Advertisement

- India

- /

- Personal Products

- /

- NSEI:EMAMILTD

It Might Not Be A Great Idea To Buy Emami Limited (NSE:EMAMILTD) For Its Next Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Emami Limited (NSE:EMAMILTD) is about to trade ex-dividend in the next 3 days. Investors can purchase shares before the 12th of November in order to be eligible for this dividend, which will be paid on the 5th of December.

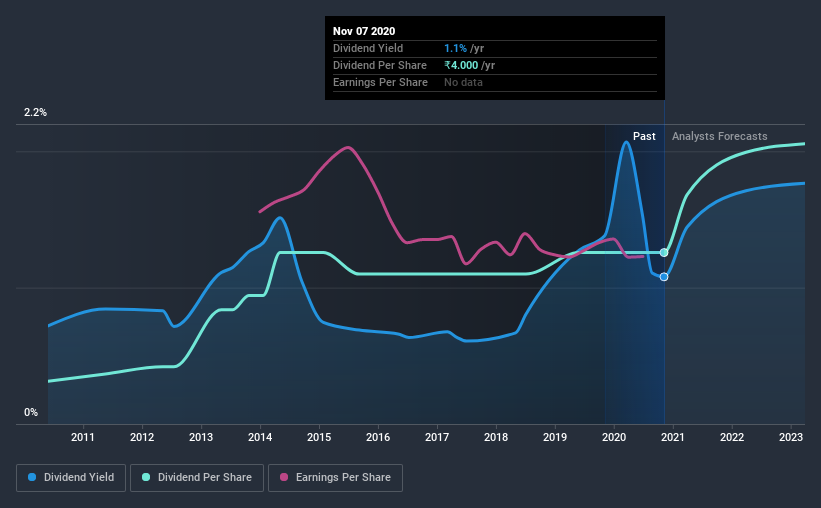

Emami's upcoming dividend is ₹4.00 a share, following on from the last 12 months, when the company distributed a total of ₹4.00 per share to shareholders. Based on the last year's worth of payments, Emami has a trailing yield of 1.1% on the current stock price of ₹370.95. If you buy this business for its dividend, you should have an idea of whether Emami's dividend is reliable and sustainable. As a result, readers should always check whether Emami has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for Emami

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Emami is paying out an acceptable 60% of its profit, a common payout level among most companies. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out 98% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want look more closely here.

Emami paid out less in dividends than it reported in profits, but unfortunately it didn't generate enough cash to cover the dividend. Were this to happen repeatedly, this would be a risk to Emami's ability to maintain its dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Readers will understand then, why we're concerned to see Emami's earnings per share have dropped 8.9% a year over the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Since the start of our data, 10 years ago, Emami has lifted its dividend by approximately 15% a year on average. Growing the dividend payout ratio while earnings are declining can deliver nice returns for a while, but it's always worth checking for when the company can't increase the payout ratio any more - because then the music stops.

Final Takeaway

From a dividend perspective, should investors buy or avoid Emami? Emami had an average payout ratio, but its free cash flow was lower and earnings per share have been declining. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Emami.

With that in mind though, if the poor dividend characteristics of Emami don't faze you, it's worth being mindful of the risks involved with this business. Our analysis shows 2 warning signs for Emami and you should be aware of them before buying any shares.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

When trading Emami or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emami might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:EMAMILTD

Emami

Manufactures and markets personal and healthcare products in India and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor