- United States

- /

- Banks

- /

- NasdaqGS:TCBK

TriCo Bancshares (NASDAQ:TCBK)'s Could Be A Buy For Its Upcoming Dividend

It looks like TriCo Bancshares (NASDAQ:TCBK) is about to go ex-dividend in the next 3 days. Investors can purchase shares before the 12th of December in order to be eligible for this dividend, which will be paid on the 30th of December.

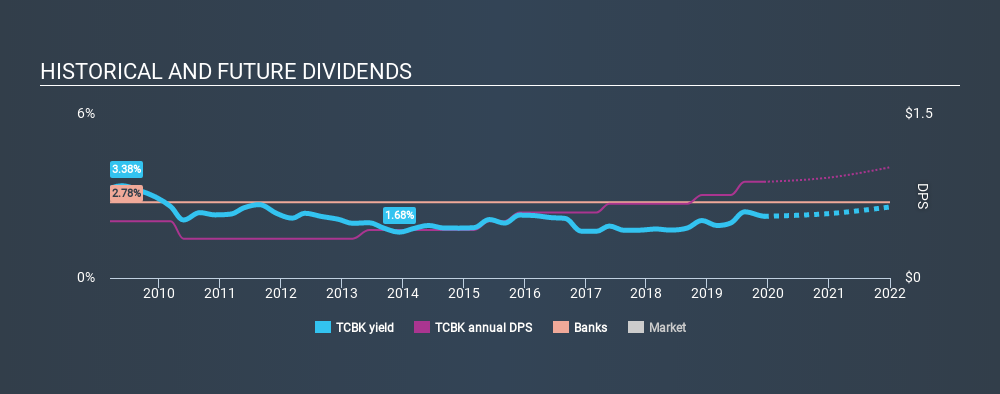

TriCo Bancshares's next dividend payment will be US$0.22 per share, and in the last 12 months, the company paid a total of US$0.88 per share. Looking at the last 12 months of distributions, TriCo Bancshares has a trailing yield of approximately 2.3% on its current stock price of $38.98. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for TriCo Bancshares

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. That's why it's good to see TriCo Bancshares paying out a modest 26% of its earnings.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. Fortunately for readers, TriCo Bancshares's earnings per share have been growing at 12% a year for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. TriCo Bancshares has delivered 5.4% dividend growth per year on average over the past ten years. Earnings per share have been growing much quicker than dividends, potentially because TriCo Bancshares is keeping back more of its profits to grow the business.

To Sum It Up

Has TriCo Bancshares got what it takes to maintain its dividend payments? Companies like TriCo Bancshares that are growing rapidly and paying out a low fraction of earnings, are usually reinvesting heavily in their business. This is one of the most attractive investment combinations under this analysis, as it can create substantial value for investors over the long run. TriCo Bancshares ticks a lot of boxes for us from a dividend perspective, and we think these characteristics should mark the company as deserving of further attention.

Wondering what the future holds for TriCo Bancshares? See what the five analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:TCBK

TriCo Bancshares

Operates as a bank holding company for Tri Counties Bank that provides commercial banking services to individual and corporate customers.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion

<html><head></head><body><div dir="auto">This is true here, but always true in the case of Alpha leaders. Often is takes a turn or two to get it right, like Gates to Nardella,  or Anton to Pinchar. This is when succession planning has failed or never happened. </div><div><br></div> </body></html>