- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1001

Here's Why We Don't Think Hong Kong Shanghai Alliance Holdings's (HKG:1001) Statutory Earnings Reflect Its Underlying Earnings Potential

As a general rule, we think profitable companies are less risky than companies that lose money. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. In this article, we'll look at how useful this year's statutory profit is, when analysing Hong Kong Shanghai Alliance Holdings (HKG:1001).

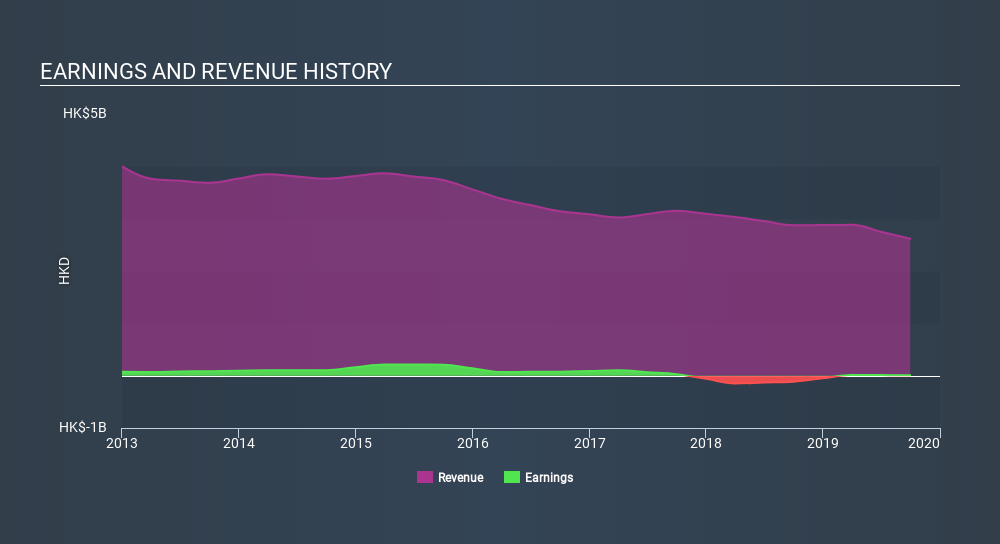

While Hong Kong Shanghai Alliance Holdings was able to generate revenue of HK$2.62b in the last twelve months, we think its profit result of HK$8.22m was more important.

Check out our latest analysis for Hong Kong Shanghai Alliance Holdings

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. This article will focus on the impact unusual items have had on Hong Kong Shanghai Alliance Holdings's statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Hong Kong Shanghai Alliance Holdings.

How Do Unusual Items Influence Profit?

We can't deny that higher profits generally leave us optmistic, but we'd prefer it if the profit were to be sustainable. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. Which is hardly suprising, given the name. Hong Kong Shanghai Alliance Holdings had a rather significant contribution from unusual items relative to its profit to September 2019. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Hong Kong Shanghai Alliance Holdings's Profit Performance

As previously mentioned, Hong Kong Shanghai Alliance Holdings's large boost from unusual items won't be there indefinitely, so its statutory earnings are probably a poor guide to its underlying profitability. As a result, we think it may well be the case that Hong Kong Shanghai Alliance Holdings's underlying earnings power is lower than its statutory profit. On the bright side, the company showed enough improvement to book a profit this year, after losing money last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. While earnings are important, another area to consider is the balance sheet. You can seeour latest analysis on Hong Kong Shanghai Alliance Holdings's balance sheet health here.

This note has only looked at a single factor that sheds light on the nature of Hong Kong Shanghai Alliance Holdings's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:1001

Hong Kong Shanghai Alliance Holdings

Engages in the distribution and processing of construction materials in Hong Kong and Mainland China.

Good value average dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)