Key Takeaways

- Accelerated digital adoption, loyalty program success, and modernized store expansion are driving stronger revenue growth and operating efficiency than analysts anticipate.

- Strategic menu innovation and localization, combined with favorable demographic trends and a solid balance sheet, position the company for sustained market share and margin gains.

- Heightened health awareness, economic volatility, competition, rising costs, and ESG demands pose persistent challenges to revenue, margins, and profitability.

Catalysts

About Arcos Dorados Holdings- Operates as a franchisee of McDonald’s restaurants.

- Analyst consensus acknowledges the positive impact of the Four D's strategy but likely underestimates the speed and scale at which Arcos Dorados is leveraging digital and loyalty synergies; with 60% digital sales penetration already achieved and loyalty member sales surpassing 23% in key markets, a sharp acceleration in digital-driven frequency and ticket size could materially boost both revenue growth and operating leverage faster than expected.

- While analysts broadly expect EOTF expansion to drive operational improvements, they may be understating the compounding effects of near-complete EOTF penetration and rapid new openings; as 90% of the portfolio modernizes and site selection is increasingly optimized with AI, Arcos Dorados will have a uniquely defensible and operationally efficient footprint to maximize same-store revenue and EBITDA margins.

- The expanding middle class and rising urbanization across Latin America directly benefit Arcos Dorados, positioning the company for outsized same-store sales growth and market share gains as consumer purchasing power and urban traffic flows increase, ultimately supporting multi-year revenue and earnings expansion well above current market expectations.

- Strategic menu innovation and aggressive localization are just beginning to unlock higher-margin premium offerings and incremental revenue streams; this adaptability-evidenced by record dessert sales, targeted licensed products, and localized campaigns-is likely to sustainably lift net margins and average check over time.

- With industry consolidation expected to accelerate and Arcos Dorados holding a strong balance sheet with investment grade ratings and low net leverage, the company is poised to capitalize on M&A opportunities or further exclusive market rights as weaker competitors retrench, boosting future top-line and scale-driven margin expansion.

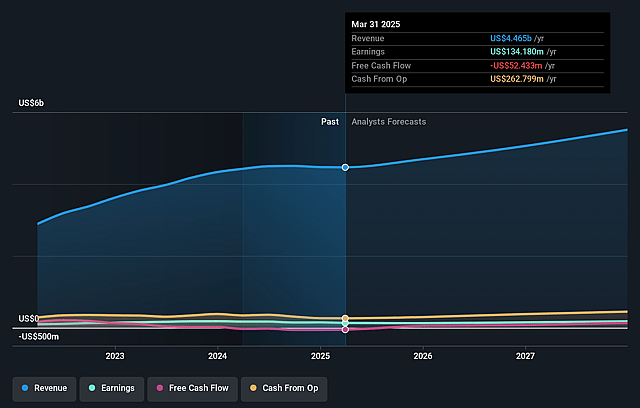

Arcos Dorados Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Arcos Dorados Holdings compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Arcos Dorados Holdings's revenue will grow by 12.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 2.9% today to 3.5% in 3 years time.

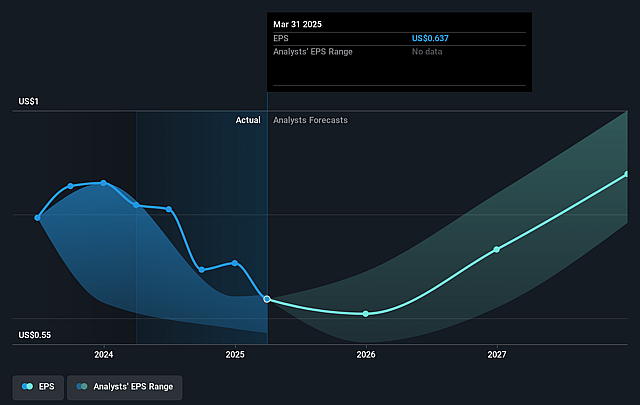

- The bullish analysts expect earnings to reach $226.0 million (and earnings per share of $1.08) by about September 2028, up from $130.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 19.5x on those 2028 earnings, up from 11.2x today. This future PE is lower than the current PE for the US Hospitality industry at 23.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.12%, as per the Simply Wall St company report.

Arcos Dorados Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising health consciousness and increasing regulatory scrutiny of fast food and processed meats may cause a long-term decline in customer volumes, which would put sustained pressure on revenue generation.

- Currency volatility and macroeconomic instability in core Latin American markets, such as Brazil and Argentina, create unpredictable earnings outcomes, leading to swings in reported profits and undermining long-term earnings growth.

- Intensifying competition from regional quick-service restaurants and new entrants, especially in segments like desserts, forces Arcos Dorados to engage in aggressive pricing and promotional activity, potentially eroding operating margins and market share.

- Escalating food input costs, particularly beef, and ongoing wage inflation in Latin America threaten to increase operating expenses, thereby compressing net profit margins over the long term.

- Demands for sustainable business practices and ESG compliance are likely to require persistent investments in supply chain transparency, packaging, and energy management, elevating operating costs and impacting bottom-line profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Arcos Dorados Holdings is $13.42, which represents two standard deviations above the consensus price target of $10.4. This valuation is based on what can be assumed as the expectations of Arcos Dorados Holdings's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $14.0, and the most bearish reporting a price target of just $8.5.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $6.5 billion, earnings will come to $226.0 million, and it would be trading on a PE ratio of 19.5x, assuming you use a discount rate of 16.1%.

- Given the current share price of $6.9, the bullish analyst price target of $13.42 is 48.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.