Last Update 09 Jul 26

Fair value Decreased 46%FWRD: Cost Discipline And Amazon Partnership Optionality Will Drive Future Share Recovery

Forward Air's updated analyst price target has shifted lower by $15.67 to $18.33, as analysts adjust their assumptions around revenue growth, profit margins, and future P/E following recent research updates from firms that reduced their targets on the stock.

Analyst Commentary

Recent research updates on Forward Air reflect a more cautious stance from Wall Street, with price targets moving lower as analysts revisit their expectations for revenue, margins, and the appropriate P/E multiple for the stock.

Bullish Takeaways

- Bullish analysts still see potential for Forward Air to narrow the gap between current trading levels and their adjusted price targets if execution around cost control and operational efficiency improves.

- Some continue to view the revised targets as accounting for nearer term uncertainty, while still leaving room for upside if revenue trends and profitability track closer to prior expectations.

- There is a view that a lower P/E assumption may already reflect a more conservative outlook, which could appeal to investors who prioritize valuation discipline.

- Supporters of the stock see the recent reset in expectations as creating a clearer bar for management to meet or beat, which may help rebuild confidence over time.

Bearish Takeaways

- Bearish analysts are focusing on the cut in price targets, including reductions of up to double digits in dollar terms, as a sign that earlier growth and margin assumptions may have been too optimistic.

- Concerns center on the risk that Forward Air may face ongoing pressure on revenue growth and profitability, which could limit near term re rating potential for the stock.

- Some see the reset in valuation assumptions, including lower P/E expectations, as a response to execution risks and uncertainty around how quickly the company can stabilize its financial profile.

- The recent target moves are viewed by more cautious voices as a reminder that investors may need to factor in a wider range of outcomes for earnings and cash flow when assessing Forward Air’s current share price.

What’s in the News for Forward Air

- FreightWaves reports that Amazon's new national LTL network could potentially be complemented by acquiring Forward Air, highlighting Forward Air's established time sensitive, national expedited freight platform as a possible fit with Amazon's economy tier offering. Source: FreightWaves, Craig Fuller.

- Forward Air has been dropped from multiple Russell value benchmarks, including the Russell 3000E Value Benchmark, Russell 3000 Value Benchmark, Russell 2500 Value Benchmark, Russell Small Cap Comp Value Benchmark, and Russell 2000 Value Benchmark, reflecting recent index rebalancing decisions.

- The stock has also been removed from several S&P indices, including the S&P Transportation Select Industry Index, S&P 600 Industrials sector, S&P 1000, S&P 600, and the S&P Composite 1500, changing how certain index and passive strategies may gain exposure to Forward Air.

- A proposed US$28,000,000 cash settlement has been announced in the Forward Air Stockholder Litigation, with a class action preliminarily certified for settlement purposes and a settlement hearing scheduled for June 25, 2026, in the Chancery Court for the State of Tennessee, Third Judicial District, Greene County.

- Class members in the Forward Air Stockholder Litigation are being notified of key deadlines, including objection and exclusion dates in mid 2026, and the requirement to file a Proof of Claim by July 10, 2026, to participate in any distribution from the Net Settlement Fund.

Valuation Changes for Forward Air

- Fair Value: The updated fair value estimate has fallen significantly from $34.00 to $18.33, indicating a materially lower assessment of Forward Air's share value.

- Discount Rate: The discount rate has been adjusted slightly lower from 12.5% to 12.46%, a marginal change in the assumed cost of capital.

- Revenue Growth: The projected revenue growth rate has fallen significantly from 4.71% to 2.45%, reflecting more cautious expectations for Forward Air's top line.

- Net Profit Margin: The assumed net profit margin has edged slightly lower from 4.66% to 4.58%, signaling a modest shift in expected profitability.

- Future P/E: The future P/E multiple has been cut sharply from 12.0x to 7.30x, pointing to a lower valuation multiple being applied to Forward Air's earnings outlook.

Key Takeaways

- Recovery in freight volumes, premium services, and focus on e-commerce position the company for future revenue growth and stronger operating margins.

- Integration of Omni Logistics and technology investments are driving synergies, cost savings, and margin expansion, supporting sustained earnings growth.

- Prolonged freight market weakness, reliance on cost controls over organic growth, and costly strategic changes could constrain Forward Air's revenue, margins, and earnings stability.

Catalysts

About Forward Air- Operates as an asset-light freight and logistics company in the United States, Mexico, Europe, Asia, and Canada.

- The normalization and anticipated recovery of freight volumes, along with Forward Air's premium service offering in expedited freight and final-mile logistics, position the company to capitalize on the sustained growth in e-commerce and demand for time-definite delivery solutions-likely supporting future top-line revenue growth and improving operating leverage as volumes rebound.

- Integration of Omni Logistics has driven meaningful synergy gains, cost savings, and commercial opportunities, with the combined network enabling new business wins and enhanced cross-selling, supporting higher consolidated EBITDA margins and long-term earnings growth as integration shifts toward operational transformation.

- Ongoing investment in pricing analytics and network optimization has materially improved segment margins even in a soft market, and positions the company to expand net margins further as market conditions improve and incremental volume is absorbed with minimal additional SG&A expense.

- Forward Air's focus on technology-streamlining systems, optimizing network operations, and improving cost modeling-should drive continued reduction in cost per shipment and improved margin profile, supporting sustainable earnings expansion.

- As domestic supply chains become more complex and customers demand greater resiliency and agility, Forward Air's flexible service offerings and track record for high service levels are likely to enhance customer retention, enable pricing discipline, and improve net revenue stability, particularly as supply chain trends accelerate toward nearshoring and regionalization.

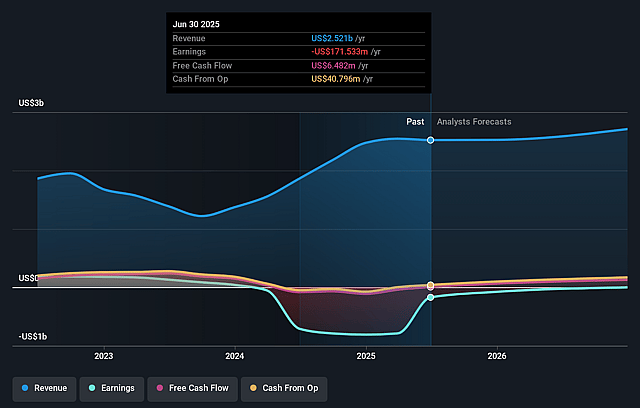

Forward Air Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Forward Air's revenue will grow by 2.5% annually over the next 3 years.

- Analysts are not forecasting that Forward Air will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Forward Air's profit margin will increase from -3.7% to the average US Logistics industry of 4.6% in 3 years.

- If Forward Air's profit margin were to converge on the industry average, you could expect earnings to reach $121.5 million (and earnings per share of $3.54) by about July 2029, up from -$91.5 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 7.4x on those 2029 earnings, up from -4.2x today. This future PE is lower than the current PE for the US Logistics industry at 16.7x.

- Analysts expect the number of shares outstanding to grow by 2.71% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing softness and unpredictability in global freight volumes, referenced as a "current freight recession" with "muted" demand and macroeconomic uncertainty (including tariff and consumer confidence risks), could last longer than expected; if persistent, this would constrain Forward Air's revenue growth and limit margin expansion for an extended period.

- The Expedited Freight segment experienced an 11.5% year-over-year revenue decline on a 12.7% drop in tonnage, with management emphasizing that margin improvement has come from pricing discipline and cost-cutting rather than organic volume growth; without volume recovery, headwinds could emerge for both top-line revenue and sustained profitability.

- Despite successful initial integration, management acknowledged that future margin improvement in key segments relies on network operating leverage and higher shipment volume (i.e., growth in a "tighter" market), implying that if the overall industry shifts toward nearshoring/regionalization, or if automation reduces demand for long-haul LTL services, long-term revenue and net margins may be pressured.

- The company's strategic review and possible portfolio adjustments introduce uncertainty, and while management asserts "the whole is greater than the sum of the parts," any missteps in further transformation, potential divestitures, or acquisition integration could increase operating costs and earnings volatility.

- Continuous need for significant investment in service, technology, and cost optimization (highlighted as "costly and time-consuming"), especially to meet increasing customer service expectations and adapt to changing logistics technology, may create sustained upward pressure on SG&A and capex; if these investments do not translate to proportionate revenue gains, overall earnings and return on capital could decline.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $18.33 for Forward Air based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.6 billion, earnings will come to $121.5 million, and it would be trading on a PE ratio of 7.4x, assuming you use a discount rate of 12.5%.

- Given the current share price of $12.18, the analyst price target of $18.33 is 33.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Forward Air?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.