Advertisement

- United Kingdom

- /

- Trade Distributors

- /

- LSE:RS1

What Should We Expect From Electrocomponents plc's (LON:ECM) Earnings Over The Next Few Years?

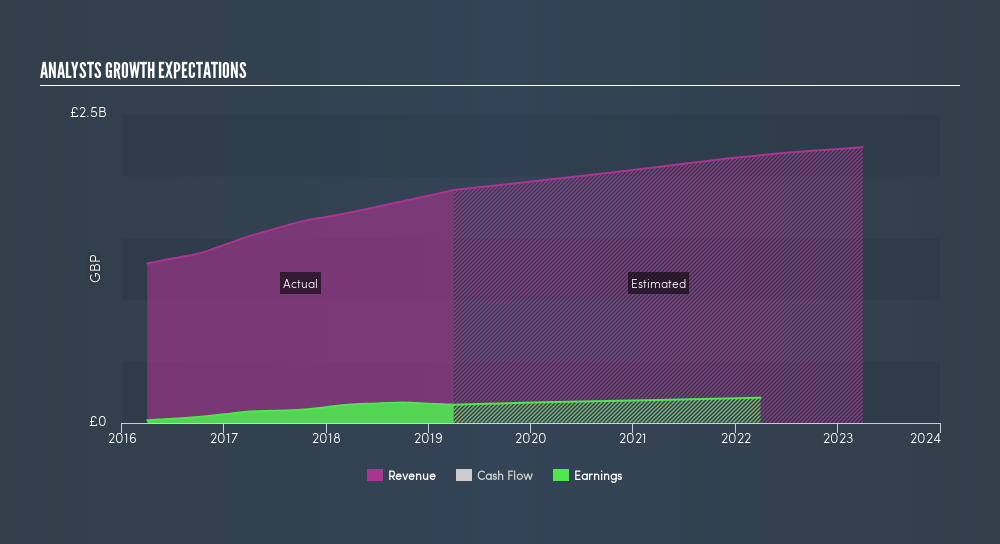

Electrocomponents plc's (LON:ECM) latest earnings announcement in June 2019 confirmed that the company experienced a slight headwind with earnings deteriorating from UK£150m to UK£148m, a change of -1.0%. Below, I've presented key growth figures on how market analysts view Electrocomponents's earnings growth outlook over the next few years and whether the future looks brighter. I will be using net income excluding extraordinary items in order to exclude one-off volatility which I am not interested in.

See our latest analysis for Electrocomponents

Analysts' outlook for the coming year seems positive, with earnings climbing by a robust 15%. This growth seems to continue into the following year with rates arriving at double digit 26% compared to today’s earnings, and finally hitting UK£204m by 2022.

Even though it is useful to understand the rate of growth year by year relative to today’s value, it may be more beneficial evaluating the rate at which the earnings are moving every year, on average. The pro of this technique is that we can get a better picture of the direction of Electrocomponents's earnings trajectory over the long run, irrespective of near term fluctuations, which may be more relevant for long term investors. To calculate this rate, I put a line of best fit through analyst consensus of forecasted earnings. The slope of this line is the rate of earnings growth, which in this case is 10%. This means that, we can expect Electrocomponents will grow its earnings by 10% every year for the next couple of years.

Next Steps:

For Electrocomponents, I've compiled three pertinent aspects you should further examine:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is ECM worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether ECM is currently mispriced by the market.

- Other High-Growth Alternatives: Are there other high-growth stocks you could be holding instead of ECM? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:RS1

RS Group

Engages in the distribution of maintenance, repair, and operations products and service solutions in the United Kingdom, the United States, France, Mexico, Germany, Italy, Switzerland, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

61 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

JA

Jamesiskindacool on Woodside Energy Group ·

Does WDS Have More in the Tank?

Fair Value:AU$36.611.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Treasury Wine Estates ·

Is TWE Aging Well?

Fair Value:AU$7.0733.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Transurban Group ·

Is TCL Worth the Toll?

Fair Value:AU$14.252.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

180 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative