Last Update 25 May 26

Fair value Increased 7.02%ROKU: Higher Margin Assumptions And Platform Scale Will Drive Free Cash Flow

Roku's updated analyst price target has been lifted from $158.85 to $170.00 as analysts factor in higher modeled revenue growth, improved profit margins, a lower assumed discount rate, and a recalibrated future P/E of 31.32x.

Analyst Commentary

Recent Street research shows a cluster of bullish analysts lifting Roku price targets, which lines up with the move to a modeled future P/E of 31.32x in the updated valuation. The group includes several large research houses that have adjusted their numbers on Roku within a tight time frame, signaling growing confidence in the company’s ability to support higher earnings assumptions over the forecast period.

Across these reports, bullish analysts are generally framing the new targets around a mix of higher revenue expectations, better margin assumptions, and a lower discount rate applied to Roku’s future cash flows. Together, these inputs help justify a higher fair value range for the stock in their models.

Bullish Takeaways

- Multiple bullish analysts have raised Roku price targets by US$5 to US$32, which supports the view that the updated US$170.00 target sits within a broader rerating of the stock’s valuation multiples.

- The concentration of positive target changes around the same set of research dates suggests improving conviction in execution, particularly on revenue growth and profitability assumptions embedded in forward estimates.

- Several bullish reports referencing Roku price target increases of US$10 to US$30 tie directly to higher modeled operating leverage and margins, which is consistent with the higher future P/E of 31.32x used in the revised framework.

- Incremental raises from firms that already covered Roku, including adjustments in the US$8 to US$32 range, point to analysts revisiting earlier assumptions rather than initiating entirely new views. This can support a more sustained shift in sentiment toward the stock.

For investors, the key thread across these comments is that more bullish analysts are now comfortable underwriting a higher valuation multiple for Roku on the back of updated growth and margin inputs, even if their individual price targets and rating stances differ.

What's in the News

- Roku expanded its subscription aggregation by adding Peacock Premium Plus to The Roku Channel in the U.S., giving viewers access to live sports and the ability to pause and replay live content directly within Roku's interface, with subscriptions priced at US$16.99 per month or US$169.99 per year.

- Apple TV is now available as a Premium Subscription on The Roku Channel in the U.S., allowing customers to subscribe using their Roku account for US$12.99 per month or US$99 per year and stream Apple Originals, films, and live sports in one place.

- Roku launched Howdy, its ad-free SVOD service, as a subscription on Prime Video in the U.S. for US$2.99 per month, extending the service beyond the Roku platform and offering thousands of titles from major content partners.

- Roku became the North American streaming home for the inaugural Enhanced Games, with the event available for free on the Roku Sports Channel across the U.S., Canada, and Mexico, adding another live sports offering to the platform.

- The International Trade Commission opened an investigation into alleged patent infringement involving several companies, including Roku, related to smart televisions and streaming devices, following a complaint filed by InnoTV Labs LLC.

Valuation Changes

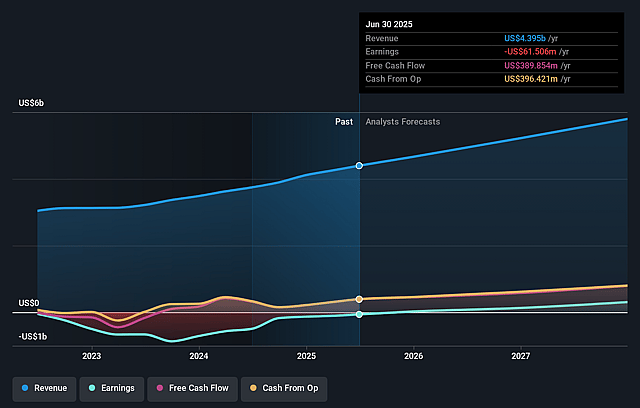

- Fair Value: Updated modeled fair value has risen from $158.85 to $170.00.

- Discount Rate: The discount rate used in the model has fallen slightly from 8.99% to 8.84%.

- Revenue Growth: Assumed long term revenue growth has increased from 14.66% to 16.24%.

- Net Profit Margin: Modeled net profit margin has moved higher from 10.78% to 13.28%.

- Future P/E: Future P/E multiple in the valuation has shifted lower from 42.62x to 31.32x.

Key Takeaways

- Roku's advanced home screen integration, unique ad tools, and global reach position it to capture substantial ad revenue and margin gains as TV budgets shift to connected platforms.

- Expanding first-party content and international growth, combined with increasing engagement and rising ARPU, signal significant long-term recurring revenue and earnings upside.

- Intensifying regulatory, competitive, and structural challenges threaten Roku's future revenue growth and margin expansion despite ongoing investments and a mature user base.

Catalysts

About Roku- Operates a TV streaming platform in the United States and internationally.

- While analyst consensus expects platform revenue growth from home screen optimization, the full power of Roku's home screen is likely still being underestimated-its integration and advanced machine learning recommendations across over half of US broadband households and growing international users could unlock a step-change in both ad and subscription yields, accelerating revenue and margin expansion even beyond current double-digit expectations.

- Analysts broadly agree that expanding SMB-focused ad demand via third-party partnerships and Roku Ads Manager will improve revenue streams, but the addressable market is vastly larger as performance-based video ad budgets migrate from social platforms to CTV; Roku's unique scale and self-serve tools could capture outsized share of a multibillion-dollar market, sharply increasing ad revenues and driving structural margin gains.

- Roku is set to benefit massively from the accelerating shift of TV budgets to connected platforms due to its unrivaled reach, powerful first-party data, and deep integration with global DSPs-positioning the company as the default "gatekeeper" for advertisers, which will both grow top-line ad revenues and boost long-term pricing power, directly impacting net margins.

- The rapid growth and deepening engagement of The Roku Channel (up 80% in hours year-on-year, ranking as a top app globally) indicates that Roku's owned and operated content business has only begun its monetization journey, with rising AVOD and bundled subscription opportunities poised to significantly lift recurring revenue, ARPU, and gross profit in coming years.

- As the integration of smart TVs and home devices becomes ubiquitous worldwide, Roku's OS strategy places it in prime position to scale outside the US, and this global expansion-combined with operational leverage and volume-driven margin improvements-suggests international revenue and earnings could ramp faster than Wall Street anticipates, materially raising long-term earnings power.

Roku Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Roku compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Roku's revenue will grow by 16.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 4.1% today to 13.3% in 3 years time.

- The bullish analysts expect earnings to reach $1.0 billion (and earnings per share of $7.03) by about May 2029, up from $201.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $561.8 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 31.4x on those 2029 earnings, down from 92.0x today. This future PE is greater than the current PE for the US Entertainment industry at 31.0x.

- The bullish analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.84%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Growth in Roku's high-margin advertising business is heavily reliant on continued access to user data, but tightening regulations on data privacy and evolving laws such as GDPR and CCPA could severely limit ad targeting capabilities, putting direct pressure on long-term ad revenue and platform margins.

- Roku's international and U.S. device penetration is already strong, resulting in mature market saturation in developed regions, which means future active account growth may stagnate, making it increasingly difficult to drive incremental improvements in average revenue per user and ultimately curbing revenue expansion potential.

- The company's rising investments in content acquisition, platform development, and integrating acquisitions like Frndly are not guaranteed to produce proportional increases in platform monetization, increasing the risk that climbing operating costs will outpace revenue growth and suppress net margins and earnings over time.

- As mega-cap tech players such as Amazon, Apple, and Google further consolidate their dominance in streaming platforms, operating systems, and advertising, Roku faces intense competition for both platform access and advertising spend, potentially eroding its share of user engagement and digital ad revenue and reducing its overall competitive positioning.

- The shift of major content providers toward their own direct-to-consumer platforms lessens Roku's negotiating leverage and diminishes the appeal of its aggregator model, which may ultimately restrict content diversity and reduce both user engagement and the company's take rate on subscriptions and ad inventory, creating headwinds for sustainable long-term revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Roku is $170.0, which represents up to two standard deviations above the consensus price target of $145.3. This valuation is based on what can be assumed as the expectations of Roku's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $170.0, and the most bearish reporting a price target of just $95.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $7.8 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 31.4x, assuming you use a discount rate of 8.8%.

- Given the current share price of $125.55, the analyst price target of $170.0 is 26.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Roku?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.