Last Update04 Oct 25Fair value Decreased 1.62%

Analysts have slightly lowered their fair value estimate for Upstart Holdings from approximately $80.85 to $79.54. They cite concerns about rising delinquencies in recent loan vintages and possible risks to future transaction volume.

Analyst Commentary

Recent analyst notes on Upstart Holdings present a mixture of optimism and caution, reflecting both the company’s strengths and the challenges it faces in the current environment.

Bullish Takeaways

- Bullish analysts have lifted price targets for Upstart, citing positive quarterly results that indicate resilience in the company’s execution and underlying business model.

- Despite volatile market reactions, continued growth in transaction volume and a strong earnings beat are viewed as signs of Upstart’s ability to navigate near-term uncertainty.

- The company’s marketplace platform is regarded as a leader in the sector, with potential for share gains as lending activity stabilizes or recovers.

- Raising of price targets reflects confidence that current challenges may be temporary and that valuation upside remains achievable if execution stays on track.

Bearish Takeaways

- Bearish analysts remain cautious due to a concerning rise in loan delinquencies in recent vintages, which they see as a potential risk to sustained transaction growth and loan performance.

- Some note that consensus expectations for transaction volume may be overly optimistic, particularly if delinquency trends persist or worsen.

- There are concerns over take rate compression as Upstart shifts its focus upmarket, with risks that this could weigh on future profitability and growth rates.

- Certain Wall Street firms have tempered their outlooks and suggest near-term downside in the stock if these business risks are not addressed effectively.

What's in the News

- Cornerstone Community Financial Credit Union has partnered with Upstart to offer more inclusive personal loans via the Upstart Referral Network, with lending set to begin in April 2025 (Key Developments).

- ABNB Federal Credit Union started partnering with Upstart in May 2025, expanding access to personal loans through a streamlined and branded online experience (Key Developments).

- Cabrillo Credit Union joined the Upstart Referral Network in April 2025, allowing qualified applicants to receive tailored offers and complete loan processes online (Key Developments).

- Upstart completed its previously announced buyback program, repurchasing a total of 5,884,000 shares. This represents 7.04% of shares for $177.95 million (Key Developments).

- The company provided earnings guidance for Q3 and the full year 2025, forecasting $280 million in quarterly revenue, a GAAP net loss of $9 million for the quarter, and $1.055 billion in annual revenue with $35 million in GAAP net income (Key Developments).

Valuation Changes

- Fair Value Estimate has decreased slightly from $80.85 to $79.54, reflecting a modest reduction in assessed company value.

- Discount Rate has risen from 8.32% to 8.50%. This indicates a higher return requirement and slightly increased perceived risk.

- Revenue Growth Projection remains unchanged at approximately 27.21%, suggesting stable growth expectations.

- Net Profit Margin Projection is effectively unchanged and holds steady at around 18.52%.

- Future P/E Ratio has fallen slightly from 34.12x to 33.74x. This reflects a minor adjustment in valuation multiples by analysts.

Key Takeaways

- Improvements in underwriting, automation, and personalization enhance loan approval rates, lower costs, and reduce default risks, positively impacting revenue and net margins.

- Strategic HELOC growth, backed by strong banking relationships, alongside expanded borrower base, sets stage for future revenue growth and earnings support.

- High default rates and macroeconomic volatility threaten revenue stability, while maintaining model accuracy and managing profitability amid these conditions are critical challenges.

Catalysts

About Upstart Holdings- Operates a cloud-based artificial intelligence (AI) lending platform in the United States.

- The implementation of Model 19, featuring the Payment Transition Model (PTM), has improved underwriting accuracy, which is likely to enhance loan approval rates and reduce default risks, positively impacting revenue and net margins.

- Upstart's HELOC product growth, driven by conversion improvements, cross-selling, and state expansion, positions it well for future revenue growth and margins with the potential to leverage its strong relationships with banks and credit unions for cost-effective funding.

- Improvements in small dollar relief loans, such as reduced origination costs, have expanded Upstart's borrower base and are expected to contribute to revenue growth, while the integration of small dollar repayment data will enhance the accuracy of underwriting models.

- Increased automation and personalization in servicing operations have reduced costs and improved borrower outcomes, which will likely improve net margins through operational efficiencies and lower default rates.

- Enhanced lending partner confidence, due to strong platform performance and capital market engagements, strengthens funding capabilities and sets the stage for increased origination volume, supporting earnings growth in the medium term.

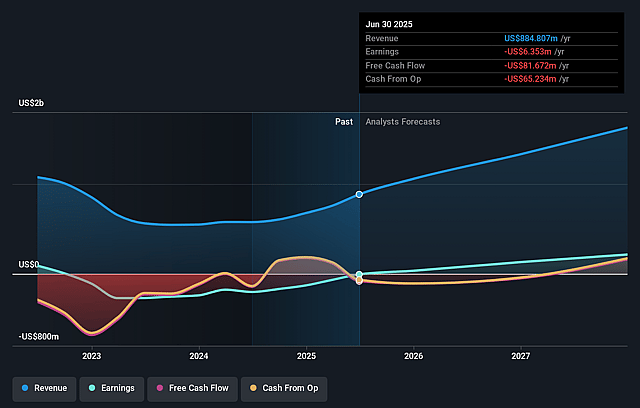

Upstart Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Upstart Holdings's revenue will grow by 27.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.7% today to 18.5% in 3 years time.

- Analysts expect earnings to reach $337.2 million (and earnings per share of $1.54) by about September 2028, up from $-6.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 34.1x on those 2028 earnings, up from -976.3x today. This future PE is greater than the current PE for the US Consumer Finance industry at 10.6x.

- Analysts expect the number of shares outstanding to grow by 5.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.32%, as per the Simply Wall St company report.

Upstart Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company has faced periods of underperformance due to high default rates during macroeconomic volatility, potentially impacting future revenue and profit stability.

- There are concerns about maintaining consistent model accuracy, which is crucial for managing risk and ensuring profitability, due to potential gaps between predicted and actual default rates.

- The company's profitability is sensitive to macroeconomic changes, such as interest rate movements and macro indices (e.g., the Upstart Macro Index), which could affect earnings and net margins if conditions worsen.

- Although the company plans to reduce loans on its balance sheet, potential funding constraints could delay these efforts, affecting liquidity and net income.

- Investments in new product categories and marketing could pressure operating margins and net income if not managed properly against growth expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $80.846 for Upstart Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $105.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.8 billion, earnings will come to $337.2 million, and it would be trading on a PE ratio of 34.1x, assuming you use a discount rate of 8.3%.

- Given the current share price of $64.46, the analyst price target of $80.85 is 20.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.