Advertisement

- United States

- /

- Electrical

- /

- NasdaqGM:ARRY

Need To Know: Analysts Just Made A Substantial Cut To Their Array Technologies, Inc. (NASDAQ:ARRY) Estimates

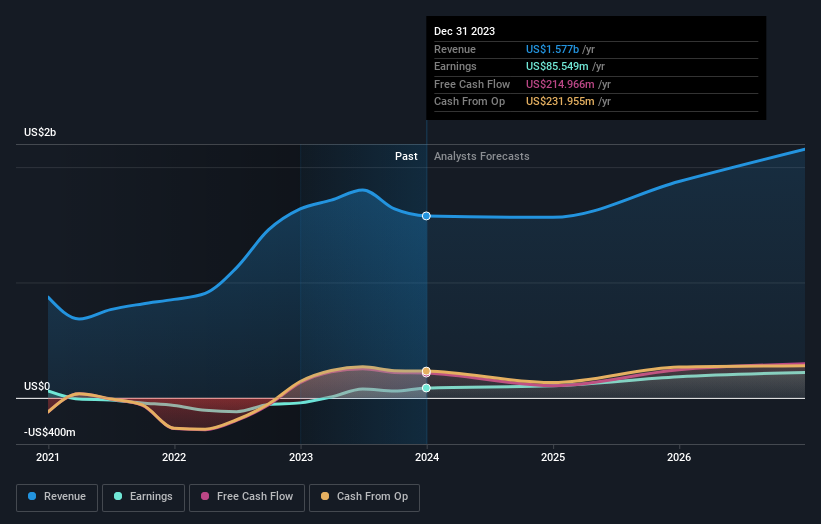

The latest analyst coverage could presage a bad day for Array Technologies, Inc. (NASDAQ:ARRY), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

Following this downgrade, Array Technologies' 23 analysts are forecasting 2024 revenues to be US$1.6b, approximately in line with the last 12 months. Per-share earnings are expected to ascend 15% to US$0.65. Previously, the analysts had been modelling revenues of US$1.9b and earnings per share (EPS) of US$0.87 in 2024. Indeed, we can see that the analysts are a lot more bearish about Array Technologies' prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Array Technologies

The consensus price target fell 13% to US$21.28, with the weaker earnings outlook clearly leading analyst valuation estimates.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that sales are expected to reverse, with a forecast 0.8% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 25% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 7.7% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Array Technologies is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that Array Technologies' revenues are expected to grow slower than the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Array Technologies.

A high debt burden combined with a downgrade of this magnitude always gives us some reason for concern, especially if these forecasts are just the first sign of a business downturn. See why we're concerned about Array Technologies' balance sheet by visiting our risks dashboard for free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:ARRY

Array Technologies

Manufactures and sells solar tracking technology products in the United States, Spain, Brazil, Australia, and internationally.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5620.1% overvalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TI

TibiT on Costco Wholesale ·

Investment Thesis: Costco Wholesale (COST)

Fair Value:US$726.2932.7% overvalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.7% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

YI

yiannisz on Intuit ·

Intuit Stock: When Financial Software Becomes the Operating System for Small Business

Fair Value:US$769.8929.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on UnitedHealth Group ·

UnitedHealth Stock: Why Scale, Data, and Integration Still Matter in U.S. Healthcare

Fair Value:US$308.357.4% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VP

VPC on Ramayana Lestari Sentosa ·

Unique One, Retail Sector, but Short Time Investmentnya Almost 2,5 kali Persediaan

Fair Value:Rp279.8866.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8230.6% undervalued

78 followersusers have followed this narrative

6 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.4% undervalued

1030 followersusers have followed this narrative

6 commentsusers have commented on this narrative

30 likesusers have liked this narrative

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3324.7% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Trending Discussion

RO

RockeTeller on West Red Lake Gold Mines ·

I'm exiting the positions at great return! WRLG got great competent management. But, 100k oz gold too small in today environment. They might looking for M/A opportunity in the future, or they might get take over by Aris Mining, I don't know. But, Frank Giustra stated he's believed in multi-assets, so that's my speculation. Anyhow, I want to be aggressive in today's gold price. I'm buying Lahontan Gold LG with this as exchange. Higher upside, more leverage. WRLG CEO is BOD's of LG, that's something. This will be my last update on WRLG, good luck!

1

|0