- United States

- /

- Other Utilities

- /

- NYSE:WEC

WEC Energy Group (NYSE:WEC) Projects 2025 Earnings Growth and Announces Dividend Increase

Reviewed by Simply Wall St

WEC Energy Group (NYSE:WEC) has recently announced its earnings guidance for 2025, projecting earnings per share between $5.17 and $5.27, with a midpoint of $5.22. The company also plans to increase its quarterly dividend by 6.9% to 89.25 cents per share, effective in the first quarter of 2025. These developments, alongside a $28 billion capital investment plan focusing on renewables and natural gas, underscore WEC's commitment to growth despite facing financial challenges and regulatory hurdles. The company's report discusses its financial performance, growth strategies, and risk management efforts.

Click here and access our complete analysis report to understand the dynamics of WEC Energy Group.

Core Advantages Driving Sustained Success for WEC Energy Group

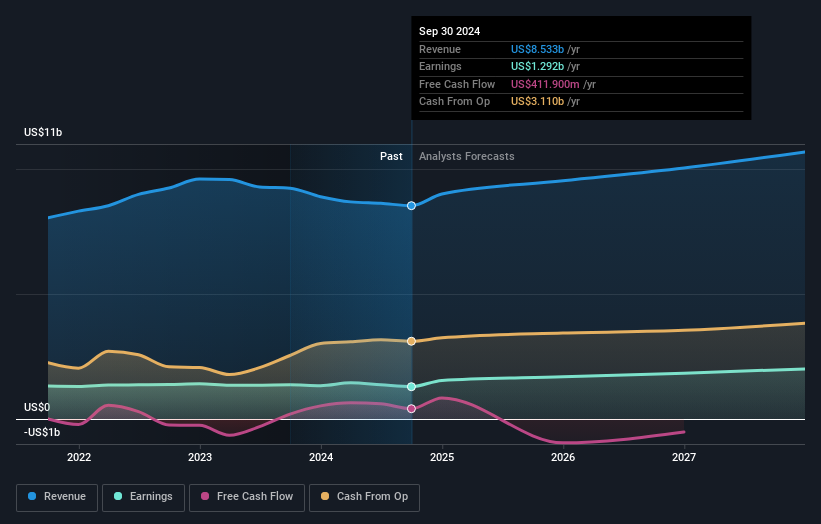

WEC Energy Group's financial performance is highlighted by its third-quarter 2024 adjusted earnings of $0.82 per share, affirming its solid financial health. Scott Lauber, President and CEO, emphasized the company's trajectory towards a strong 2024. The economic environment in Wisconsin, marked by a 2.9% unemployment rate, supports the company's growth strategies and capital investments. This favorable backdrop is complemented by a $28 billion capital plan for 2025-2029, the largest in its history, aimed at enhancing system reliability through investments in renewables and natural gas generation. Furthermore, the company's reliable dividend payments over the past decade and forecasted earnings growth of 11.44% per year bolster its financial stability. The company is currently trading below its estimated fair value, suggesting it may be undervalued, which could be indicative of its strong market positioning.

Challenges Constraining WEC Energy Group's Potential

The company has faced a 5.4% decline in earnings growth over the past year, with a low return on equity of 10.4%. These figures highlight financial challenges, exacerbated by a high net debt to equity ratio of 151.1%. The interest payments, only covered 2.7 times by earnings, reveal financial vulnerabilities. Regulatory changes in Illinois have also impacted earnings, as noted by CFO Xia Lu, who pointed to increased O&M, depreciation, and interest expenses. Additionally, a reduction of $800 million in planned infrastructure investments may indicate strategic challenges. Despite these issues, the company's valuation suggests it may be undervalued, yet it remains expensive relative to industry averages.

Growth Avenues Awaiting WEC Energy Group

Opportunities abound for WEC Energy Group, particularly in renewable energy investments. The company plans to invest $9.1 billion in solar, wind, and battery storage, positioning itself to meet the growing demand for clean energy. Economic development in Wisconsin, especially in the I-94 corridor, promises increased energy sales with an anticipated demand of 1,800 megawatts over the next five years. The acquisition of a 90% interest in Hardin Solar III Energy Park, adding 250 megawatts of renewable energy, aligns with its expansion strategy. These initiatives are poised to enhance market position and drive performance.

Market Volatility Affecting WEC Energy Group's Position

Regulatory challenges in Illinois, including the Safety Modernization Program review, pose ongoing risks. Economic dependency in service areas, as highlighted by Lauber, underscores the potential impact of downturns on energy demand and financial performance. Weather-related risks continue to affect operations, with year-to-date earnings trailing by $0.07 due to adverse conditions. These factors necessitate effective risk management strategies to safeguard against market volatility and maintain growth momentum.

Conclusion

WEC Energy Group's financial health, underscored by its third-quarter 2024 adjusted earnings of $0.82 per share, positions it well for future growth, particularly with its substantial $28 billion capital plan aimed at enhancing system reliability and expanding into renewables. However, the company faces significant challenges, including a recent decline in earnings growth, a high net debt to equity ratio, and regulatory hurdles in Illinois, which could constrain its potential. The company's strategic investments in renewable energy and its current trading status below estimated fair value suggest a strong market positioning that could drive future performance. This implies that while the company is expensive relative to peers based on its Price-To-Earnings Ratio, it holds promising prospects for growth if it can effectively manage its financial vulnerabilities and capitalize on its investment strategies.

Next Steps

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade WEC Energy Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if WEC Energy Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WEC

WEC Energy Group

Through its subsidiaries, provides regulated natural gas and electricity, and renewable and nonregulated renewable energy services in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Community Narratives