Advertisement

- United States

- /

- Gas Utilities

- /

- NYSE:SR

These 4 Measures Indicate That Spire (NYSE:SR) Is Using Debt In A Risky Way

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Spire Inc. (NYSE:SR) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Spire

How Much Debt Does Spire Carry?

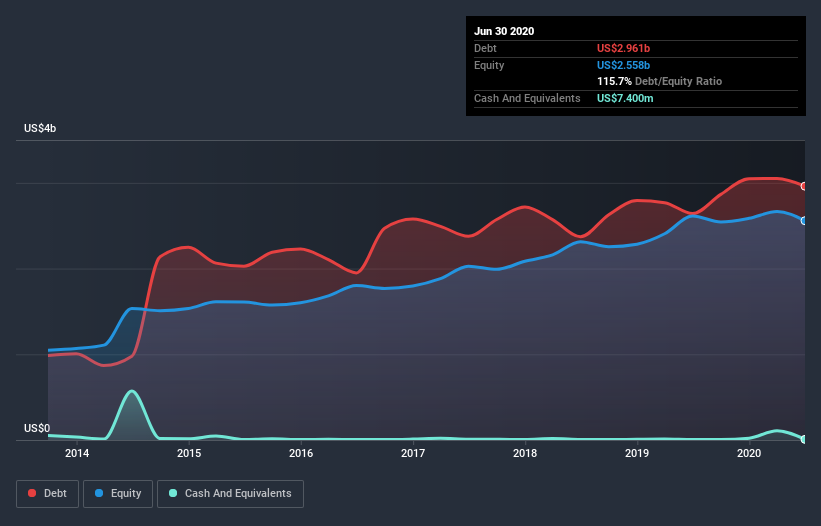

The image below, which you can click on for greater detail, shows that at June 2020 Spire had debt of US$2.96b, up from US$2.64b in one year. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is Spire's Balance Sheet?

The latest balance sheet data shows that Spire had liabilities of US$1.11b due within a year, and liabilities of US$4.16b falling due after that. On the other hand, it had cash of US$7.40m and US$258.6m worth of receivables due within a year. So its liabilities total US$5.0b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the US$2.97b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Spire would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Spire has a rather high debt to EBITDA ratio of 5.8 which suggests a meaningful debt load. However, its interest coverage of 3.0 is reasonably strong, which is a good sign. Notably, Spire's EBIT was pretty flat over the last year, which isn't ideal given the debt load. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Spire's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Spire burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Spire's conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to grow its EBIT isn't such a worry. We should also note that Gas Utilities industry companies like Spire commonly do use debt without problems. Taking into account all the aforementioned factors, it looks like Spire has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 5 warning signs for Spire (1 is concerning!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading Spire or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:SR

Spire

Engages in the purchase, retail distribution, and sale of natural gas to residential, commercial, industrial, and other end-users of natural gas in the United States.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45040.0% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2034.6% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

ES

Ester on Lagenda Properties Berhad ·

Lagenda Properties 录得创纪录销售额与收入,推动盈利能见度提升

Fair Value:RM 2.543.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on STLLR Gold ·

STLLR Gold, Eric Sprott + Agnico Backed: Massive Canadian Gold Developer at Junior Prices

Fair Value:CA$102.2298.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

PE

peter_4mgsy on Rhythm Pharmaceuticals ·

High-Growth Emerging Commercial Stage Biotech

Fair Value:US$13413.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

289 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

153 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

174 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

BU

buildittheywillcome on QXO ·

Lots of whimsical thinking on this consolidation play. Sprinkle "AI" and digital and folks get absolutely frothy. Highly leveraged M&A in a low margin, cyclical business. What could go wrong? How is QXO going to execute better than BLDR who has higher margins, closer relationships with builders, is further down the road of consolidating spend, and has a much better digital platform for builders despite challenges of slow market adoption. As an investment, QXO seems more of a "personality" play than a tech play in an sleepy industry Brad just "discovered". Please challenge this POV and help me see what I'm missing in QXO.

0

|0