- South Africa

- /

- Chemicals

- /

- JSE:BCF

Shareholders May Not Be So Generous With Bowler Metcalf Limited's (JSE:BCF) CEO Compensation And Here's Why

Key Insights

- Bowler Metcalf's Annual General Meeting to take place on 7th of November

- Salary of R3.82m is part of CEO Friedel Sass's total remuneration

- The total compensation is 72% higher than the average for the industry

- Bowler Metcalf's EPS declined by 3.5% over the past three years while total shareholder return over the past three years was 57%

Bowler Metcalf Limited (JSE:BCF) has exhibited strong share price growth in the past few years. However, its earnings growth has not kept up, suggesting that there may be something amiss. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 7th of November. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

Check out our latest analysis for Bowler Metcalf

Comparing Bowler Metcalf Limited's CEO Compensation With The Industry

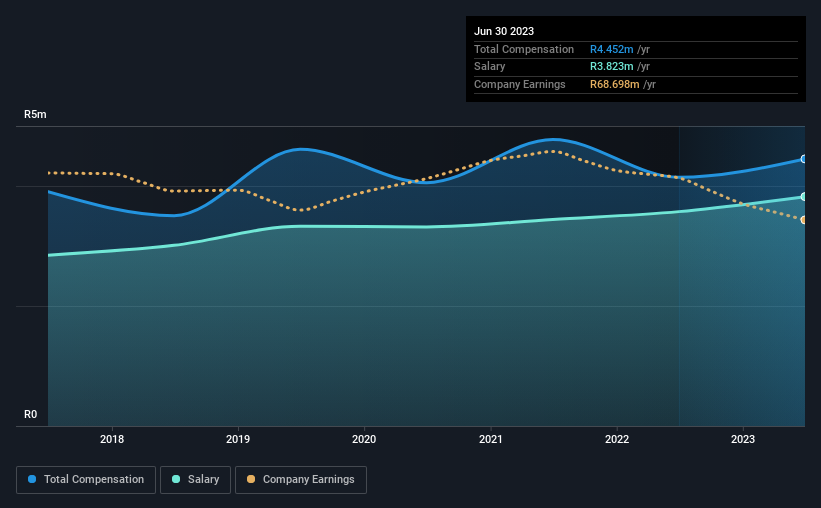

At the time of writing, our data shows that Bowler Metcalf Limited has a market capitalization of R712m, and reported total annual CEO compensation of R4.5m for the year to June 2023. That's just a smallish increase of 7.4% on last year. We note that the salary portion, which stands at R3.82m constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the South Africa Chemicals industry with market capitalizations below R3.7b, reported a median total CEO compensation of R2.6m. Accordingly, our analysis reveals that Bowler Metcalf Limited pays Friedel Sass north of the industry median. What's more, Friedel Sass holds R197m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | R3.8m | R3.6m | 86% |

| Other | R629k | R571k | 14% |

| Total Compensation | R4.5m | R4.1m | 100% |

On an industry level, roughly 49% of total compensation represents salary and 51% is other remuneration. According to our research, Bowler Metcalf has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Bowler Metcalf Limited's Growth

Over the last three years, Bowler Metcalf Limited has shrunk its earnings per share by 3.5% per year. Its revenue is up 6.5% over the last year.

Few shareholders would be pleased to read that EPS have declined. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Bowler Metcalf Limited Been A Good Investment?

We think that the total shareholder return of 57%, over three years, would leave most Bowler Metcalf Limited shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

While the return to shareholders does look promising, it's hard to ignore the lack of earnings growth and this makes us question whether these strong returns will continue. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 2 warning signs for Bowler Metcalf you should be aware of, and 1 of them is a bit concerning.

Important note: Bowler Metcalf is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Bowler Metcalf might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:BCF

Bowler Metcalf

Manufactures and sells rigid plastic packaging in South Africa.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion