Last Update 15 May 26

EVGO: Softer 2026 Guide Will Set Stage For Future Stall Acceleration

Narrative Update on EVgo

Analysts have trimmed EVgo's average price target by $0.50 to $3.50, reflecting softer than anticipated guidance and a slightly lower revenue growth outlook. They continue to highlight ongoing network expansion and a longer term investment thesis that remains in place.

Analyst Commentary

Recent Street research on EVgo clusters around lower price targets and more measured expectations, even as many firms maintain positive or neutral ratings. The common thread is that analysts are recalibrating what they are willing to pay for the stock relative to execution risks and the current macro backdrop.

Morgan Stanley, Evercore ISI, RBC Capital, Stifel, Cantor Fitzgerald, Benchmark, UBS, and JPMorgan have all updated their views, with most trimming price targets across a range that now generally spans US$3.50 to US$7. JPMorgan shifted its stance to Neutral from Overweight, while others kept Buy, Outperform, Overweight, or Equal Weight ratings in place despite lower valuation marks.

Several research notes point to a softer than anticipated FY26 guide and a slower stall deployment tempo than some had expected, even as some firms continue to cite a longer term investment case. There is also an explicit acknowledgment from at least one firm that sector-wide valuation pressure and the broader macro environment are influencing the multiples applied to EVgo.

Bearish Takeaways

- Bearish analysts are cutting price targets to levels such as US$3.50, indicating reduced upside assumptions and a more cautious stance on how current fundamentals support previous valuation ranges.

- The downgrade to Neutral at JPMorgan signals rising concern that execution and growth risks could limit near term share performance, even if the long term story is still referenced in research.

- Softer than anticipated FY26 guidance and a lower stall deployment tempo versus some forecasts are feeding worries that growth may track closer to the low end of prior expectations, which pressures valuation multiples.

- Comments about sector-wide valuation pressure and a muted sentiment backdrop suggest that, in the view of Bearish analysts, EVgo could continue to face headwinds if execution does not clearly outpace peers.

What's in the News

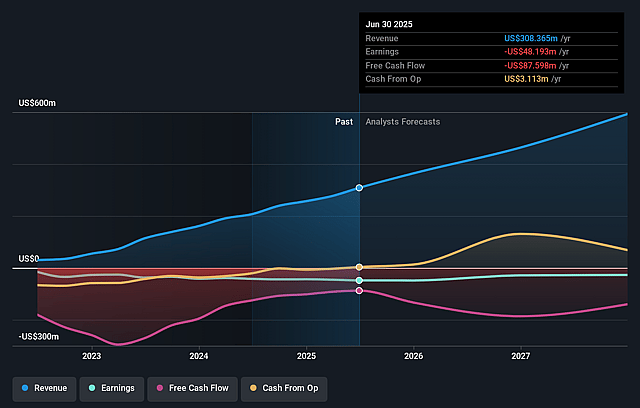

- EVgo issued second quarter 2026 guidance, calling for total revenue of US$75 million to US$85 million. (Company guidance)

- The company reaffirmed full year 2026 total revenue guidance in a range of US$410 million to US$470 million. (Company guidance)

- Earlier guidance for full year 2026 also outlined the same total revenue range of US$410 million to US$470 million, indicating the company is presenting a consistent outlook to investors. (Company guidance)

Valuation Changes

- Fair Value: Held steady at $3.0 per share, indicating no change in the central valuation estimate used in this framework.

- Discount Rate: Edged lower from 9.59% to 9.45%, a small reduction in the rate used to discount future cash flows.

- Revenue Growth: Moderated slightly from 21.52% to 20.68%, pointing to a more restrained forward revenue growth assumption.

- Net Profit Margin: Ticked up marginally from 4.71% to 4.72%, reflecting a very small adjustment in expected profitability.

- Future P/E: Moved down from 19.48x to 18.47x, implying a lower earnings multiple applied to future earnings estimates.

Key Takeaways

- Revenue growth is threatened by slower EV adoption, shifting government policies, and intense competition from larger players and emerging technologies.

- Persistent low utilization rates and reliance on subsidies may drive cash burn, increasing risk of capital raises and margin pressure.

- Accelerating EV adoption, capital efficiency gains, rapid network expansion, technological upgrades, and high-margin ancillary services are set to boost EVgo's growth and profitability.

Catalysts

About EVgo- Owns and operates a direct current fast charging network for electric vehicles in the United States.

- The company's aggressive expansion is fundamentally dependent on projections that electric vehicle growth will vastly outpace charging infrastructure deployment; if EV adoption disappoints due to persistent consumer resistance, competing technologies, or flattening government mandates, EVgo's addressable market could stagnate or shrink, causing revenues by 2029 to fall well short of the $1.2–$1.5 billion target.

- EVgo's long-term financial success relies heavily on an ongoing stream of public and private incentives and low-cost project financing, but with heightened macroeconomic risk and the possibility of government policy shifts or cuts to subsidies, the company could face sharply increased CapEx and borrowing costs, delaying expansion plans and squeezing margins in out-years.

- Despite management's focus on operational leverage, persistently low stall utilization rates combined with multi-year net losses create a substantial risk of cash burn, pressuring the company to raise additional capital in the future and threatening both net margins and shareholder returns through dilution.

- The accelerating pace of network buildout and planned fivefold increase in annual stall deployment could exacerbate industry-wide risks of oversupply, price competition, and technological obsolescence as new charging solutions and battery technologies reduce reliance on public chargers, leading to lower-than-forecast throughput and flattening long-term earnings.

- EVgo's recurring revenue and customer growth are vulnerable as competition intensifies from both large, well-capitalized players (including Tesla and energy majors) and public-private initiatives, risking eroding market share, compressing gross margins, and undermining the projected 32–38 percent adjusted EBITDA margin by decade's end.

EVgo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on EVgo compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming EVgo's revenue will grow by 20.7% annually over the next 3 years.

- The bearish analysts are not forecasting that EVgo will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate EVgo's profit margin will increase from -11.1% to the average US Specialty Retail industry of 4.7% in 3 years.

- If EVgo's profit margin were to converge on the industry average, you could expect earnings to reach $34.7 million (and earnings per share of $0.21) by about May 2029, up from -$46.4 million today.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.6x on those 2029 earnings, up from -5.8x today. This future PE is lower than the current PE for the US Specialty Retail industry at 19.2x.

- The bearish analysts expect the number of shares outstanding to grow by 5.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.45%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The accelerating growth in electric vehicle adoption and a projected quadrupling of EVs in operation by 2030 is expected to significantly increase demand for DC fast charging, expanding EVgo's addressable market and driving revenue and throughput per stall.

- Substantial improvements in capital efficiency, such as a 28% reduction in net CapEx per stall for 2025 and increasingly high capital offsets from state grants and utility incentives, position EVgo for higher project returns and improved net margins over time.

- Robust access to non-dilutive, low-cost capital from both public (DOE) and private (commercial banks) sources allows EVgo to scale aggressively, with forecasts showing a network expansion to approximately 14,000 stalls by 2029, enabling greater operational leverage and EBITDA growth.

- Strategic technological advancements, including next-generation charging architecture, rapid deployment of 350-kilowatt chargers, and integration of NACS cables to attract Tesla drivers, are likely to enhance customer experience, boost network utilization, and support both top-line and bottom-line financials.

- High-margin ancillary revenue streams, such as dedicated hubs for autonomous vehicles, as well as increasing adoption of ridesharing and subscription plans, are expected to provide additional recurring revenues and further strengthen gross margin and EBITDA as these segments scale within the business.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for EVgo is $3.0, which represents up to two standard deviations below the consensus price target of $4.25. This valuation is based on what can be assumed as the expectations of EVgo's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $7.0, and the most bearish reporting a price target of just $3.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $735.2 million, earnings will come to $34.7 million, and it would be trading on a PE ratio of 18.6x, assuming you use a discount rate of 9.5%.

- Given the current share price of $1.9, the analyst price target of $3.0 is 36.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on EVgo?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.