Advertisement

- India

- /

- Construction

- /

- NSEI:SEMAC

Should You Be Impressed By Revathi Equipment's (NSE:REVATHI) Returns on Capital?

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Although, when we looked at Revathi Equipment (NSE:REVATHI), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Revathi Equipment is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

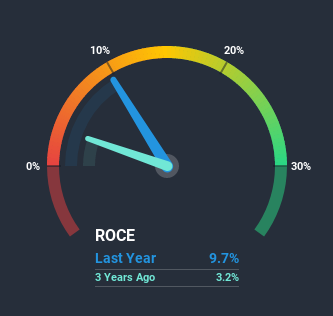

0.097 = ₹201m ÷ (₹2.6b - ₹562m) (Based on the trailing twelve months to June 2020).

Therefore, Revathi Equipment has an ROCE of 9.7%. On its own that's a low return on capital but it's in line with the industry's average returns of 9.5%.

Check out our latest analysis for Revathi Equipment

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Revathi Equipment, check out these free graphs here.

What The Trend Of ROCE Can Tell Us

In terms of Revathi Equipment's historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 13% over the last five years. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a side note, Revathi Equipment has done well to pay down its current liabilities to 21% of total assets. That could partly explain why the ROCE has dropped. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.In Conclusion...

We're a bit apprehensive about Revathi Equipment because despite more capital being deployed in the business, returns on that capital and sales have both fallen. Investors haven't taken kindly to these developments, since the stock has declined 46% from where it was five years ago. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

Revathi Equipment does come with some risks though, we found 3 warning signs in our investment analysis, and 1 of those is a bit concerning...

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you’re looking to trade Revathi Equipment, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:SEMAC

Semac Construction

Provides integrated design, engineering, procurement, construction, and consultancy services for commercial and industrial projects in India.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5360.2% undervalued

136 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18053.4% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.313.7% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2451.0% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Paradigm Biopharmaceuticals ·

I am a shareholder and my investment thesis is maintained

Fair Value:AU$183.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Blackrock Silver ·

Nevada 1st-Tier 30 Baggers Silver Play Potential

Fair Value:CA$23.7294.2% undervalued

3 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Wasco Greenergy Berhad ·

Wasco Greenergy Positioned For Stronger Recovery Backed By Renewable Energy Expansion

Fair Value:RM 0.933.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.9% undervalued

108 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74016.4% undervalued

37 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6112.2% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative