- United Kingdom

- /

- Insurance

- /

- AIM:PGH

4 Days To Buy Personal Group Holdings Plc (LON:PGH) Before The Ex-Dividend Date

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Personal Group Holdings Plc (LON:PGH) is about to trade ex-dividend in the next 4 days. Ex-dividend means that investors that purchase the stock on or after the 21st of May will not receive this dividend, which will be paid on the 26th of June.

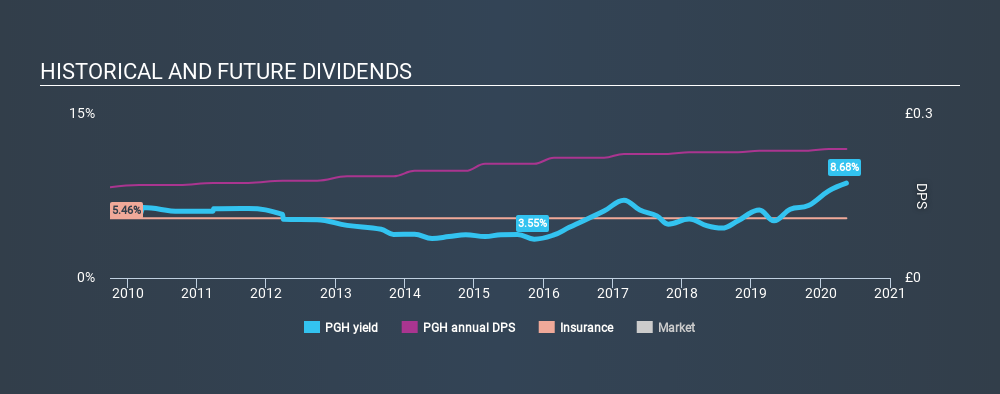

Personal Group Holdings's upcoming dividend is UK£0.015 a share, following on from the last 12 months, when the company distributed a total of UK£0.24 per share to shareholders. Calculating the last year's worth of payments shows that Personal Group Holdings has a trailing yield of 8.7% on the current share price of £2.72. If you buy this business for its dividend, you should have an idea of whether Personal Group Holdings's dividend is reliable and sustainable. So we need to investigate whether Personal Group Holdings can afford its dividend, and if the dividend could grow.

See our latest analysis for Personal Group Holdings

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Its dividend payout ratio is 82% of profit, which means the company is paying out a majority of its earnings. The relatively limited profit reinvestment could slow the rate of future earnings growth. We'd be concerned if earnings began to decline.

Companies that pay out less in dividends than they earn in profits generally have more sustainable dividends. The lower the payout ratio, the more wiggle room the business has before it could be forced to cut the dividend.

Click here to see how much of its profit Personal Group Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. This is why it's a relief to see Personal Group Holdings earnings per share are up 2.4% per annum over the last five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past ten years, Personal Group Holdings has increased its dividend at approximately 3.6% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Is Personal Group Holdings an attractive dividend stock, or better left on the shelf? Earnings per share have been growing at a reasonable rate, and the company is paying out a bit over half its earnings as dividends. It might be worth researching if the company is reinvesting in growth projects that could grow earnings and dividends in the future, but for now we're on the fence about its dividend prospects.

With that being said, if dividends aren't your biggest concern with Personal Group Holdings, you should know about the other risks facing this business. We've identified 2 warning signs with Personal Group Holdings (at least 1 which is a bit unpleasant), and understanding these should be part of your investment process.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About AIM:PGH

Personal Group Holdings

Engages in the provision of employee services and salary sacrifice technology products in the United Kingdom.

Flawless balance sheet with proven track record and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)