- United States

- /

- Water Utilities

- /

- NYSE:CWT

Reassessing California Water Service Group (CWT) Valuation After a Choppy Three-Year Share Price Decline

Reviewed by Simply Wall St

California Water Service Group (CWT) has been quietly grinding through a choppy year, with the stock slipping over the past 3 months even as revenue and net income continue to grow at a steady clip.

See our latest analysis for California Water Service Group.

The recent pullback, including a 30 day share price return of minus 3.3 percent and a 90 day share price return of minus 3.6 percent, sits on top of a much tougher three year total shareholder return of minus 23.3 percent. This suggests sentiment has been fading even as fundamentals improve.

If CWT has you reassessing defensive names, this is also a good moment to broaden your watchlist and explore fast growing stocks with high insider ownership.

With revenue and earnings still climbing and the share price lagging both analyst targets and long term history, investors now face a key question: is CWT a quietly undervalued compounder, or is the market already pricing in its future growth?

Most Popular Narrative Narrative: 17.1% Undervalued

With California Water Service Group last closing at $43.96 against a narrative fair value of approximately $53.00, the valuation case leans on long term infrastructure and margin expansion.

Analysts are assuming California Water Service Group's revenue will grow by 3.9% annually over the next 3 years. Analysts assume that profit margins will increase from 13.7% today to 16.9% in 3 years time.

Want to see what turns modest growth into a higher valuation multiple? The narrative quietly upgrades margins and earnings power in a way most investors overlook.

Result: Fair Value of $53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative faces pressure if California’s rate case is delayed, or PFAS treatment costs escalate faster than regulators allow timely recovery.

Find out about the key risks to this California Water Service Group narrative.

Another Angle on Value

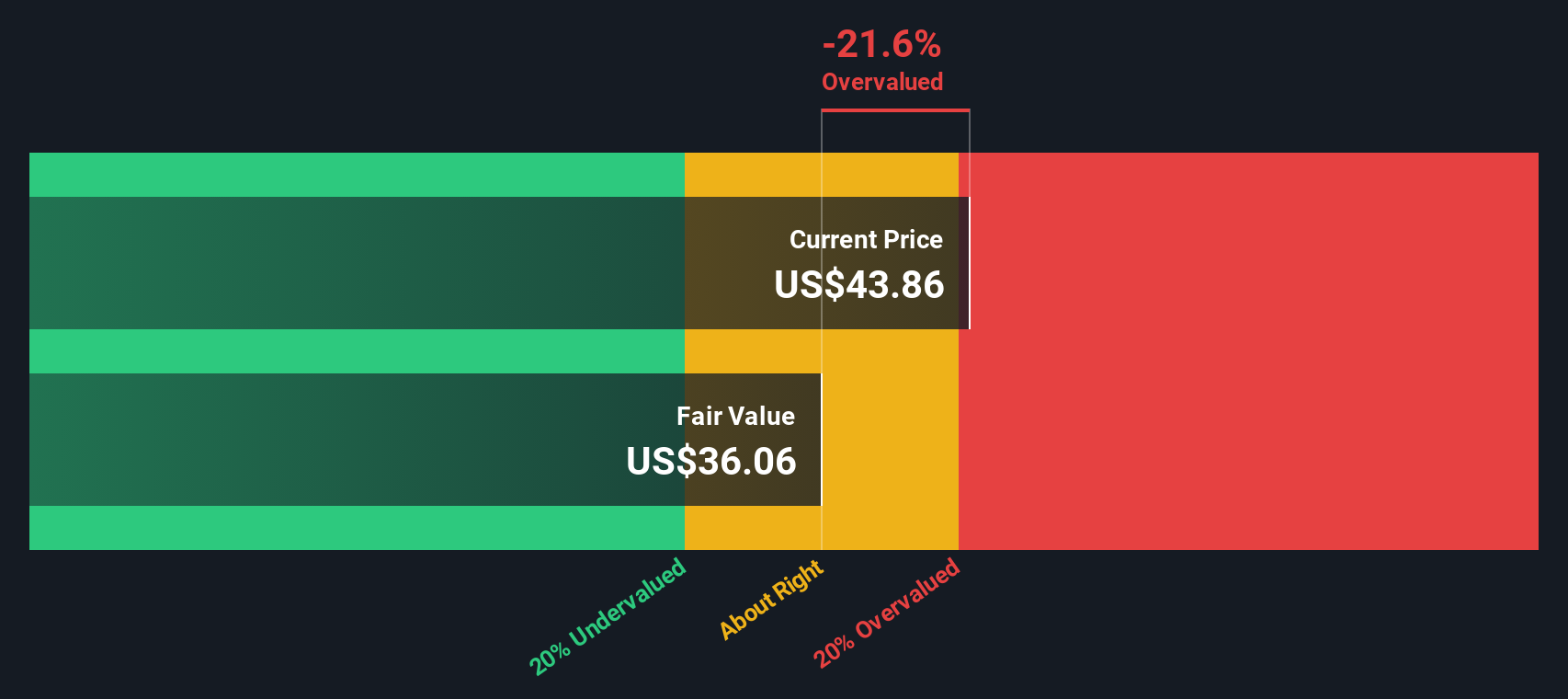

Our SWS DCF model paints a cooler picture, suggesting fair value nearer $36.06, which would make CWT look overvalued at today’s $43.96. If cash flows matter more than narrative assumptions, is the current price quietly baking in too much optimism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out California Water Service Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 915 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own California Water Service Group Narrative

If you would rather review the numbers yourself and challenge these assumptions, you can craft a tailored narrative in just a few minutes: Do it your way.

A great starting point for your California Water Service Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in fresh opportunities by using the Simply Wall Street Screener to spot compelling stocks that might otherwise slip past your radar.

- Capture potential bargains with strong cash flow upside by reviewing these 915 undervalued stocks based on cash flows that stand out on valuation alone.

- Ride innovation trends by targeting these 24 AI penny stocks positioned at the intersection of automation, data, and long term growth.

- Boost your income stream by focusing on these 13 dividend stocks with yields > 3% that can strengthen total returns through steady payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CWT

California Water Service Group

Through its subsidiaries, provides water utility and other related services in California, Washington, New Mexico, Hawaii, and Texas.

Average dividend payer and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion