- United Kingdom

- /

- Diversified Financial

- /

- LSE:DVNO

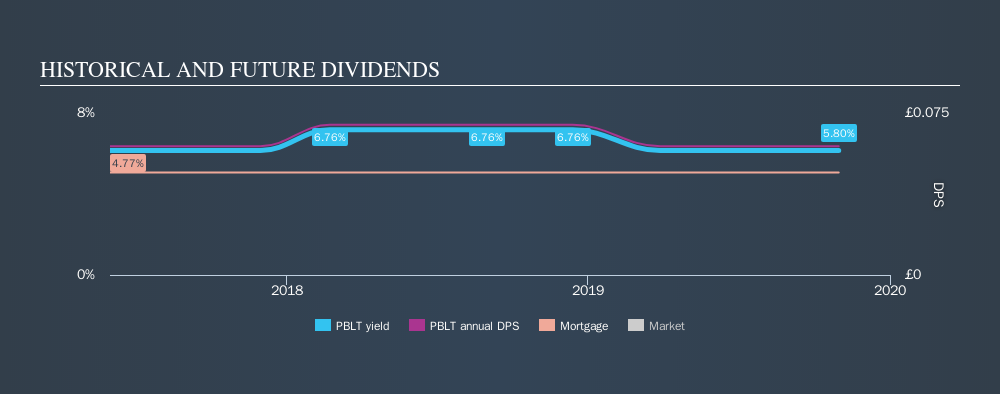

Is TOC Property Backed Lending Trust Plc (LON:PBLT) An Attractive Dividend Stock?

Today we'll take a closer look at TOC Property Backed Lending Trust Plc (LON:PBLT) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

TOC Property Backed Lending Trust yields a solid 5.8%, although it has only been paying for two years. It's certainly an attractive yield, but readers are likely curious about its staying power. Some simple analysis can reduce the risk of holding TOC Property Backed Lending Trust for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. TOC Property Backed Lending Trust paid out 227% of its profit as dividends, over the trailing twelve month period. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. It has only been paying dividends for a few short years, and the dividend has already been cut at least once. This is one income stream we're not ready to live on. Its most recent annual dividend was UK£0.06 per share, effectively flat on its first payment two years ago.

Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's not great to see that TOC Property Backed Lending Trust's have fallen at approximately 7.2% over the past five years. Declining earnings per share over a number of years is not a great sign for the dividend investor. Without some improvement, this does not bode well for the long term value of a company's dividend.

We'd also point out that TOC Property Backed Lending Trust issued a meaningful number of new shares in the past year. Regularly issuing new shares can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. TOC Property Backed Lending Trust is paying out a larger percentage of its profit than we're comfortable with. Earnings per share are down, and TOC Property Backed Lending Trust's dividend has been cut at least once in the past, which is disappointing. In short, we're not keen on TOC Property Backed Lending Trust from a dividend perspective. Businesses can change, but we've spotted a few too many concerns with this one to get comfortable.

Are management backing themselves to deliver performance? Check their shareholdings in TOC Property Backed Lending Trust in our latest insider ownership analysis.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:DVNO

Develop North

An investment company, provides a portfolio of fixed rate loans primarily secured over land and/or property in the United Kingdom.

Excellent balance sheet with proven track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)