Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:SAIA

How Does Saia's (NASDAQ:SAIA) P/E Compare To Its Industry, After Its Big Share Price Gain?

Saia (NASDAQ:SAIA) shareholders are no doubt pleased to see that the share price has had a great month, posting a 39% gain, recovering from prior weakness. That brought the twelve month gain to a very sharp 56%.

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. So some would prefer to hold off buying when there is a lot of optimism towards a stock. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). Investors have optimistic expectations of companies with higher P/E ratios, compared to companies with lower P/E ratios.

View our latest analysis for Saia

Does Saia Have A Relatively High Or Low P/E For Its Industry?

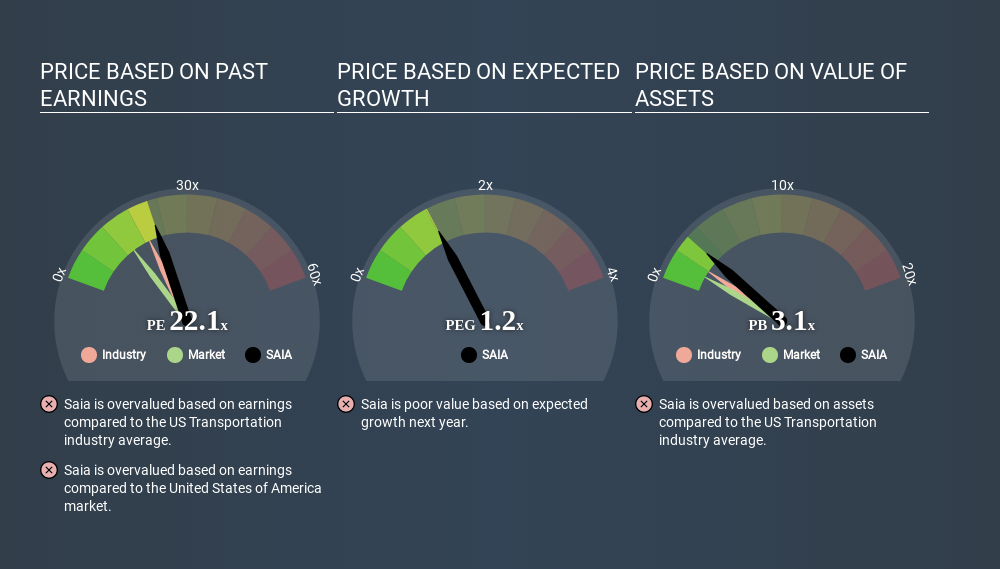

We can tell from its P/E ratio of 22.12 that there is some investor optimism about Saia. As you can see below, Saia has a higher P/E than the average company (20.3) in the transportation industry.

Saia's P/E tells us that market participants think the company will perform better than its industry peers, going forward. Shareholders are clearly optimistic, but the future is always uncertain. So investors should delve deeper. I like to check if company insiders have been buying or selling.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. That means unless the share price increases, the P/E will reduce in a few years. So while a stock may look expensive based on past earnings, it could be cheap based on future earnings.

Most would be impressed by Saia earnings growth of 12% in the last year. And it has bolstered its earnings per share by 15% per year over the last five years. This could arguably justify a relatively high P/E ratio.

Remember: P/E Ratios Don't Consider The Balance Sheet

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. That means it doesn't take debt or cash into account. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

So What Does Saia's Balance Sheet Tell Us?

Saia's net debt is 3.9% of its market cap. The market might award it a higher P/E ratio if it had net cash, but its unlikely this low level of net borrowing is having a big impact on the P/E multiple.

The Verdict On Saia's P/E Ratio

Saia trades on a P/E ratio of 22.1, which is above its market average of 14.7. The company is not overly constrained by its modest debt levels, and its recent EPS growth very solid. Therefore, it's not particularly surprising that it has a above average P/E ratio. What we know for sure is that investors have become much more excited about Saia recently, since they have pushed its P/E ratio from 15.9 to 22.1 over the last month. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors have an opportunity when market expectations about a stock are wrong. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

You might be able to find a better buy than Saia. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About NasdaqGS:SAIA

Saia

Operates as a transportation company in North America.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

158 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

OL

OLetourneau on Texas Instruments ·

TXN — Fair Value $285

Fair Value:US$284.320.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OL

OLetourneau on Otis Worldwide ·

OTIS — Fair Value $87

Fair Value:US$88.5816.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OL

OLetourneau on Moody's ·

MCO — Fair Value $529

Fair Value:US$5299.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

279 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

166 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0