Catalysts

About Coeur Mining

Coeur Mining operates a portfolio of gold and silver mines in North America, focusing on multi asset production and free cash flow generation.

What are the underlying business or industry changes driving this perspective?

- Reliance on currently elevated gold and silver prices to sustain record free cash flow means any normalization in metals prices would quickly compress EBITDA and reduce the projected more than $550 million in annual free cash flow, which could pressure earnings and valuation multiples.

- Rochester's continued need for modifications, downtime and conveyor fixes to reach its targeted more than 30 million ton annual crushing rate raises the risk that ramp up issues extend into 2026. This could delay the planned 7 to 8 million ounces of silver and 70,000 ounces of gold per year and weigh on revenue growth.

- Greater use of marginal and lower grade ore at operations such as Palmarejo to capitalize on high prices could permanently dilute average reserve quality. It could also lift unit costs once prices moderate and erode net margins over the medium term.

- Silvertip's long dated, capital intensive development path in a tightening regulatory and permitting environment in Canada could lead to cost overruns, schedule slippage and subpar returns on invested capital. This could depress future earnings rather than enhance them.

- Transitioning from a net operating loss position to paying U.S. federal and state income taxes as current high profitability consumes tax assets will structurally raise the effective tax rate. This would cut into net income even if operating margins remain stable.

Assumptions

This narrative explores a more pessimistic perspective on Coeur Mining compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Coeur Mining's revenue will grow by 18.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 24.0% today to 36.1% in 3 years time.

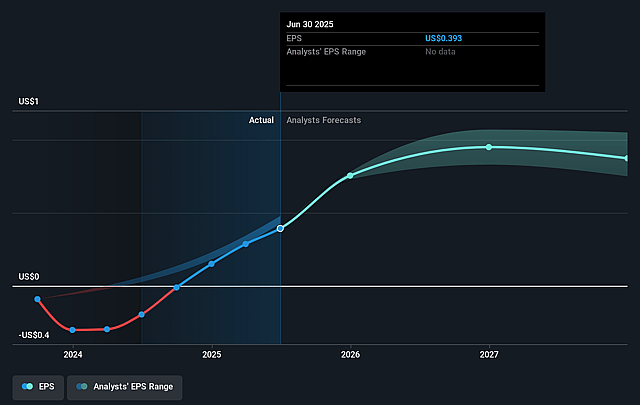

- The bearish analysts expect earnings to reach $1.0 billion (and earnings per share of $1.31) by about December 2028, up from $408.8 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.9 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 13.0x on those 2028 earnings, down from 29.4x today. This future PE is lower than the current PE for the US Metals and Mining industry at 26.4x.

- The bearish analysts expect the number of shares outstanding to grow by 0.57% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.17%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Sustained high gold and silver prices combined with strong production growth across Las Chispas, Palmarejo, Rochester, Kensington and Wharf could support structurally higher metal sales and keep revenue on an upward trajectory rather than declining.

- The company’s rapid transition toward a net cash balance sheet, with net debt already near zero, may lead to lower interest expense and greater financial flexibility, which could help stabilize or expand net margins even if volatility emerges elsewhere.

- Ongoing cost discipline, easing inflation pressures and lower unit cost guidance at several mines suggest that operating costs may remain contained, which would protect or enhance EBITDA and net margins despite any moderation in metal prices.

- Successful integration of Las Chispas and the potential for future growth from projects like Silvertip and continued exploration at Palmarejo could extend mine lives and add new low cost ounces, supporting long term earnings growth instead of contraction.

- Share repurchases funded by strong free cash flow and a record free cash flow run rate could reduce the share count over time, boosting earnings per share and potentially supporting a higher valuation multiple than implied by a bearish outlook.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Coeur Mining is $16.0, which represents up to two standard deviations below the consensus price target of $21.29. This valuation is based on what can be assumed as the expectations of Coeur Mining's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2028, revenues will be $2.8 billion, earnings will come to $1.0 billion, and it would be trading on a PE ratio of 13.0x, assuming you use a discount rate of 8.2%.

- Given the current share price of $18.72, the analyst price target of $16.0 is 17.0% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Coeur Mining?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.