Last Update 19 Mar 26

Fair value Increased 5.92%CDE: Higher Precious Metal Prices And New Gold Deal Will Support Upside

Narrative Update

The updated analyst price target for Coeur Mining has shifted from $27.14 to $28.75. Analysts cite recent Q4 performance, higher gold and silver prices, and expectations for the combined production profile after the proposed New Gold acquisition as key drivers behind the change.

Analyst Commentary

Recent research shows a split in views on Coeur Mining, with some bullish analysts highlighting growth potential around the proposed New Gold acquisition and others focusing on more limited upside after the latest Q4 results.

Bullish Takeaways

- Bullish analysts point to 2025 as a "very successful year" and a key inflection point, citing solid performances across the five operating mines as support for higher valuation targets such as the US$40 price level.

- The proposed all share acquisition of New Gold is a central part of the constructive view, with the combined entity expected to have more than 1.2m annual gold equivalent production and over 20m ounces of silver output, which some see as a meaningful step up in scale.

- Some bullish analysts describe Coeur as an emerging all North American senior precious metals producer and one of the top two silver producers in their coverage, which they argue strengthens the case for premium pricing relative to smaller peers.

- Higher gold and silver prices since prior updates are being used by optimistic voices to justify higher price targets, as stronger commodity pricing can support cash flow and funding of growth projects if sustained.

Bearish Takeaways

- Bearish analysts describe Q4 and full year 2025 results as mixed versus their estimates, which they see as a constraint on re rating potential until there is more consistent delivery against expectations.

- One cautious view is anchored in limited upside to a US$26 price target, which leads to a Hold stance and signals concern that much of the near term execution and growth story could already be reflected in the stock.

- Some commentary highlights that even though recent quarters were characterized as strong operationally, the mixed nature of the Q4 report creates uncertainty around how reliably the business can translate production into shareholder value.

- Cautious analysts also flag that, with targets already lifted to around US$29 by some, any slip in execution on integration of the proposed New Gold deal or future guidance could put pressure on current valuation expectations.

What’s in the News

- Share repurchase activity continued between October 1, 2025 and December 31, 2025, with Coeur buying back 145,929 shares for US$2.29 million, completing a total of 814,129 shares repurchased for US$9.62 million under the May 27, 2025 program (Key Developments).

- Fourth quarter 2025 production results showed gold output of 112,429 ounces and silver output of 4.7 million ounces, compared with 87,149 ounces of gold and 3.2 million ounces of silver in the same quarter a year earlier (Key Developments).

- For full year 2025, reported production was 419,046 ounces of gold and 17.9 million ounces of silver, compared with 341,582 ounces of gold and 11.4 million ounces of silver a year earlier (Key Developments).

- Coeur issued 2026 production guidance, expecting total gold production of 390,000 to 460,000 ounces and total silver production of 18.2 million to 21.3 million ounces (Key Developments).

- At a special meeting on January 27, 2026, stockholders approved an increase in authorized common shares from 900,000,000 to 1,300,000,000 and backed the issuance of new Coeur shares to New Gold shareholders in connection with the planned arrangement (Key Developments).

Valuation Changes

- Fair Value: Updated analyst fair value has risen from $27.14 to $28.75, representing a modest uplift in the valuation anchor used in this framework.

- Discount Rate: The discount rate has eased slightly from 8.25% to 8.22%, representing a marginal change in the implied required return.

- Revenue Growth: Assumed long term revenue growth has moved from 36.79% to 43.36%, reflecting a higher growth input in the model.

- Net Profit Margin: Assumed net profit margin has shifted from 42.11% to 40.65%, indicating a slightly lower profitability assumption on future earnings.

- Future P/E: The future P/E multiple has edged down from 10.01x to 9.54x, implying a slightly lower earnings multiple being applied to projected results.

Key Takeaways

- Rising industrial and investor demand for silver and gold, along with operational improvements, position the company for strong revenue growth and margin expansion.

- Exploration and asset integration efforts are set to extend mine life and underpin stable long-term production.

- Greater regulatory, operational, and financial risks may constrain growth, pressure margins, and jeopardize long-term profitability and cash flow stability.

Catalysts

About Coeur Mining- Operates as a gold and silver producer in the United States, Canada, and Mexico.

- The company is set to benefit from anticipated sustained demand growth for silver, underpinning future topline revenue expansion, as global electrification and clean energy adoption drive higher usage of silver in solar panels, batteries, and EVs.

- Persistent inflationary pressures and ongoing geopolitical uncertainty continue to bolster investor demand for gold and silver as safe-haven assets, which could lead to higher realized prices and expanded net margins for Coeur.

- The successful ramp-up and integration of the Rochester expansion and Las Chispas asset are driving significant increases in silver and gold production, positioning Coeur for robust revenue and earnings growth in the near to medium term.

- Strengthened operational efficiencies-reflected in declining cost applicable to sales per ounce and process improvements at key mines-are improving operating leverage and could further support margin expansion and cash generation.

- Aggressive brownfield exploration and land package expansion at existing sites are likely to extend mine life and expand reserves, supporting sustained long-term production and reducing future earnings volatility.

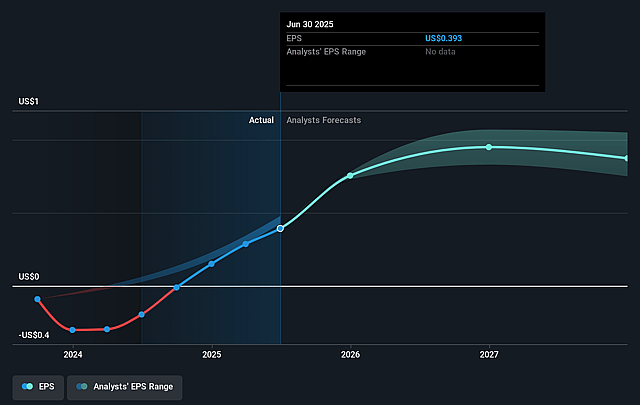

Coeur Mining Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Coeur Mining's revenue will grow by 12.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.1% today to 32.3% in 3 years time.

- Analysts expect earnings to reach $676.1 million (and earnings per share of $0.69) by about September 2028, up from $190.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $1.1 billion in earnings, and the most bearish expecting $485 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.8x on those 2028 earnings, down from 47.1x today. This future PE is lower than the current PE for the US Metals and Mining industry at 22.7x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.37%, as per the Simply Wall St company report.

Coeur Mining Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Expectations for higher regulatory and permitting hurdles, especially highlighted by the multi-year Silvertip development process and emphasis on not cutting corners, may extend lead times for new asset development and expansion, potentially delaying growth projects and revenue realization.

- The company's reliance on existing reserves and need for ongoing infill and expansion drilling to maintain or extend mine life, especially at Las Chispas and other key assets, presents a risk of production declines should exploration fail to replace depletion, which could negatively impact long-term revenue and earnings stability.

- Exposure to currency fluctuations (e.g., significant impact of the strong Mexican peso on costs and taxation) introduces cost volatility and could erode net margins if adverse foreign exchange moves persist.

- Coeur's high capital intensity, as seen in substantial investments at Rochester and Las Chispas as well as legacy acquisition-related amortization and deferred tax liabilities, may pressure cash flows and lead to higher non-cash expenses, reducing reported net income over time.

- Regional and jurisdictional risks, including potential resource nationalism, changing tax regimes, and environmental permitting delays in the U.S., Mexico, and Canada, could increase operating costs, cause project delays, or disrupt production, all of which would impact long-term profitability and cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.083 for Coeur Mining based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.5, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.1 billion, earnings will come to $676.1 million, and it would be trading on a PE ratio of 18.8x, assuming you use a discount rate of 7.4%.

- Given the current share price of $13.97, the analyst price target of $13.08 is 6.8% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Coeur Mining?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives