Last Update 10 Jul 26

Fair value Decreased 2.18%GPN: Worldpay Integration And FY26 Framework Are Expected To Drive Repricing

Global Payments' updated analyst price target edges lower to $92.56, as analysts weigh more cautious assumptions around travel driven revenue, integration risk and slightly lower projected P/E multiples across upcoming periods.

Analyst Commentary

Recent Street research on Global Payments shows a split view, with some analysts seeing the recent pullback as overdone while others focus on execution risk, travel related uncertainty and a more conservative growth outlook into 2026.

Bullish Takeaways

- Bullish analysts view the recent double digit share price decline as disproportionate to any changes in Global Payments' messaging, suggesting sentiment has weakened faster than fundamentals.

- Some see the Worldpay combination as reinforcing Global Payments' role as a pure play acquirer. They argue this could support longer term scale and earnings power if integration is executed effectively.

- Several updated price targets, even after cuts into the US$90 to US$110 range, still sit above recent trading levels. This indicates room in their models for execution on the current outlook.

- A portion of the Street expects Q2 to land roughly in line with current expectations and views current guidance reaffirmations as a sign that management is not signaling a reset in the near term.

Bearish Takeaways

- Bearish analysts are trimming Q2 and fiscal 2026 estimates, citing travel related headwinds tied to the Middle East conflict and questioning whether Global Payments' assumption of normalized travel by the end of Q2 is realistic.

- Several firms have reduced price targets, in some cases into the US$65 to US$95 range, reflecting more cautious P/E assumptions and lower modeled growth across the second half and into 2026.

- Concerns remain around integration risk from Worldpay, legacy technology debt and earnings quality. Some argue that added scale alone may not improve Global Payments' competitive position or revenue trajectory.

- A subset of the Street is maintaining Neutral or Hold style ratings. This signals that they see limited near term catalysts for multiple expansion until there is clearer evidence on travel trends and delivery against the 2026 framework.

What's in the News for Global Payments

- Analyst commentary highlights Global Payments as one of the Top 10 "Extreme Value" stocks, with Wells Fargo's Jason Kupferberg maintaining a Buy rating and a price target that implies 33% potential upside, while other analysts reduce quarterly earnings estimates due to travel related headwinds linked to the Middle East conflict (source: recent analyst reports summarized in news flow).

- Global Payments reiterates an assumption that travel demand could normalize by the end of Q2 and has issued guidance for fiscal 2026 that includes anticipated revenue growth and higher adjusted earnings per share. This indicates management's stated confidence in its longer term framework (source: company guidance cited in news reports).

- The company completed its US$24b acquisition of Worldpay in January 2026, expanding its merchant base and payment volume and reinforcing Global Payments' focus on scaling transaction volume in digital payments. It is continuing to invest in technology and partnerships amid competition and rising operating costs (source: Worldpay acquisition coverage).

- Global Payments stock recorded a 22% gain over a 7 day period in early July 2026, lifting market capitalization by about US$3.9b to around US$21b. Some third party metrics such as a GF Value estimate of US$126.72 and a GF Score of 84/100 are cited in the news as indicators of potential undervaluation and strong growth and profitability, alongside moderate financial strength and higher perceived risk (source: recent share price performance analysis).

- Recent company updates also highlight new and expanded client and product activity, including the Worldpay powered partnership with Lightspeed DMS for embedded payments, the exclusive U.S. POS and in store payment solutions agreement with CKE Restaurants for its Hardee's and Carl's Jr. locations, and the launch of AI first Genius handheld and kiosk configurations showcased at the National Restaurant Association Show. Together, these point to ongoing product development and enterprise wins for Global Payments (source: company announcements).

Valuation Changes for Global Payments

- Fair Value: The updated model fair value for Global Payments has edged lower from $94.62 to $92.56, a reduction of about 2.2%.

- Discount Rate: The discount rate has been trimmed slightly from 9.34% to 9.14%, reflecting a modest adjustment to the required return used in the analysis.

- Revenue Growth: Projected revenue growth has been adjusted fractionally from 16.19% to 16.16%, keeping expectations broadly stable.

- Net Profit Margin: The forecast net profit margin is effectively unchanged, remaining at 16.28% in the latest update.

- Future P/E: The future P/E assumption has been revised down from 18.32x to 17.84x, indicating a slightly lower valuation multiple applied to Global Payments in forward periods.

Key Takeaways

- Integrated platforms, strategic acquisitions, and tech investments are enhancing Global Payments' growth, margin expansion, and competitive positioning in digital and cross-border payments.

- Strong demand from small and mid-sized businesses and operational transformations are expected to drive recurring revenues, improved client retention, and expanded market share.

- Ongoing divestitures, integration risks, and rising competition threaten revenue stability, margin expansion, and the company's ability to adapt amid regulatory and technological disruption.

Catalysts

About Global Payments- Provides payment technology and software solutions for card, check, and digital-based payments in the Americas, Europe, and the Asia-Pacific.

- The expanding rollout of the Genius integrated POS platform across the US and international markets positions Global Payments to capitalize on the ongoing movement from cash to digital payments and e-commerce growth, likely supporting accelerating revenues and new market share wins.

- Robust demand for integrated payment and software bundles, especially for small and mid-sized businesses (SMBs), is expected to drive higher recurring SaaS-like revenue streams and improved net margins through operating leverage, as evidenced by increased sales productivity and strong ISV partner growth.

- Cross-border payment capabilities are being enhanced through acquisitions (e.g., APAC-focused digital wallet/QR software) and expanded international distribution, enabling Global Payments to address the rising need for real-time, frictionless payments in global trade-supporting future transaction volume and revenue growth.

- The Worldpay acquisition and operational transformation program are creating scale benefits, cost efficiencies, and significant cross-selling opportunities (e.g., selling Genius into Worldpay's merchant base); these are expected to boost earnings growth and margin expansion after integration.

- Investments in cloud-based infrastructure, AI-powered fraud prevention, marketing automation, and streamlined customer onboarding are reducing churn, improving client stickiness, and enabling faster product launches, which will likely aid both revenue growth and net margin improvement over the next several years.

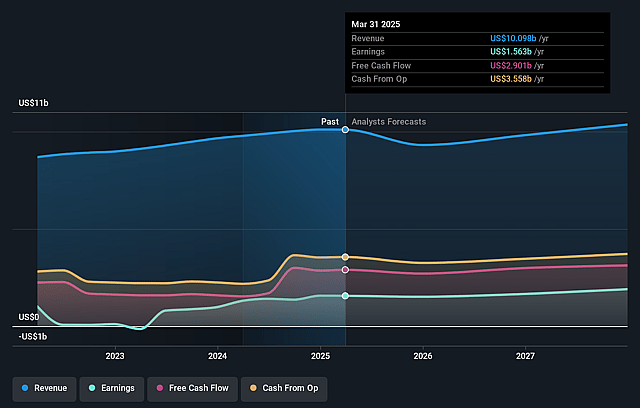

Global Payments Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Global Payments's revenue will grow by 16.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.1% today to 16.3% in 3 years time.

- Analysts expect earnings to reach $2.3 billion (and earnings per share of $9.95) by about July 2029, up from $630.2 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $3.3 billion in earnings, and the most bearish expecting $1.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 17.8x on those 2029 earnings, down from 33.0x today. This future PE is greater than the current PE for the US Diversified Financial industry at 16.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.14%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on large-scale acquisitions like Worldpay, along with portfolio divestitures (e.g., payroll and issuer solutions), heightens integration and execution risk, which could potentially lead to operational disruption, integration challenges, and possible goodwill impairment-negatively impacting both revenue stability and long-term earnings growth.

- Increasing adoption of alternative, decentralized payment solutions and the rise of embedded finance models could erode merchant reliance on third-party payment processors, structurally compressing industry-wide fees and threatening future revenue and margin expansion.

- Margin pressures could intensify over time due to increased competition from fintech upstarts, legacy banks, and direct merchant network connections, particularly as merchants focus on optimizing payment acceptance costs, which may reduce net margins.

- Ongoing global regulatory changes and data privacy requirements across jurisdictions (such as strengthening data protection acts and emerging CBDCs/digital rails) could drive higher compliance costs and introduce uncertainty that would compress earnings and complicate international expansion.

- Sustained divestitures (over $550 million annualized revenue already divested and the potential for more post-Worldpay) and portfolio shifts may thin the company's long-term revenue base, lessen diversification, and increase exposure to secular risk in key verticals, challenging the company's ability to grow and maintain resilient free cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $92.56 for Global Payments based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $194.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $13.9 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 17.8x, assuming you use a discount rate of 9.1%.

- Given the current share price of $76.04, the analyst price target of $92.56 is 17.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Global Payments?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.