Catalysts

About Porch Group

Porch Group provides insurance, software, data and home services that focus on homeowners and homebuyers across the moving and homeownership journey.

What are the underlying business or industry changes driving this perspective?

- The insurance platform is built around 89 unique Home Factors and other property data that are not widely available in the market, which management links to industry leading attritional loss ratios of 17% and gross loss ratios of 22%. They state that this supports structurally higher gross margins and the potential for stronger net margins over time.

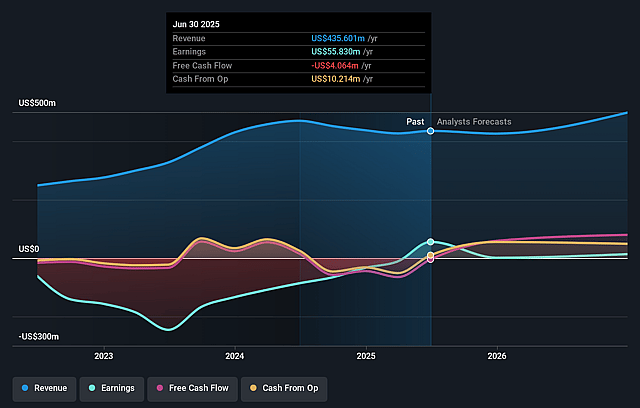

- Surplus at the reciprocal, combined with non admitted assets, reached US$412 million at the end of Q3 2025. Management references a 5:1 premium to surplus rule of thumb that could support about US$2 billion of premium, which they connect to the capacity to support more than US$350 million in annual Insurance Services adjusted EBITDA, directly tied to earnings power.

- The company reports strong top of funnel metrics, including growing agency appointments and quote volumes, with Texas currently around 60% of the book and only a fraction of agencies signed in that state and nationally. Management notes that this points to a long runway to expand distribution and lift revenue as more policies are written.

- Management highlights the ability to flex pricing and incentives along a steep elasticity curve in homeowners insurance, using current margin headroom to selectively lower prices for low risk customers when desired. They describe this as a way to accelerate premium growth while still supporting surplus generation, revenue and Insurance Services margins.

- The Software & Data and Consumer Services segments charge largely per transaction and are currently operating against what management calls a trough U.S. housing market. They state these businesses are set up to grow when housing activity improves, which could add incremental revenue and operating leverage on top of the existing insurance earnings base.

Assumptions

This narrative explores a more optimistic perspective on Porch Group compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

- The bullish analysts are assuming Porch Group's revenue will grow by 16.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 6.9% today to 12.7% in 3 years time.

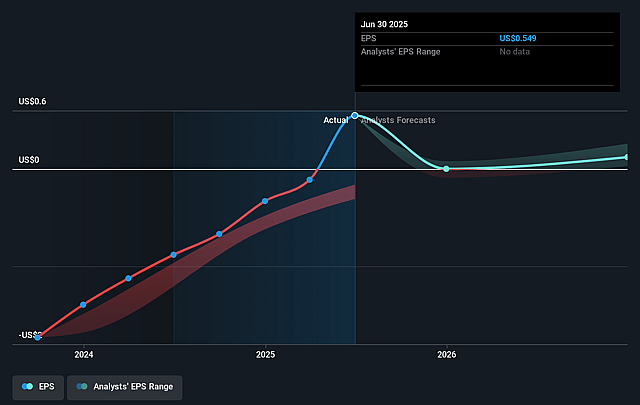

- The bullish analysts expect earnings to reach $87.4 million (and earnings per share of $0.81) by about January 2029, up from $30.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $29.1 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 28.1x on those 2029 earnings, down from 31.8x today. This future PE is lower than the current PE for the US Software industry at 31.7x.

- The bullish analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.56%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Porch Group is heavily reliant on its Insurance Services segment, which contributes 64% of shareholder interest revenue. Any sustained deterioration in industry loss ratios, reinsurance terms or regulatory changes affecting homeowners insurance could pressure pricing power and profitability, which would directly weigh on revenue and adjusted EBITDA.

- The company repeatedly links future upside to a recovery in the U.S. housing market, while also describing current conditions as a trough. If housing transactions stay muted for an extended period, per transaction models in Software & Data and Consumer Services could be constrained, which could limit growth in revenue and reduce operating leverage and net margins.

- Management is choosing to prioritize surplus generation at the reciprocal and to be patient on lowering prices to accelerate premium growth. If competitive pressure or changing consumer behavior later forces price cuts without a corresponding step up in volumes, the combination of lower average premium and higher acquisition incentives could squeeze Insurance Services margins and earnings.

- The insurance model and Home Factors data advantage depend on accurate risk selection and pricing, and management frequently highlights very low attritional and gross loss ratios as a key edge. If new data signals, AI driven insights or underwriting models prove less predictive over time or are matched by peers, loss ratios could shift higher and erode the structurally high gross margin profile, which would affect net margins and earnings.

- Surplus growth at the reciprocal is partly tied to movements in Porch Group’s share price, with 18.3 million shares held at the reciprocal. A prolonged share price decline would reduce surplus value and capital flexibility, which could limit the capacity to support targeted premium levels and in turn cap the Insurance Services contribution to revenue and adjusted EBITDA.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Porch Group is $22.0, which represents up to two standard deviations above the consensus price target of $18.12. This valuation is based on what can be assumed as the expectations of Porch Group's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $22.0, and the most bearish reporting a price target of just $13.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $689.8 million, earnings will come to $87.4 million, and it would be trading on a PE ratio of 28.1x, assuming you use a discount rate of 9.6%.

- Given the current share price of $9.22, the analyst price target of $22.0 is 58.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Porch Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.