Advertisement

- United States

- /

- Renewable Energy

- /

- NYSE:ORA

Ormat Technologies (ORA) Is Down 6.4% After Ormega100 Launch And Cautious Bernstein Initiation Has The Bull Case Changed?

Reviewed by Sasha Jovanovic

- Earlier in June 2026, Ormat Technologies announced the Ormega100, a 100 MW autonomous surface power unit designed to accelerate commercialization of its Enhanced Geothermal System developments and connect subsurface resources with large-scale binary power generation.

- The Ormega100, described as the industry’s largest binary unit tailored for high-temperature EGS environments, could materially influence how quickly geothermal projects scale from pilot phase to full commercial deployment.

- Now we’ll examine how Bernstein’s cautious initiation and Ormat’s Ormega100 launch together reshape the company’s investment narrative around geothermal growth.

Find 45 companies with promising cash flow potential yet trading below their fair value.

Ormat Technologies Investment Narrative Recap

To own Ormat, you need to believe geothermal and storage can compound steadily while the company manages high capital needs and operational complexity. Bernstein’s cautious initiation spotlights exploration and execution risk, while the Ormega100 launch highlights EGS as the key near term catalyst; together, they refocus attention on whether Ormat can translate technical progress into reliable, profitable growth. The biggest immediate risk still sits in execution across capital intensive projects and wellfield performance, rather than this specific announcement.

Among recent updates, the launch of the 100 MW Ormega100 unit is most relevant here because it directly addresses concerns about Ormat’s Enhanced Geothermal System pilots and their path to commercial scale. By linking subsurface EGS development with a large, modular surface unit, Ormat is trying to shorten the time between pilot projects and grid connected power, which could matter for how investors weigh EGS as a future earnings contributor versus ongoing capex and balance sheet pressure.

Yet against this potential, investors should be aware of how Ormat’s high annual exploration drilling spend and elevated net debt could...

Read the full narrative on Ormat Technologies (it's free!)

Ormat Technologies' narrative projects $1.3 billion revenue and $194.6 million earnings by 2029. This requires 4.1% yearly revenue growth and a $67.0 million earnings increase from $127.6 million today.

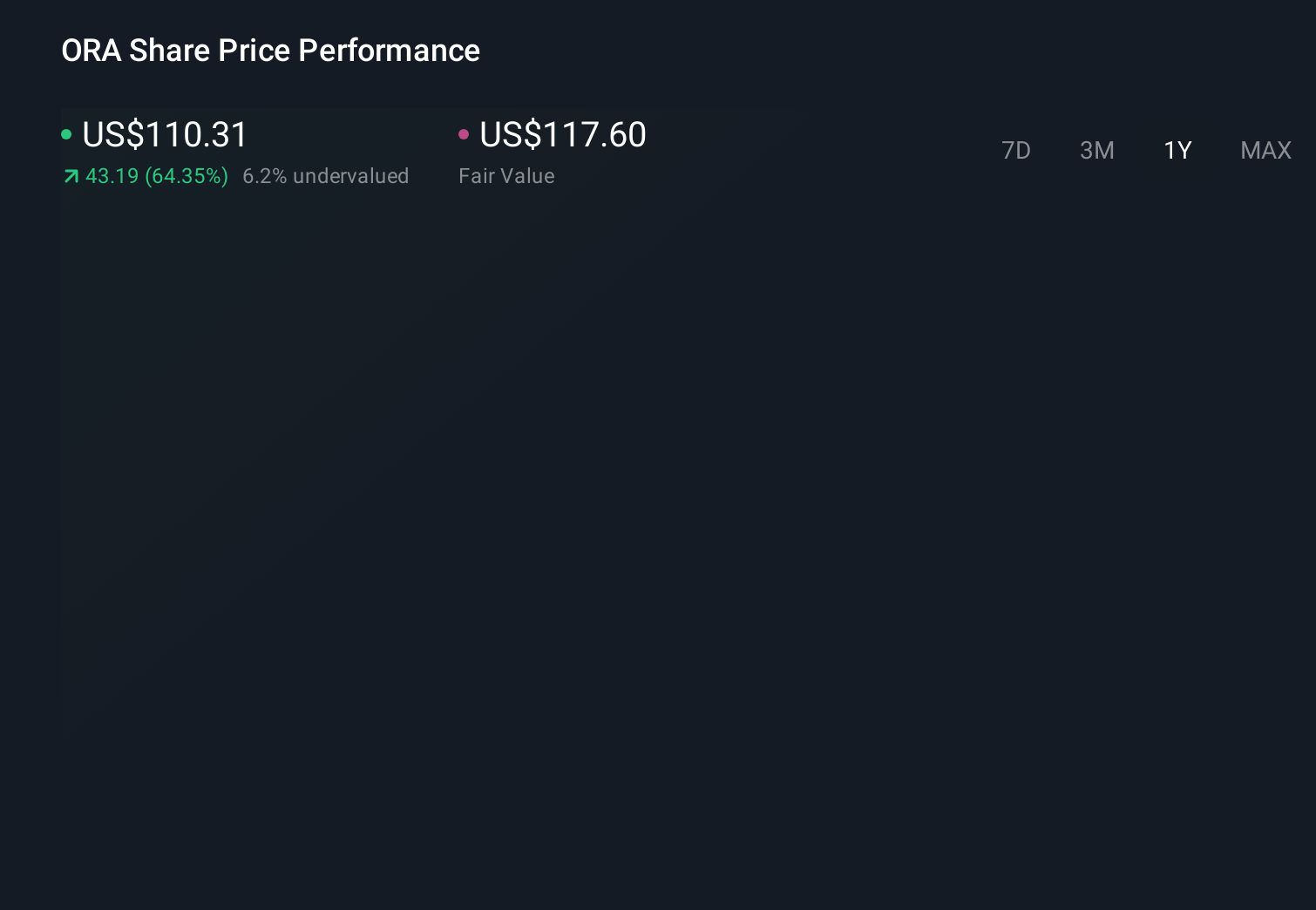

Uncover how Ormat Technologies' forecasts yield a $135.45 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members see Ormat’s fair value between US$118.26 and US$174.88, underlining how far individual views can spread. Before you decide where you stand, consider how capex demands and balance sheet risk could affect Ormat’s ability to turn innovations like Ormega100 into long term financial performance and explore several alternative viewpoints.

Explore 3 other fair value estimates on Ormat Technologies - why the stock might be worth 7% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ormat Technologies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Ormat Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ormat Technologies' overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ORA

Ormat Technologies

Engages in the geothermal and recovered energy power business in the United States, Indonesia, Kenya, Turkey, Chile, Guatemala, Guadeloupe, New Zealand, Honduras, France, Indonesia, the Philippines, and internationally.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.8% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

LY

Lyra on DT Cloud Star Acquisition ·

A SPAC in the Endgame Between Lifeboat and Siren Song

Fair Value:US$6.1584.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Luca Mining ·

Luca Mining, $176M Revenue, Strong FCF, 200K Oz AuEq Vision & Debt-Free by Mid-2026

Fair Value:CA$3.9972.4% undervalued

4 followersusers have followed this narrative

1 commentusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

58 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative