Advertisement

- United States

- /

- Chemicals

- /

- NYSE:MTX

Is Minerals Technologies Inc.'s (NYSE:MTX) CEO Pay Justified?

In 2016 Doug Dietrich was appointed CEO of Minerals Technologies Inc. (NYSE:MTX). This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for Minerals Technologies

How Does Doug Dietrich's Compensation Compare With Similar Sized Companies?

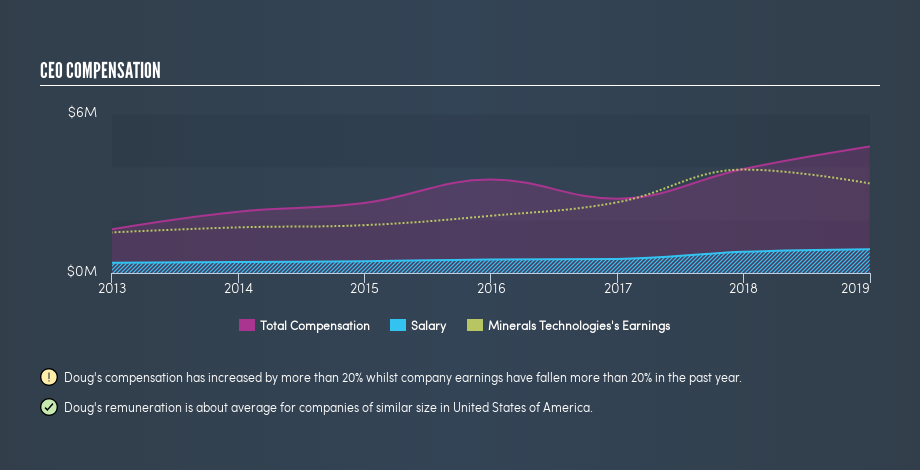

At the time of writing our data says that Minerals Technologies Inc. has a market cap of US$1.7b, and is paying total annual CEO compensation of US$4.8m. (This is based on the year to December 2018). We think total compensation is more important but we note that the CEO salary is lower, at US$898k. As part of our analysis we looked at companies in the same jurisdiction, with market capitalizations of US$1.0b to US$3.2b. The median total CEO compensation was US$4.1m.

That means Doug Dietrich receives fairly typical remuneration for the CEO of a company that size. Although this fact alone doesn't tell us a great deal, it becomes more relevant when considered against the business performance.

You can see a visual representation of the CEO compensation at Minerals Technologies, below.

Is Minerals Technologies Inc. Growing?

Over the last three years Minerals Technologies Inc. has grown its earnings per share (EPS) by an average of 14% per year (using a line of best fit). It achieved revenue growth of 3.5% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see modest revenue growth, suggesting the underlying business is healthy.

Has Minerals Technologies Inc. Been A Good Investment?

Since shareholders would have lost about 33% over three years, some Minerals Technologies Inc. shareholders would surely be feeling negative emotions. It therefore might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Doug Dietrich is paid around what is normal the leaders of comparable size companies.

We think that the EPS growth is very pleasing, but we find the returns over the last three years to be lacking. Considering the improvement in earnings per share, one could argue that the CEO pay is appropriate, albeit not too low. CEO compensation is one thing, but it is also interesting to check if the CEO is buying or selling Minerals Technologies (free visualization of insider trades).

Important note: Minerals Technologies may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:MTX

Minerals Technologies

Develops, produces, and markets various mineral, mineral-based products and services.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on High Arctic Overseas Holdings ·

Deep Value Multi Bagger Opportunity

Fair Value:CA$773.0% undervalued

6 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Okinawa Cellular Telephone ·

Mobile strategy pays off as churn falls

Fair Value:JP¥3.26k8.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ED

Edward_Sterling on Micron Technology ·

Micron’s AI Crown Sits on a Cycle That Hasn’t Changed

Fair Value:US$1.98k45.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative