Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

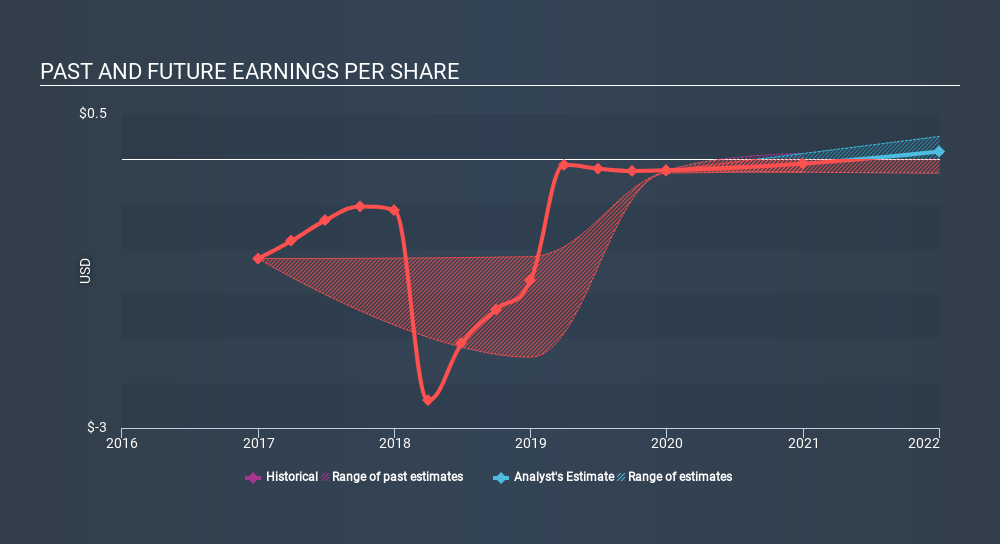

Dropbox, Inc. (NASDAQ:DBX): Is Breakeven Near?

Dropbox, Inc.'s (NASDAQ:DBX): Dropbox, Inc. provides a collaboration platform worldwide. The US$7.7b market-cap company announced a latest loss of -US$52.7m on 31 December 2019 for its most recent financial year result. The most pressing concern for investors is DBX’s path to profitability – when will it breakeven? Below I will provide a high-level summary of the industry analysts’ expectations for DBX.

Check out our latest analysis for Dropbox

According to the 14 industry analysts covering DBX, the consensus is breakeven is near. They expect the company to post a final loss in 2020, before turning a profit of US$36m in 2021. DBX is therefore projected to breakeven around a couple of months from now! What rate will DBX have to grow year-on-year in order to breakeven on this date? Using a line of best fit, I calculated an average annual growth rate of 49%, which is extremely buoyant. Should the business grow at a slower rate, it will become profitable at a later date than expected.

Underlying developments driving DBX’s growth isn’t the focus of this broad overview, but, bear in mind that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before I wrap up, there’s one aspect worth mentioning. DBX currently has no debt on its balance sheet, which is quite unusual for a cash-burning loss-making, growth company, which typically has high debt relative to its equity. This means that DBX has been operating purely on its equity investment and has no debt burden. This aspect reduces the risk around investing in the loss-making company.

Next Steps:

There are too many aspects of DBX to cover in one brief article, but the key fundamentals for the company can all be found in one place – DBX’s company page on Simply Wall St. I’ve also put together a list of important aspects you should further research:

- Valuation: What is DBX worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether DBX is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Dropbox’s board and the CEO’s back ground.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1944.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

56 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.9% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30152.0% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4851.3% undervalued

200 followersusers have followed this narrative

16 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RD

rdiab on Fortinet ·

FTNT Is The Cybersecurity Powerhouse A Buy?

Fair Value:US$125.5628.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PT

PTA on Chipotle Mexican Grill ·

Chipotle Mexican Grill will thrive with a 5% revenue boost

Fair Value:US$27.8822.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75026.5% undervalued

93 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5456.6% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.7% undervalued

56 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0