Last Update 06 Jul 26

Fair value Decreased 7.69%PRCH: Elevated Execution Risks Will Pressure Confidence In Future Profitability

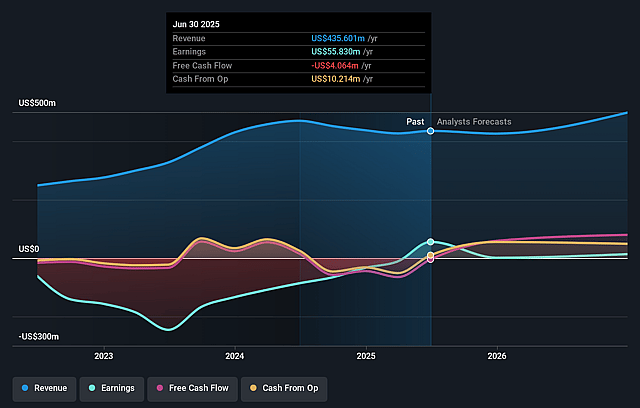

Analysts have reduced their fair value estimate for Porch Group from $13.00 to $12.00, reflecting updated views on the discount rate, revenue growth, profit margin, and future P/E following recent research coverage and price target adjustments.

Analyst Commentary

Recent Street research on Porch Group has centered on updated price targets and the risk profile around execution, revenue growth and long term profitability. While some research has reiterated constructive views, bearish analysts remain cautious about how current valuation lines up with these operational challenges.

Across the latest reports on Porch Group, the discussion has focused on how assumptions for revenue, margins and future P/E multiples feed into fair value estimates. The revised US$12.00 fair value highlights that even modest changes in these inputs can have a meaningful impact on what analysts see as a reasonable price level for the stock.

Bearish analysts are paying close attention to whether Porch Group can deliver on growth expectations without putting additional pressure on profitability. Their commentary often points to execution risks around scaling the business model, as well as uncertainty over how quickly the company can convert revenue growth into sustainable earnings.

For investors, these mixed views emphasize the importance of understanding how different research teams are treating key variables such as discount rates, margin profiles and terminal valuation multiples when assessing Porch Group.

Bearish Takeaways

- Bearish analysts highlight that the lower fair value estimate of US$12.00 leaves less room for error if Porch Group falls short on revenue growth or margin improvement targets.

- There is concern that current valuation already reflects ambitious assumptions for future P/E, which could be challenged if execution on profitability or cash flow is slower than expected.

- Cautious commentary points to the sensitivity of Porch Group’s valuation to discount rate assumptions, with higher required returns leading to reduced fair values.

- Some bearish views focus on the risk that any slip in operational performance or guidance could prompt further price target revisions, especially if revenue or margin trends do not align with existing models.

What’s in the News for Porch Group

- Porch Group, through its subsidiary Homeowners of America, launched operations in Michigan, marking the 22nd state in which HOA operates. (Source: Key Developments)

- The Michigan launch is described as supporting Porch Group’s broader plan to expand insurance distribution across more states. (Source: Key Developments)

- Management commentary around the launch highlights a focus on growing insurance premiums and cash flow over time through Porch Group’s insurance platform. (Source: Key Developments)

Valuation Changes for Porch Group

- Fair Value: Reduced from $13.00 to $12.00, a decline of about 7.7% in the updated model.

- Discount Rate: Adjusted from 9.50% to roughly 9.24%, a small reduction in the required return input.

- Revenue Growth: Revised from about 13.56% to roughly 13.03%, a modest reduction in assumed growth.

- Net Profit Margin: Increased from around 4.42% to about 12.11%, a large uplift in the margin assumption used.

- Future P/E: Brought down from roughly 50.5x to about 22.6x, indicating a much lower valuation multiple in the updated analysis.

Catalysts

About Porch Group

Porch Group operates an integrated home services and insurance platform that leverages proprietary property data, software and partnerships to deliver high margin insurance and home solutions.

What are the underlying business or industry changes driving this perspective?

- Although the company has built a substantial surplus position at the reciprocal that can support materially higher premium volumes, slower than anticipated expansion into new states and cautious pricing decisions could delay the realization of the implied capacity and cap near term revenue growth and EBITDA expansion.

- While industry wide digital transformation and the adoption of data driven underwriting support demand for Porch Group's Home Factors and AI enabled analytics, extended carrier testing cycles and slower commercialization could temper the contribution from data licensing and limit incremental high margin Software and Data revenue in 2026 and beyond.

- Although the structural shift toward outsourced vertical SaaS in the housing ecosystem positions the software portfolio for operating leverage when housing activity recovers, a prolonged trough in U.S. housing transactions or only a muted rebound would constrain transaction based volumes and slow improvement in segment level net margins.

- While the company has demonstrated the ability to drive industry leading loss ratios through granular property insights and selective risk appetite, relying too heavily on ultra low loss ratios rather than judiciously trading some margin for growth could underutilize surplus and result in flatter long term earnings growth than its capital base would otherwise support.

- Although expanding agency appointments and partnerships with large national distributors create a broader top of funnel aligned with growing consumer reliance on intermediated insurance distribution, execution risk in ramping agent productivity and managing incentive structures could limit premium scale and keep consolidated earnings below the potential implied by current distribution breadth.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Porch Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Porch Group's revenue will grow by 13.0% annually over the next 3 years.

- The bearish analysts are not forecasting that Porch Group will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Porch Group's profit margin will increase from -3.3% to the average US Software industry of 12.1% in 3 years.

- If Porch Group's profit margin were to converge on the industry average, you could expect earnings to reach $87.2 million (and earnings per share of $0.69) by about July 2029, up from -$16.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $122.2 million in earnings, and the most bearish expecting $-5.3 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 22.7x on those 2029 earnings, up from -100.9x today. This future PE is lower than the current PE for the US Software industry at 28.1x.

- The bearish analysts expect the number of shares outstanding to grow by 4.92% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.24%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The strategy of prioritizing surplus generation at the reciprocal over faster premium growth could delay scaling written premiums. If competitive conditions or regulation later constrain pricing power, Porch may miss the optimal window for expansion, putting long term revenue and earnings growth at risk.

- Insurance Services profitability is heavily dependent on exceptionally low gross and attritional loss ratios. If climate trends, severe weather patterns or competitive pressure force Porch to relax underwriting standards or cut prices more aggressively, loss ratios may normalize and compress segment net margins and consolidated earnings.

- Software and Data and Consumer Services remain tied to a trough U.S. housing market and per transaction models. If the expected housing recovery is weaker or more drawn out than anticipated, transaction volumes may stay subdued, limiting diversification away from insurance and slowing consolidated revenue growth and margin expansion.

- The Home Factors and broader data licensing opportunity relies on carriers adopting AI enabled, data driven underwriting. If long sales cycles, integration complexity or slower than expected commercialization persist, high margin data revenue may ramp more slowly than planned, restraining future gross margins and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Porch Group is $12.0, which represents up to two standard deviations below the consensus price target of $16.29. This valuation is based on what can be assumed as the expectations of Porch Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $720.2 million, earnings will come to $87.2 million, and it would be trading on a PE ratio of 22.7x, assuming you use a discount rate of 9.2%.

- Given the current share price of $15.19, the analyst price target of $12.0 is 26.6% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Porch Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.