Last Update 01 May 26

ARVN: Early Neurology Readouts And Cash Runway Will Drive Bullish Repricing

Analysts have nudged Arvinas' implied price target higher by a few dollars per share, reflecting updated models after recent Q4 results, early approval for Vepdeg, and a fuller view of the upcoming data cycle for programs like ARV-102 and other 2026 readouts.

Analyst Commentary

Recent Street research on Arvinas clusters around early approval for Vepdeg, the updated Q4 models, and a more detailed path for ARV-102 and other 2026 data events. Price targets in the reports cited here sit in a range of $11 to $20 per share, with analysts split between more enthusiastic and more reserved stances.

Bullish Takeaways

- Bullish analysts view early approval for Vepdeg as a key milestone that helps frame Arvinas as a commercial-stage story rather than purely a development-stage name. This, in their models, feeds into higher valuations.

- Several updated models after the Q4 report explicitly tie higher price targets to the clearer timeline of data readouts through 2026, including ARV-102. In their view, this improves visibility on the pipeline's potential contribution to long term growth.

- Some bullish analysts highlight the company's reported cash balance of $685.4m at the end of 2025, which they see as providing funding into the second half of 2028 and reducing near term financing risk in their valuation work.

- Planned ARV-102 milestones, including data in Parkinson's disease patients and potential progression toward a registrational trial, are cited as key execution markers that, if met, could support the higher price target range these analysts put forward.

Bearish Takeaways

- More cautious analysts maintain Neutral stances even as they adjust targets higher. They point to the need for further clinical clarity across the Phase 1 pipeline before taking a more constructive view on long term growth.

- These bearish analysts flag that, despite upcoming ARV-102 data and conference presentations, the programs are still early. As a result, they temper valuation assumptions until there is more evidence on safety and efficacy in patients.

- There is an emphasis on execution risk around the busy 2026 readout calendar, where timing, quality of data, and regulatory interactions could all influence whether Arvinas ultimately tracks closer to the upper or lower end of the current target range.

- Some cautious commentary frames the current target prices as already factoring in a meaningful amount of future pipeline success. In their view, this limits upside until new results justify revisiting the models again.

What's in the News

- Arvinas presented Phase 1 multiple dose data for ARV-102 in Parkinson's disease at AD/PD 2026 in Copenhagen, with approximately 50% or greater LRRK2 reduction in cerebrospinal fluid at all doses by day 14 and sustained through day 28, along with dose dependent CSF exposure and peripheral LRRK2 degradation. (Key Developments)

- In the same Phase 1 trial, ARV-102 was reported as generally safe and well tolerated over 28 days of daily dosing at 20 mg, 40 mg, and 80 mg, with only mild treatment emergent and treatment related adverse events and no serious adverse events, discontinuations, or deaths. (Key Developments)

- Biomarker data from the ARV-102 study showed reductions in endolysosomal and neuroinflammatory proteins such as CD68 and GPNMB, which are described as elevated in LRRK2 related Parkinson's disease and progressive supranuclear palsy. Arvinas plans further investigation of ARV-102 in neurodegenerative diseases associated with LRRK2 and endolysosomal dysfunction. (Key Developments)

- From October 1, 2025 to December 31, 2025, Arvinas repurchased 7,449,728 shares for US$70.73 million, completing a total of 10,009,758 shares repurchased for US$90.97 million under the buyback announced on September 17, 2025. This represents 14.01% of shares. (Key Developments)

- Arvinas appointed Randy Teel, Ph.D., as Chief Executive Officer effective February 12, 2026, succeeding John Houston, Ph.D., who is retiring from the CEO role and remaining on the Board while providing consulting and advisory services to the company. (Key Developments)

Valuation Changes

- Fair Value: $14.88 is unchanged, with the updated model keeping the same implied per share estimate as before.

- Discount Rate: 6.98% is effectively flat, suggesting no material adjustment to the assumed risk profile in the model.

- Revenue Growth: The long term revenue growth assumption remains at an annual 15.08% decline, with no practical change in the updated inputs.

- Net Profit Margin: The projected net profit margin has eased slightly from 19.89% to 19.44%, indicating a modestly more conservative view on future profitability.

- Future P/E: The future P/E multiple has risen slightly from 29.0x to 29.7x, pointing to a marginally higher valuation multiple being applied to expected earnings.

Key Takeaways

- Advancements in targeted therapies and partnerships position Arvinas to capitalize on precision medicine trends and diversify future revenue streams.

- Streamlined operations and supportive industry momentum enhance prospects for improved margins and faster approval timelines.

- Cost-cutting measures, strategic pipeline shifts, and external commercialization uncertainties heighten risks to innovation, growth, and long-term profitability amid rising competition and industry headwinds.

Catalysts

About Arvinas- A clinical-stage biotechnology company, engages in the discovery, development, and commercialization of therapies to degrade disease-causing proteins.

- Arvinas is positioned to benefit from a growing addressable market due to the rapid aging of the global population and the increasing prevalence of diseases like cancer and neurodegeneration, directly driving long-term potential for revenue growth as more patients seek innovative therapies.

- The company's continued advancements in targeted and personalized therapies, specifically through its differentiated PROTAC platform and new clinical-stage assets such as ARV-102 (for Parkinson's/PSP), ARV-393 (BCL6 degrader), and ARV-806 (KRAS degrader), align with healthcare's shift toward precision medicine and expand opportunities for future high-margin product launches.

- Solid progress and early validation in partnerships and licensing, as seen with Novartis and ongoing collaboration (or renegotiation) with Pfizer, offer the potential for substantial milestone payments and tiered royalties, thus strengthening future earnings and diversifying revenue streams.

- Operational efficiencies executed via company-wide restructuring, strategic pipeline prioritization, and workforce reduction have significantly extended Arvinas' cash runway to 2028, improving the sustainability of R&D and positioning net margins for improvement even ahead of potential major product approvals.

- Industry-wide momentum, including increased M&A and biopharma investment in targeted protein degradation and more supportive regulatory frameworks for breakthrough therapies, are expected to accelerate Arvinas' approval timelines, pipeline value realization, and drive overall earnings uplift as the sector re-rates innovators.

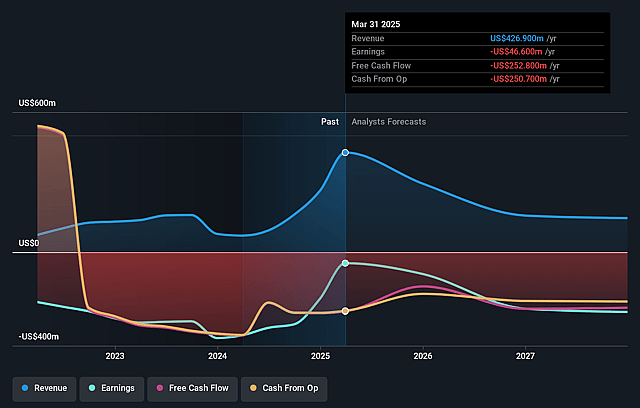

Arvinas Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Arvinas's revenue will decrease by 15.1% annually over the next 3 years.

- Analysts are not forecasting that Arvinas will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Arvinas's profit margin will increase from -30.8% to the average US Pharmaceuticals industry of 19.4% in 3 years.

- If Arvinas's profit margin were to converge on the industry average, you could expect earnings to reach $31.3 million (and earnings per share of $0.61) by about May 2029, up from -$80.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $218.4 million in earnings, and the most bearish expecting $-355.5 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 30.0x on those 2029 earnings, up from -7.8x today. This future PE is greater than the current PE for the US Pharmaceuticals industry at 16.1x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.98%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The recent restructuring resulted in cutting one-third of Arvinas' workforce, reprioritizing the pipeline, and reducing R&D expenses, reflecting a need to conserve cash that may constrain innovation and slow future program growth, potentially limiting long-term revenue and earnings expansion.

- Uncertainty around vepdeg's commercialization path, including ongoing negotiations with Pfizer over development rights and no near-term plan for internal commercial infrastructure, raises the risk of delays or gaps in market launch, which could suppress anticipated revenue streams and earnings from their lead asset.

- Heavy reliance on the unproven PROTAC platform and early-stage pipeline exposes Arvinas to significant R&D and regulatory risks; if pivotal clinical trials disappoint or timelines slip, this could result in prolonged negative net margins and increased cash burn.

- Increasing competition in the targeted protein degradation and oncology space-including large pharma and other biotechs with advanced programs-may erode potential market share, threaten pricing power, and compress long-term revenue and profitability prospects.

- Broader industry and policy trends such as global drug price regulation, rising cost of capital, and potential supply chain disruptions could heighten margin pressure and operational expenses, impacting long-term earnings and Arvinas' ability to sustain profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $14.88 for Arvinas based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $21.0, and the most bearish reporting a price target of just $6.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $160.8 million, earnings will come to $31.3 million, and it would be trading on a PE ratio of 30.0x, assuming you use a discount rate of 7.0%.

- Given the current share price of $9.9, the analyst price target of $14.88 is 33.4% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Arvinas?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.