Last Update 22 Jun 26

PRCH: Capital Optimization And Coverage Resumption Will Support Future Upside Potential

Analysts have modestly raised their average price target on Porch Group by $1, supported by recent resumed coverage and updated research that reiterates a constructive view on the stock's long term prospects.

Analyst Commentary

Recent research coverage on Porch Group reflects a generally constructive stance, with analysts updating their work to support the revised price targets and long term view on the stock.

Bullish Takeaways

- Bullish analysts frame the resumed coverage as a sign that Porch Group remains investable in their view, with enough visibility on the business to support refreshed models and a new price framework.

- The incremental US$1 move in average price target is being used by bullish analysts to signal that they see room for upside relative to where the stock is trading today.

- Supportive commentary focuses on Porch Group's ability to execute on its business plan over time, which these analysts see as important for justifying current and potential valuation multiples.

- Constructive views emphasize that, with updated research in hand, the risk or reward profile looks acceptable for investors who are comfortable with execution risk and are focused on long term growth potential.

Bearish Takeaways

- Bearish analysts or more cautious readers of the research may view the modest US$1 price target change as limited conviction, suggesting expectations are being fine tuned rather than reset meaningfully.

- The reliance on long term prospects leaves shorter term execution and market conditions as open questions, which can matter for how Porch Group trades relative to target prices.

- Some investors may see the need for resumed coverage and updated work as a reminder that the story still depends heavily on future execution, which can constrain how much they are willing to pay on P/S or other valuation metrics today.

- The constructive tone in research does not remove the possibility that Porch Group could underperform expectations if growth, profitability or operational milestones do not track to the assumptions built into these updated targets.

What’s in the News for Porch Group

- Porch Group agreed to repurchase approximately 2.1 million shares of its common stock from Porch Reciprocal Exchange for US$15 million in cash, according to recent news reports.

- The transaction converts Porch Reciprocal Exchange’s stock holdings into liquid assets, which the reports state is intended to increase the Reciprocal’s statutory surplus and improve its regulatory capital position.

- After the sale, Porch Reciprocal Exchange continues to hold about 16.2 million Porch Group shares, so it still has exposure to any future share price movements, based on the same reports. (Source: recent news coverage of Porch Group Repurchases 2.1 Million Shares from Porch Reciprocal Exchange for $15 Million to Boost Capital)

- Separate company disclosures show that Homeowners of America, part of Porch Group’s insurance platform, has launched in Michigan, which is the 22nd state in which HOA operates. (Source: company key developments)

Valuation Changes for Porch Group

- Fair Value: Model fair value remains unchanged at $16.25 per share, indicating no revision to the central valuation output.

- Discount Rate: The discount rate has fallen slightly from 9.46% to 9.39%, reflecting a modest adjustment to the required return used in the valuation model.

- Revenue Growth: The revenue growth assumption is essentially unchanged at about 10.48%, with only an immaterial numerical refinement in the updated model.

- Net Profit Margin: The profit margin assumption remains effectively stable at about 7.62%, with the revised figure differing only in rounding.

- Future P/E: The future P/E multiple has edged down slightly from 52.40x to 52.30x, implying a marginally lower valuation multiple applied to Porch Group’s projected earnings.

Key Takeaways

- Porch Group's shift to a fee-based insurance model and formation of PIRE create a higher-margin, more predictable earnings structure.

- Strategic investments in software, data, and new geographies aim to boost future revenue and EBITDA growth, leveraging products like Home Factors.

- Porch Group faces potential revenue volatility and execution risks due to delayed initiatives and a transition to a commission-based model, impacting future earnings and growth.

Catalysts

About Porch Group- Operates a vertical software and insurance platform in the United States.

- Porch Group's transition to a fee-based, higher-margin model in insurance services should enhance gross margins to about 80% in 2025, making earnings more predictable and less impacted by weather volatility, thereby improving net margins.

- The formation of the Porch Insurance Reciprocal Exchange (PIRE) and the sale of Homeowners of America (HOA) Insurance Carrier into PIRE create a more predictable and higher-margin financial model, which could lead to improved earnings.

- Porch Group's strategic plans include reopening geographies and reactivating distribution partners, contributing to expected growth in gross written premiums, which could drive revenue and adjusted EBITDA growth.

- The company is investing in expanding its Vertical Software and data businesses, with initiatives such as new product launches and increased sales and product investments poised to drive faster revenue growth in 2026 and beyond.

- The introduction and expected growth of Home Factors, a data product which aids in risk selection and pricing, present new revenue opportunities and could significantly enhance the value of Porch Group's data segment, thereby impacting future revenue growth.

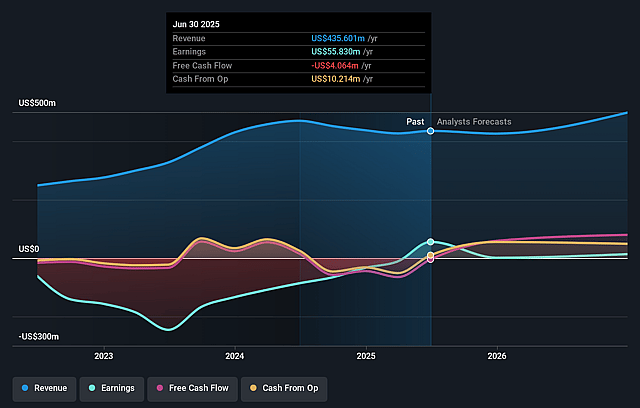

Porch Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Porch Group's revenue will grow by 10.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -3.3% today to 7.6% in 3 years time.

- Analysts expect earnings to reach $51.2 million (and earnings per share of $0.32) by about June 2029, up from -$16.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 52.5x on those 2029 earnings, up from -82.2x today. This future PE is greater than the current PE for the US Software industry at 25.9x.

- Analysts expect the number of shares outstanding to grow by 4.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.39%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Porch Group's revenue in Q4 2024 decreased by 12% year-over-year due to nonrecurring items and the sale of their legacy agency, EIG, which could indicate potential volatility in future revenues.

- The formation of the Porch Insurance Reciprocal Exchange (PIRE) and sale of their Homeowners of America Insurance Carrier were delayed longer than anticipated, signaling potential execution risks which may impact revenue predictability.

- The company’s transition to a commission and fee-based insurance services model could result in lower revenue year-over-year, suggesting potential challenges in offsetting the reduction with higher margins.

- While Porch Group’s strategic price increases in their Vertical Software business showed a 6% growth, it could face challenges in maintaining these growth levels if the housing market does not stabilize, which could impact net margins.

- Porch's ambitious targets for growth in the homeowners insurance market and the new Home Factors product depend heavily on execution and adoption by third-party carriers. Delays or difficulties in realization of these strategies could adversely impact earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $16.25 for Porch Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $672.6 million, earnings will come to $51.2 million, and it would be trading on a PE ratio of 52.5x, assuming you use a discount rate of 9.4%.

- Given the current share price of $12.38, the analyst price target of $16.25 is 23.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Porch Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.