Last Update 17 Jun 26

Fair value Increased 11%AA: Higher Margin Outlook And Aluminum Price Tailwinds Will Support Future Upside

Analysts have raised their Alcoa price target from $73.87 to $82.25, citing updated assumptions on fair value, discount rate, revenue growth, profit margins, and future P/E.

What’s in the News for Alcoa

- Alcoa shares dropped nearly 10% after the company revised its Q2 outlook, citing a projected US$60 million unfavorable impact in the Alumina segment from higher production costs at the Pinjarra refinery, cyclone related disruptions, and increased energy prices linked to geopolitical tensions near the Strait of Hormuz. Source: recent Q2 outlook update

- The company expects third party alumina shipments to decline by 120,000 metric tons, while the Aluminum segment is projected to see an approximately US$55 million favorable swing supported by inventory repositioning, higher shipments, and the restart of the San Ciprian smelter. Source: recent Q2 outlook update

- Aluminum prices on the London Metal Exchange recently reached their highest level in over four years, driven by supply disruptions in the Middle East and tensions around the Strait of Hormuz, contributing to a roughly 10% rally in Alcoa stock over five days before subsequent volatility. Source: June 2, 2026 news flow

- Aluminum prices later pulled back to two month lows following a U.S. Iran framework agreement to resume metal shipments and concerns about higher U.S. interest rates, which coincided with a decline in Alcoa shares and added to recent share price swings. Source: June 2, 2026 news flow

- Alcoa reported Q1 2026 production of 9.1 mdmt of bauxite, 2,355 kmt of alumina, and 607 kmt of aluminum and reaffirmed 2026 production and shipment guidance ranges for both the Alumina and Aluminum segments. Source: operating results and 2026 guidance

Valuation Changes for Alcoa Stock

- Fair Value: updated from $73.87 to $82.25, reflecting a higher assessed valuation level for Alcoa shares.

- Discount Rate: nudged higher from 8.81% to 8.93%, indicating a slightly higher required return in the updated model.

- Revenue Growth: revised from 5.67% to 5.88%, a modest upward adjustment in projected top line expansion assumptions for Alcoa.

- Net Profit Margin: reduced from 12.98% to 12.04%, signaling slightly lower assumed profitability on future earnings.

- Future P/E: increased from 13.65x to 16.41x, implying a higher valuation multiple applied to projected earnings in the new assessment.

Key Takeaways

- Rising use of recycled aluminum and competitive lightweight materials, plus global supply growth, threaten Alcoa's long-term demand and the reliability of growth projections.

- Ongoing tariff volatility, regulatory pressures, operational bottlenecks, and limited production flexibility could compress margins and elevate future costs.

- Decarbonization trends, supply constraints, and sustainable product innovation position Alcoa for stronger pricing, improved margins, and resilient long-term growth amid shifting global demand.

Catalysts

About Alcoa- Engages in the bauxite mining, alumina refining, aluminum production, and energy generation business in Australia, Brazil, Canada, Iceland, Norway, Spain, the United States, and internationally.

- Growing adoption of recycled aluminum and substitute lightweight materials in automotive and construction could erode long-term demand growth for primary aluminum, making future revenue growth expectations for Alcoa optimistic and possibly contributing to overvaluation.

- Persistent tariff-related market volatility, combined with Alcoa's contractual obligations limiting its ability to flexibly redirect Canadian production, may compress net margins for several quarters, especially if regional price premiums fail to fully offset heightened costs.

- Delays in securing new mine approvals in Western Australia could increase operational risk and future production costs if existing reserves are depleted faster than anticipated, potentially weighing on long-term earnings growth.

- Stagnation or further decline in aluminum prices due to global supply increases from China, India, and the Middle East, coupled with uncertain recovery in key end markets like automotive, challenges the sustainability of current revenue and EBITDA projections.

- Increasing regulatory and environmental compliance requirements, alongside aging asset maintenance-without sufficient downstream diversification-raise the risk of elevated long-term costs, potentially pressuring net margins and deteriorating free cash flow.

Alcoa Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

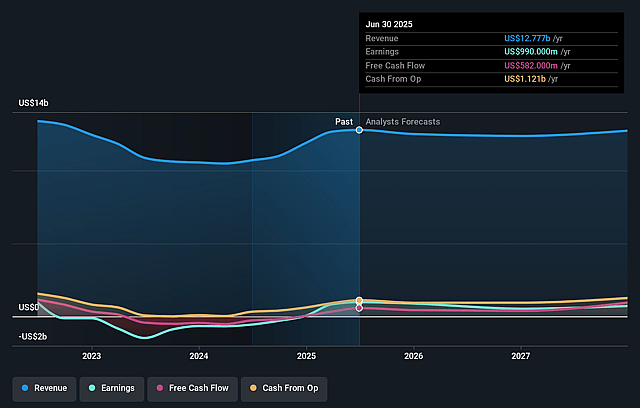

- Analysts are assuming Alcoa's revenue will grow by 5.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.1% today to 12.0% in 3 years time.

- Analysts expect earnings to reach $1.8 billion (and earnings per share of $6.03) by about June 2029, up from $1.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $3.3 billion in earnings, and the most bearish expecting $926.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 16.4x on those 2029 earnings, up from 16.2x today. This future PE is lower than the current PE for the US Metals and Mining industry at 18.8x.

- Analysts expect the number of shares outstanding to grow by 1.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.93%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Strong long-term demand drivers-including the global push for decarbonization, accelerating adoption of electric vehicles, infrastructure investments, and growth in renewable energy-are expected to significantly boost aluminum demand, supporting Alcoa's future revenues and reducing downside risk to long-term top-line growth.

- Alcoa's successful development and commercialization of its EcoLum low-carbon aluminum products and the ELYSIS zero-carbon smelting process position the company to capture premium pricing and greater market share as customers and regulators increasingly prioritize sustainability, which could sustain or expand profit margins over time.

- Tightening global aluminum supply, driven by production curtailments in China, disruptions in bauxite supply (particularly in Guinea), and new capacity constraints, may improve pricing power and reduce risk of persistent overcapacity and margin pressure-thereby supporting higher ASPs, revenues, and earnings for Alcoa.

- Alcoa's ongoing operational initiatives-such as upstream portfolio optimization, cost control programs, and contingency plans for mining approvals-are expected to improve efficiency and cushion EBITDA margins and free cash flow, providing greater resilience against near-term market volatility.

- Positive long-term geographic shifts, with North America and emerging markets projected to have higher aluminum demand growth rates than China, provide Alcoa with robust opportunities to grow shipment volumes, increase utilization of its assets, and support stronger revenue and profit recovery.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $82.25 for Alcoa based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $152.0, and the most bearish reporting a price target of just $52.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $15.0 billion, earnings will come to $1.8 billion, and it would be trading on a PE ratio of 16.4x, assuming you use a discount rate of 8.9%.

- Given the current share price of $62.87, the analyst price target of $82.25 is 23.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Alcoa?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.