- South Africa

- /

- Machinery

- /

- JSE:BEL

We Think Bell Equipment Limited's (JSE:BEL) CEO Compensation Package Needs To Be Put Under A Microscope

The results at Bell Equipment Limited (JSE:BEL) have been quite disappointing recently and CEO Leon Goosen bears some responsibility for this. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 18 June 2021. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. The data we present below explains why we think CEO compensation is not consistent with recent performance.

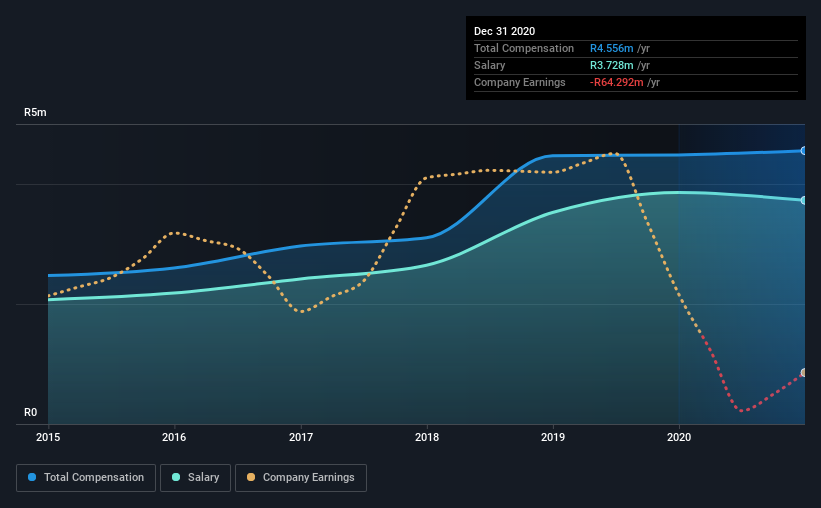

View our latest analysis for Bell Equipment

Comparing Bell Equipment Limited's CEO Compensation With the industry

According to our data, Bell Equipment Limited has a market capitalization of R870m, and paid its CEO total annual compensation worth R4.6m over the year to December 2020. That's mostly flat as compared to the prior year's compensation. We note that the salary portion, which stands at R3.73m constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the industry with market capitalizations below R2.7b, we found that the median total CEO compensation was R2.1m. Accordingly, our analysis reveals that Bell Equipment Limited pays Leon Goosen north of the industry median.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | R3.7m | R3.9m | 82% |

| Other | R828k | R627k | 18% |

| Total Compensation | R4.6m | R4.5m | 100% |

On an industry level, roughly 60% of total compensation represents salary and 40% is other remuneration. Bell Equipment pays out 82% of remuneration in the form of a salary, significantly higher than the industry average. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Bell Equipment Limited's Growth Numbers

Over the last three years, Bell Equipment Limited has shrunk its earnings per share by 78% per year. It saw its revenue drop 14% over the last year.

Overall this is not a very positive result for shareholders. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Bell Equipment Limited Been A Good Investment?

With a three year total loss of 26% for the shareholders, Bell Equipment Limited would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 2 warning signs for Bell Equipment you should be aware of, and 1 of them is significant.

Switching gears from Bell Equipment, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bell Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About JSE:BEL

Bell Equipment

Designs, manufactures, exports, distributes, and supports a range of heavy equipment for the mining and quarrying, construction, forestry, agriculture, and industry sectors in South Africa, Rest of Africa, and Europe.

Flawless balance sheet and fair value.

Market Insights

Community Narratives