Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:GTM

Why We're Not Concerned Yet About ZoomInfo Technologies Inc.'s (NASDAQ:ZI) 26% Share Price Plunge

The ZoomInfo Technologies Inc. (NASDAQ:ZI) share price has fared very poorly over the last month, falling by a substantial 26%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 56% loss during that time.

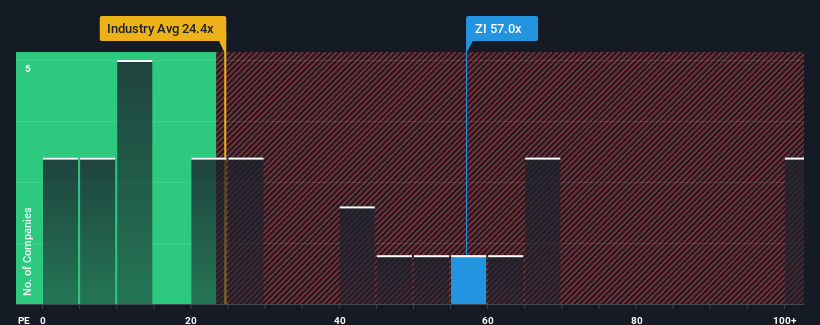

Even after such a large drop in price, ZoomInfo Technologies may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 57x, since almost half of all companies in the United States have P/E ratios under 17x and even P/E's lower than 9x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, ZoomInfo Technologies has been very sluggish. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

View our latest analysis for ZoomInfo Technologies

Is There Enough Growth For ZoomInfo Technologies?

ZoomInfo Technologies' P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered a frustrating 21% decrease to the company's bottom line. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 45% each year as estimated by the analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 9.9% per annum, which is noticeably less attractive.

With this information, we can see why ZoomInfo Technologies is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On ZoomInfo Technologies' P/E

Even after such a strong price drop, ZoomInfo Technologies' P/E still exceeds the rest of the market significantly. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that ZoomInfo Technologies maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for ZoomInfo Technologies with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on ZoomInfo Technologies, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if ZoomInfo Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:GTM

ZoomInfo Technologies

Provides go-to-market intelligence and engagement platform for sales, marketing, operations, and recruiting professionals in the United States and internationally.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.8% undervalued

65 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22045.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3533.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Gilead Sciences ·

Attractive medium-term compounder with catalyst-rich profile, but with short-term volatility tied to investment phase

Fair Value:US$128.381.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k20.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$435.6930.6% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.4% undervalued

112 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.6% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6117.9% undervalued

1187 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative