Should Income Investors Look At Kemira Oyj (HEL:KEMIRA) Before Its Ex-Dividend?

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Kemira Oyj (HEL:KEMIRA) is about to go ex-dividend in just 2 days. Investors can purchase shares before the 26th of March in order to be eligible for this dividend, which will be paid on the 7th of April.

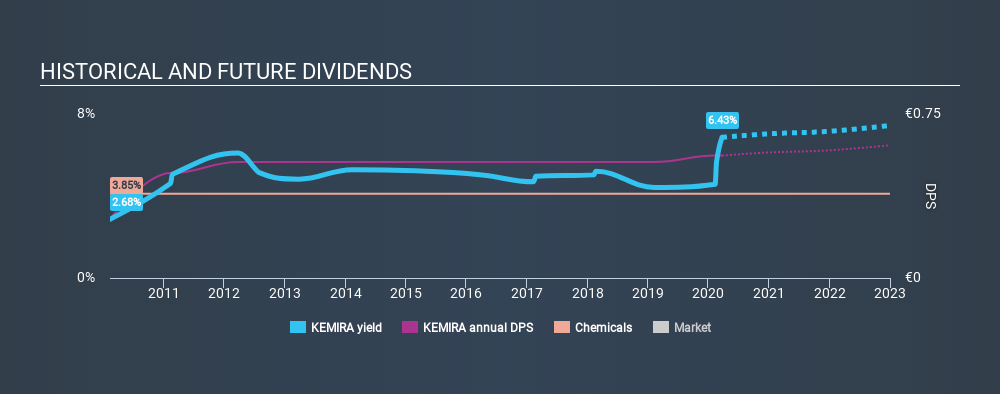

Kemira Oyj's upcoming dividend is €0.28 a share, following on from the last 12 months, when the company distributed a total of €0.56 per share to shareholders. Based on the last year's worth of payments, Kemira Oyj stock has a trailing yield of around 6.4% on the current share price of €8.705. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

See our latest analysis for Kemira Oyj

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. It paid out 78% of its earnings as dividends last year, which is not unreasonable, but limits reinvestment in the business and leaves the dividend vulnerable to a business downturn. We'd be worried about the risk of a drop in earnings. A useful secondary check can be to evaluate whether Kemira Oyj generated enough free cash flow to afford its dividend. Thankfully its dividend payments took up just 44% of the free cash flow it generated, which is a comfortable payout ratio.

It's positive to see that Kemira Oyj's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. With that in mind, we're encouraged by the steady growth at Kemira Oyj, with earnings per share up 4.1% on average over the last five years. A payout ratio of 78% looks like a tacit signal from management that reinvestment opportunities in the business are low. In line with limited earnings growth in recent years, this is not the most appealing combination.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the last ten years, Kemira Oyj has lifted its dividend by approximately 7.6% a year on average. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

To Sum It Up

Is Kemira Oyj worth buying for its dividend? Earnings per share growth has been modest and Kemira Oyj paid out over half of its profits and less than half of its free cash flow, although both payout ratios are within normal limits. In summary, while it has some positive characteristics, we're not inclined to race out and buy Kemira Oyj today.

On that note, you'll want to research what risks Kemira Oyj is facing. In terms of investment risks, we've identified 2 warning signs with Kemira Oyj and understanding them should be part of your investment process.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About HLSE:KEMIRA

Kemira Oyj

Operates as a chemicals company in Finland, rest of Europe, the Middle East, Africa, the Americas, and the Asia Pacific.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)