- United States

- /

- Energy Services

- /

- NYSE:NINE

Nine Energy Service, Inc. (NYSE:NINE) Analysts Are Cutting Their Estimates: Here's What You Need To Know

Nine Energy Service, Inc. (NYSE:NINE) just released its latest quarterly report and things are not looking great. It was a pretty negative result overall, with revenues of US$147m missing analyst predictions by 5.6%. Worse, the business reported a statutory loss of US$10.22 per share, much larger than the analysts had forecast prior to the result. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for Nine Energy Service

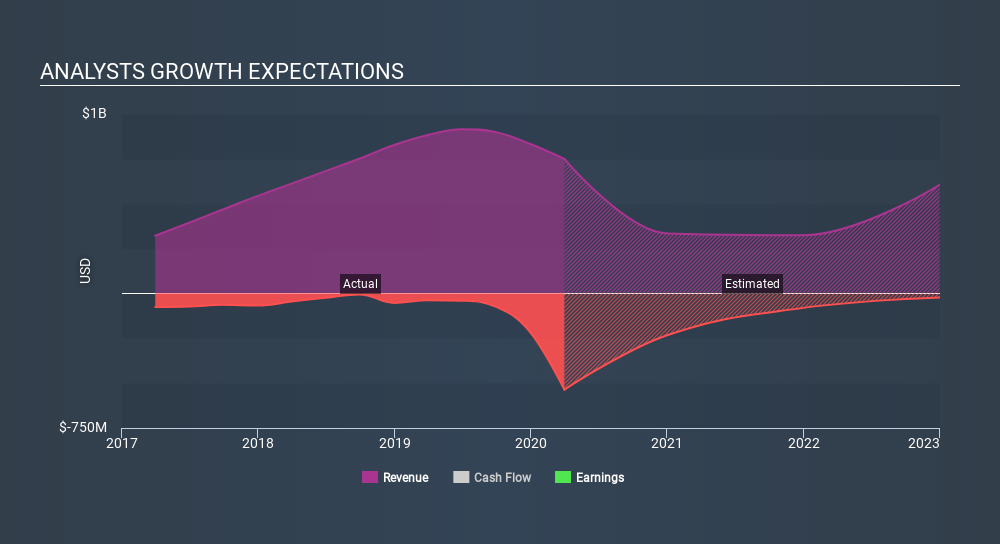

After the latest results, the consensus from Nine Energy Service's five analysts is for revenues of US$334.4m in 2020, which would reflect a concerning 55% decline in sales compared to the last year of performance. The loss per share is expected to greatly reduce in the near future, narrowing 43% to US$10.41. Before this latest report, the consensus had been expecting revenues of US$404.4m and US$2.61 per share in losses. So there's been quite a change-up of views after the recent consensus updates, withthe analysts making a serious cut to their revenue outlook while also expecting losses per share to increase.

The analysts lifted their price target 22% to US$1.03, implicitly signalling that lower earnings per share are not expected to have a longer-term impact on the stock's value. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Nine Energy Service analyst has a price target of US$1.85 per share, while the most pessimistic values it at US$0.50. With such a wide range in price targets, analysts are almost certainly betting on widely divergent outcomes in the underlying business. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with the forecast 55% revenue decline a notable change from historical growth of 27% over the last three years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 0.05% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Nine Energy Service is expected to lag the wider industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Nine Energy Service. Unfortunately, they also downgraded their revenue estimates, and our data indicates revenues are expected to perform worse than the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Nine Energy Service analysts - going out to 2022, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 4 warning signs for Nine Energy Service that you should be aware of.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:NINE

Nine Energy Service

Operates as an onshore completion services provider that targets unconventional oil and gas resource development in North American basins and internationally.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)