We Think ManagePay Systems Berhad (KLSE:MPAY) Needs To Drive Business Growth Carefully

Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So, the natural question for ManagePay Systems Berhad (KLSE:MPAY) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for ManagePay Systems Berhad

When Might ManagePay Systems Berhad Run Out Of Money?

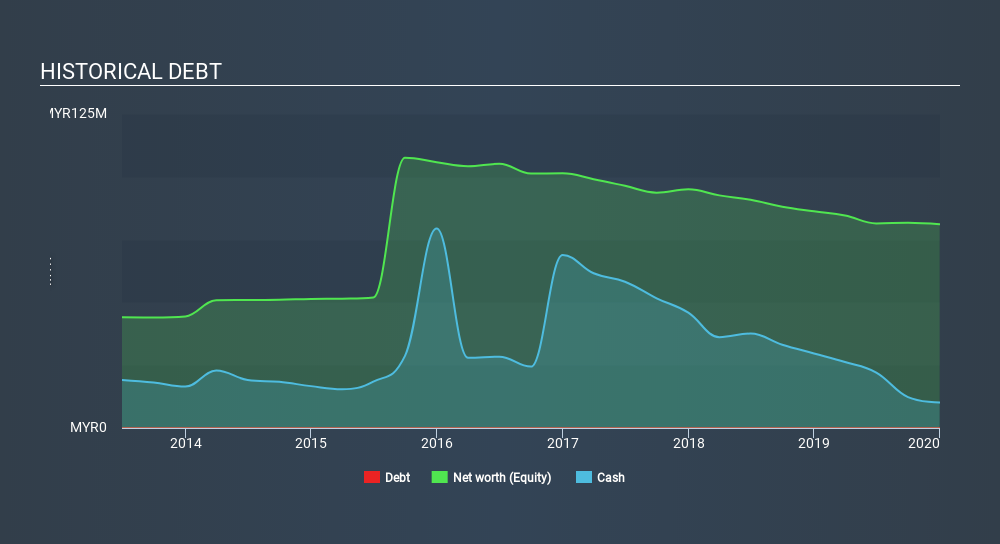

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. When ManagePay Systems Berhad last reported its balance sheet in December 2019, it had zero debt and cash worth RM10m. In the last year, its cash burn was RM14m. That means it had a cash runway of around 9 months as of December 2019. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. Depicted below, you can see how its cash holdings have changed over time.

How Well Is ManagePay Systems Berhad Growing?

On balance, we think it's mildly positive that ManagePay Systems Berhad trimmed its cash burn by 17% over the last twelve months. And arguably the operating revenue growth of 68% was even more impressive. It seems to be growing nicely. In reality, this article only makes a short study of the company's growth data. This graph of historic revenue growth shows how ManagePay Systems Berhad is building its business over time.

How Easily Can ManagePay Systems Berhad Raise Cash?

ManagePay Systems Berhad seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

ManagePay Systems Berhad has a market capitalisation of RM50m and burnt through RM14m last year, which is 28% of the company's market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

So, Should We Worry About ManagePay Systems Berhad's Cash Burn?

Even though its cash runway makes us a little nervous, we are compelled to mention that we thought ManagePay Systems Berhad's revenue growth was relatively promising. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. Separately, we looked at different risks affecting the company and spotted 6 warning signs for ManagePay Systems Berhad (of which 3 make us uncomfortable!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About KLSE:MPAY

ManagePay Systems Berhad

An investment holding company, engages in the provision of electronic payment solutions for banks and financial institutions, merchants, and card issuers in Malaysia.

Excellent balance sheet with low risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)