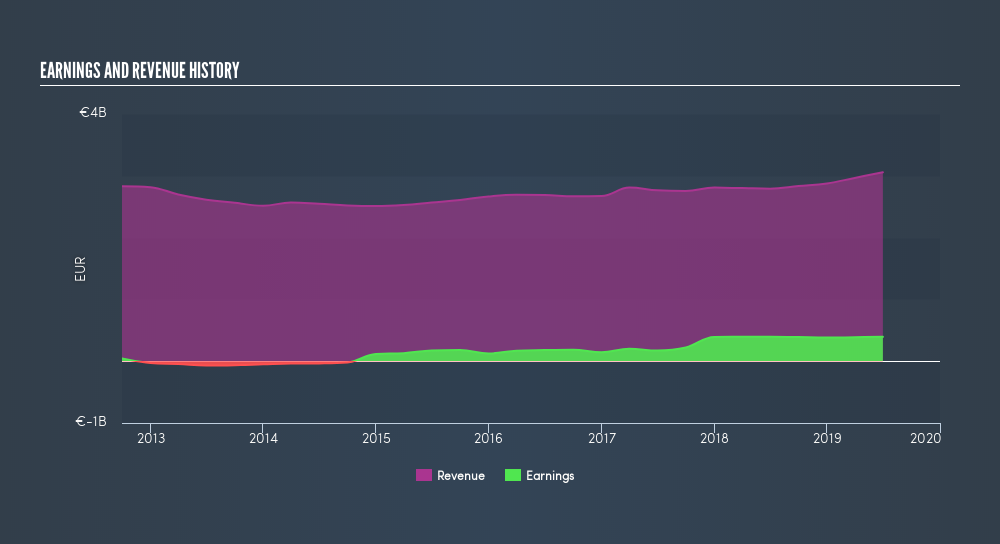

BZU’s annual earnings growth rate has been positive over the last five years, with an average rate of 35%, overtaking the industry growth rate of 17%. It has also returned an ROE of 12% recently, above the industry return of 9.5%. This continuous market outperformance demonstrates a strong track record of delivering robust returns over many years, raising my confidence in Buzzi Unicem as a long-term hold.

Next Steps:

Whether you're convinced or not, the key takeaway here is that every stock gets hit in a bear market, but not every stock deserves the blow. When prices are dropping like flies, now is the time to do your research and buy at a discount. Buzzi Unicem tick the boxes in terms of its scale, financial health and proven track record, but there are a few other things I have yet to consider. Below I've compiled a list of factors for you to continue your reading before you buy:- Future Outlook: What are well-informed industry analysts predicting for BZU’s future growth? Take a look at our free research report of analyst consensus for BZU’s outlook.

- Valuation: What is BZU worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether BZU is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About BIT:BZU

Buzzi

Manufactures, distributes, and sells cement, ready-mix concrete, and natural aggregates.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.5% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.825.6% undervalued

24 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32038.5% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

BR

browser on Bentley Systems ·

Bentley Systems’ Strategic Positioning in the Digital Infrastructure Cycle

Fair Value:US$15.72102.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6526.7% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.9628.6% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

89 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.8% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23053.3% overvalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative