Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:HBCP

What We Learned About Home Bancorp's (NASDAQ:HBCP) CEO Pay

John Bordelon has been the CEO of Home Bancorp, Inc. (NASDAQ:HBCP) since 2008, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for Home Bancorp

Comparing Home Bancorp, Inc.'s CEO Compensation With the industry

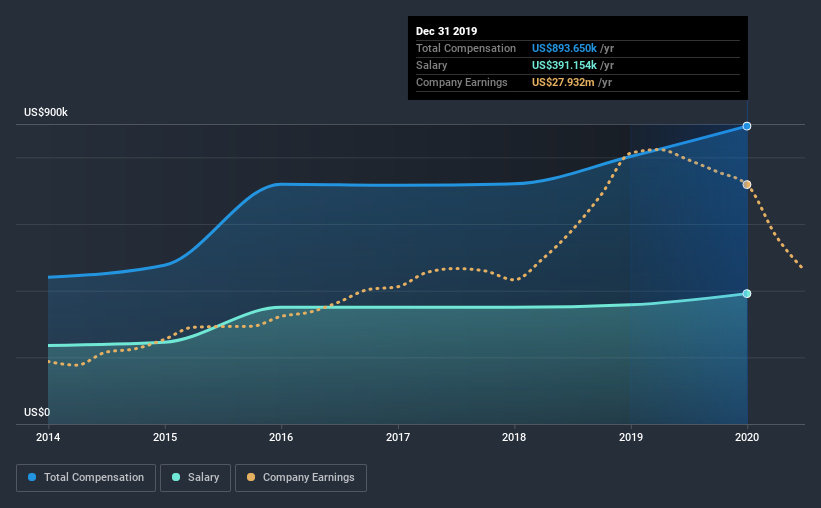

At the time of writing, our data shows that Home Bancorp, Inc. has a market capitalization of US$237m, and reported total annual CEO compensation of US$894k for the year to December 2019. Notably, that's an increase of 11% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$391k.

On examining similar-sized companies in the industry with market capitalizations between US$100m and US$400m, we discovered that the median CEO total compensation of that group was US$894k. So it looks like Home Bancorp compensates John Bordelon in line with the median for the industry. Moreover, John Bordelon also holds US$4.5m worth of Home Bancorp stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$391k | US$358k | 44% |

| Other | US$502k | US$445k | 56% |

| Total Compensation | US$894k | US$802k | 100% |

Talking in terms of the industry, salary represented approximately 58% of total compensation out of all the companies we analyzed, while other remuneration made up 42% of the pie. In Home Bancorp's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Home Bancorp, Inc.'s Growth Numbers

Home Bancorp, Inc. has reduced its earnings per share by 8.5% a year over the last three years. In the last year, its revenue is down 15%.

Overall this is not a very positive result for shareholders. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Home Bancorp, Inc. Been A Good Investment?

Since shareholders would have lost about 33% over three years, some Home Bancorp, Inc. investors would surely be feeling negative emotions. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

As we touched on above, Home Bancorp, Inc. is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Meanwhile, EPS growth and shareholder returns have been in the red for the last three years. We'd stop short of saying compensation is inappropriate, but we would understand if shareholders had questions regarding a future raise.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 2 warning signs for Home Bancorp that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading Home Bancorp or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Home Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGS:HBCP

Home Bancorp

Operates as the bank holding company for Home Bank, National Association that provides various banking products and services for individuals and businesses in Louisiana, Mississippi, and Texas, the United States.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1946.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4347.7% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.3% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AN

AnimalDoctorKwon on Ultragenyx Pharmaceutical ·

burns cash despite four approved drugs, trapped by structural inefficiencies and gene-therapy scaling hurdles that thin safety margins.

Fair Value:US$4636.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on BridgeBio Pharma ·

Faces a brutal commercial dogfight against Pfizer’s entrenched monopoly and Alnylam’s silencers, compressing its safety margins

Fair Value:US$25225.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Roivant Sciences ·

overprices legal wins and pipeline, ignoring fierce anti-FcRn competition, cash redeployment drag, and holding discounts.

Fair Value:US$10245.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.5% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5458.4% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.0% undervalued

61 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0