- United States

- /

- Other Utilities

- /

- NYSE:ED

Consolidated Edison (NYSE:ED) Reports Strong Q1 2025 Earnings

Reviewed by Simply Wall St

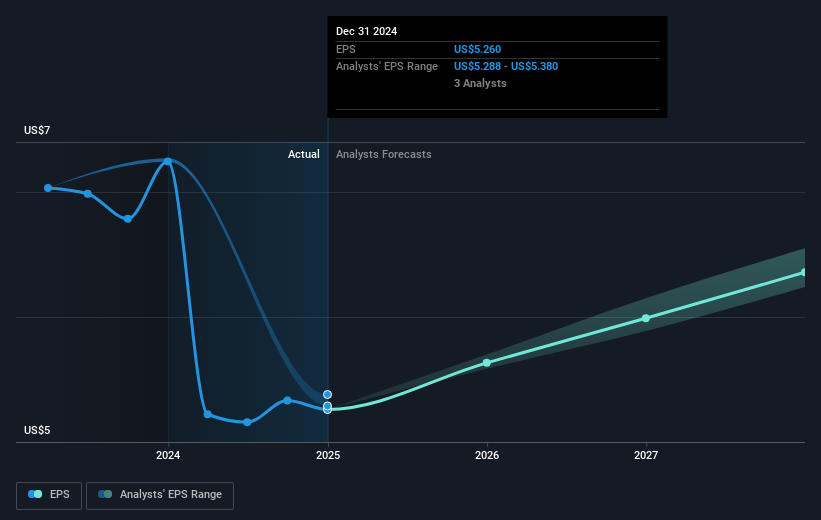

Consolidated Edison (NYSE:ED) reported strong financial results for the first quarter of 2025, with notable increases in sales and earnings compared to the previous year. This positive performance, along with the announcement of a consistent quarterly dividend of 85 cents per share, potentially provided stability and confidence to investors during the period. The company's 3.77% share price increase over the last quarter aligns fairly closely with broader market trends, indicating that its earnings growth, dividend affirmation, and other corporate actions during this time period likely supported its stock price performance amidst a generally upward-trending market environment.

Find companies with promising cash flow potential yet trading below their fair value.

Over the past five years, Consolidated Edison has achieved a total return of 68.41%, which combines share price appreciation with dividends. This long-term performance contrasts with its one-year return, where the company underperformed the US Integrated Utilities industry, which returned 9.7%. Additionally, its return over the past year fell short of the broader US market, which saw an 11.5% increase.

The company's recent earnings growth and dividend declaration could have positive implications for future revenue and earnings forecasts, although analysts expect its annual profit growth rate to fall short of the market average. Despite solid financial results and earnings growth, Consolidated Edison's current share price remains below the consensus analyst price target of US$105.97, indicating room for potential appreciation within the estimated fair value framework. The company's continued commitment to dividend payments and stable financial performance offers some reassurance to investors, but its slower expected growth may temper broader market enthusiasm.

Assess Consolidated Edison's previous results with our detailed historical performance reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ED

Consolidated Edison

Through its subsidiaries, engages in the regulated electric, gas, and steam delivery businesses in the United States.

Average dividend payer and fair value.

Similar Companies

Market Insights

Community Narratives