Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:INTC

Intel Corporation Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

It's been a pretty great week for Intel Corporation (NASDAQ:INTC) shareholders, with its shares surging 15% to US$68.47 in the week since its latest full-year results. The result was positive overall - although revenues of US$72b were in line with what analysts predicted, Intel surprised by delivering a statutory profit of US$4.71 per share, modestly greater than expected. Analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see analysts' latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Intel

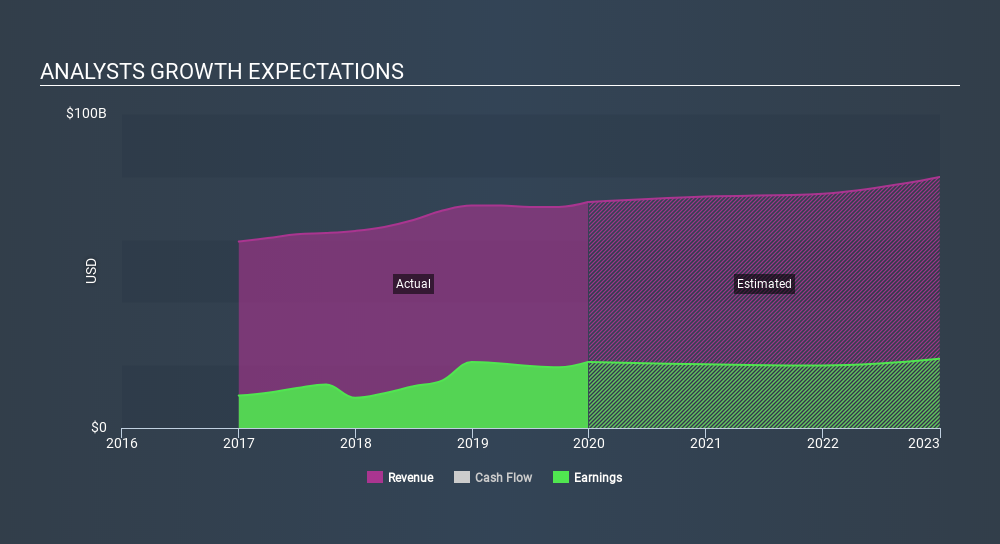

Taking into account the latest results, the most recent consensus for Intel from 37 analysts is for revenues of US$73.7b in 2020, which is a credible 2.5% increase on its sales over the past 12 months. Statutory per share are forecast to be US$4.74, approximately in line with the last 12 months. In the lead-up to this report, analysts had been modelling revenues of US$72.2b and earnings per share (EPS) of US$4.46 in 2020. It looks like there's been a modest increase in sentiment following the latest results, with analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

It will come as no surprise to learn that analysts have increased their price target for Intel 15% to US$66.59 on the back of these upgrades. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Intel, with the most bullish analyst valuing it at US$90.00 and the most bearish at US$45.00 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

It can also be useful to step back and take a broader view of how analyst forecasts compare to Intel's performance in recent years. We would highlight that Intel's revenue growth is expected to slow, with forecast 2.5% increase next year well below the historical 6.2%p.a. growth over the last five years. By way of comparison, other companies in this market with analyst coverage, are forecast to grow their revenue at 8.2% per year. So it's pretty clear that, while revenue growth is expected to slow down, analysts still expect the wider market to grow faster than Intel.

The Bottom Line

The most important thing to take away from this is that analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Intel following these results. They also upgraded their revenue estimates for next year, even though sales are expected to grow slower than the wider market. There was also a nice increase in the price target, with analysts feeling that the intrinsic value of the business is improving.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Intel going out to 2022, and you can see them free on our platform here..

It might also be worth considering whether Intel's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:INTC

Intel

Designs, develops, manufactures, markets, sells, and services computing and related end products and services in the United States, Ireland, Israel, and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

ST

StoxEurope on Sipef ·

Why I Invest in SIPEF?

Fair Value:€12125.5% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on Kucingko Berhad ·

Kucingko Berhad: Fundamentals Show Early Recovery as Creative Content Expansion Gains Traction

Fair Value:RM 0.012733.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on BP Silver ·

“valer un Potosí” GOOGLE IT. Now you’re should be kinda locked in. Educate yourself, Read the rest.

Fair Value:CA$685.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

AN

andre_k1tsg on Companhia de Saneamento de Minas Gerais ·

Eu André José Julião digo o caminho da melhorar a toda população esta entrando no trilhos.

0

|0