- United States

- /

- Aerospace & Defense

- /

- NasdaqGS:AXON

Axon Enterprise (AXON) Reports Q2 Revenue Climb To US$669 Million

Reviewed by Simply Wall St

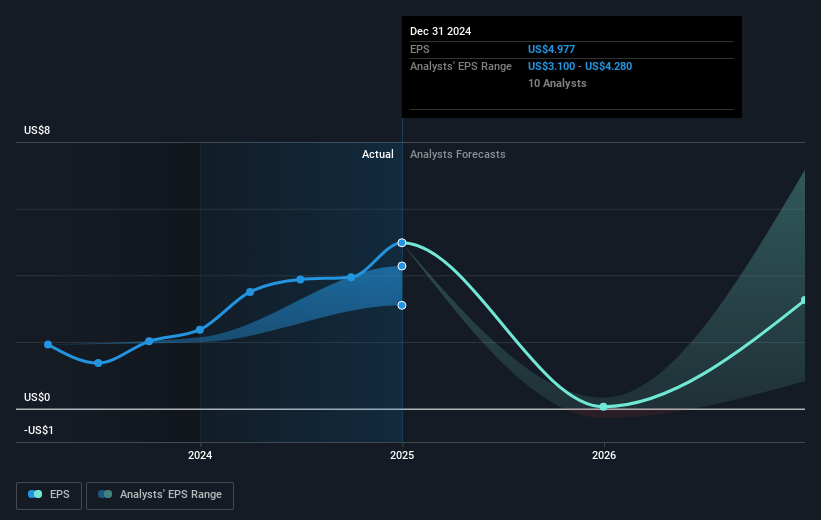

Axon Enterprise (AXON) recently showcased its Q2 results with revenue climbing to $669 million, though net income and earnings per share experienced declines. The company also raised its full-year 2025 revenue guidance, reflecting confidence in future growth prospects. Despite completing part of their share buyback plan, no shares were repurchased in the latest quarter. Over the past quarter, Axon Enterprise's stock rose by 5.1%. This movement aligns with broader market trends where indices reached record highs, and the company's positive guidance would have added weight to these gains, complementing the overall upward market trajectory.

We've spotted 2 risks for Axon Enterprise you should be aware of.

The recent Q2 performance of Axon Enterprise, alongside its raised full-year 2025 revenue guidance, supports the narrative of technology adoption driving customer value and growth. The company's commitment to innovation with advanced tech and SaaS offerings is evident through its efforts in modernizing public safety solutions. However, the lack of share buybacks in the latest quarter might signal a cautious approach towards capital allocation, which could impact future earnings and revenue forecasts, aligning with analyst expectations of moderate profit margin shrinkage.

Over the past five years, Axon's shares delivered a very large total return of 845.55%, reflecting strong long-term investor confidence. In the past year, Axon's share price performance exceeded the US market, which saw a return of 19.4%, highlighting its solid one-year growth compared to broader market trends. However, it underperformed the US Aerospace & Defense industry, which had a higher return of 34.2%. The current share price of US$765.52 sits below the analysts' consensus price target of US$873.67, indicating a potential upside but also portraying varying analyst expectations about future performance.

The company's focus on global expansion and addressing public safety challenges continues to underpin its growth trajectory. The positive reception of their latest products suggests potential for sustained revenue and earnings growth, reinforcing analyst projections. The raised revenue guidance by the company could provide additional momentum, though the competitive landscape and reliance on government funding still pose risks. Despite these factors, the marginal difference between current share pricing and projected targets underscores a consensus on its fair valuation as analysts strive for balanced future outlooks.

Explore Axon Enterprise's analyst forecasts in our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AXON

Axon Enterprise

Develops, manufactures, and sells conducted energy devices (CEDs) under the TASER brand in the United States and internationally.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives