Advertisement

- United Kingdom

- /

- Leisure

- /

- LSE:GAW

What Is Games Workshop Group's (LON:GAW) P/E Ratio After Its Share Price Tanked?

Unfortunately for some shareholders, the Games Workshop Group (LON:GAW) share price has dived 31% in the last thirty days. If we look back over the last year, the stock has gained 56% which is great, even in a bull market.

All else being equal, a share price drop should make a stock more attractive to potential investors. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

Check out our latest analysis for Games Workshop Group

Does Games Workshop Group Have A Relatively High Or Low P/E For Its Industry?

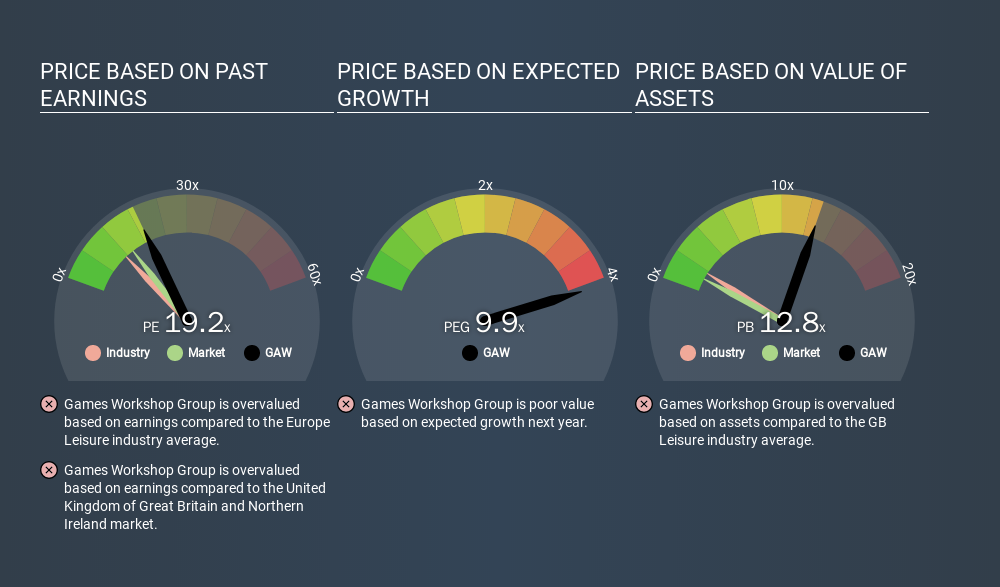

We can tell from its P/E ratio of 19.15 that there is some investor optimism about Games Workshop Group. The image below shows that Games Workshop Group has a higher P/E than the average (11.0) P/E for companies in the leisure industry.

Games Workshop Group's P/E tells us that market participants think the company will perform better than its industry peers, going forward. Shareholders are clearly optimistic, but the future is always uncertain. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. That means even if the current P/E is high, it will reduce over time if the share price stays flat. Then, a lower P/E should attract more buyers, pushing the share price up.

Games Workshop Group increased earnings per share by a whopping 30% last year. And earnings per share have improved by 62% annually, over the last five years. With that performance, I would expect it to have an above average P/E ratio.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

The 'Price' in P/E reflects the market capitalization of the company. Thus, the metric does not reflect cash or debt held by the company. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

Is Debt Impacting Games Workshop Group's P/E?

The extra options and safety that comes with Games Workshop Group's UK£33m net cash position means that it deserves a higher P/E than it would if it had a lot of net debt.

The Verdict On Games Workshop Group's P/E Ratio

Games Workshop Group has a P/E of 19.2. That's higher than the average in its market, which is 12.5. Its net cash position is the cherry on top of its superb EPS growth. So based on this analysis we'd expect Games Workshop Group to have a high P/E ratio. Given Games Workshop Group's P/E ratio has declined from 27.9 to 19.2 in the last month, we know for sure that the market is significantly less confident about the business today, than it was back then. For those who don't like to trade against momentum, that could be a warning sign, but a contrarian investor might want to take a closer look.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

But note: Games Workshop Group may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:GAW

Games Workshop Group

Engages in the design, manufacture, distribution, and sale of fantasy miniature figures and games in the United Kingdom, Continental Europe, North America, Australia, New Zealand, Asia, and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

90 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0328.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Alkane Resources ·

Alkane Resources, Record Production, A$374M Cash and a Giant Copper-Gold Project

Fair Value:AU$8.5482.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

Joe222 on Encore Capital Group ·

ECPG is a solid company

Fair Value:US$120.3833.4% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

115 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative