Advertisement

- United States

- /

- Gas Utilities

- /

- NYSE:BIPC

Brookfield Infrastructure (NYSE:BIPC) Is Paying Out A Larger Dividend Than Last Year

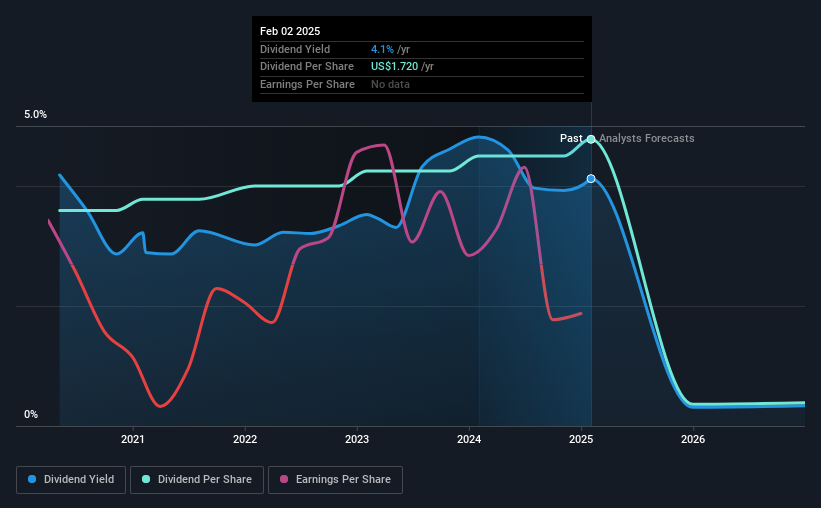

Brookfield Infrastructure Corporation (NYSE:BIPC) has announced that it will be increasing its dividend from last year's comparable payment on the 31st of March to $0.43. Based on this payment, the dividend yield for the company will be 4.1%, which is fairly typical for the industry.

View our latest analysis for Brookfield Infrastructure

Brookfield Infrastructure's Distributions May Be Difficult To Sustain

We aren't too impressed by dividend yields unless they can be sustained over time. Even though Brookfield Infrastructure isn't generating a profit, it is generating healthy free cash flows that easily cover the dividend. We generally think that cash flow is more important than accounting measures of profit, so we are fairly comfortable with the dividend at this level.

Assuming the trend of the last few years continues, EPS will grow by 32.5% over the next 12 months. We like to see the company moving towards profitability, but this probably won't be enough for it to post positive net income this year. The healthy cash flows are definitely as good sign, though so we wouldn't panic just yet, especially with the earnings growing.

Brookfield Infrastructure Is Still Building Its Track Record

It is great to see that Brookfield Infrastructure has been paying a stable dividend for a number of years now, however we want to be a bit cautious about whether this will remain true through a full economic cycle. The dividend has gone from an annual total of $1.29 in 2020 to the most recent total annual payment of $1.72. This works out to be a compound annual growth rate (CAGR) of approximately 5.9% a year over that time. The dividend has been growing as a reasonable rate, which we like. However, investors will probably want to see a longer track record before they consider Brookfield Infrastructure to be a consistent dividend paying stock.

The Company Could Face Some Challenges Growing The Dividend

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. We are encouraged to see that Brookfield Infrastructure has grown earnings per share at 32% per year over the past five years. While the company is not yet turning a profit, it is growing at a good rate. If this trajectory continues and the company can turn a profit soon, it could bode well for the dividend going forward.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. To that end, Brookfield Infrastructure has 2 warning signs (and 1 which is significant) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Brookfield Infrastructure might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:BIPC

Brookfield Infrastructure

Owns and operates utility investments in Brazil, the United Kingdom, and internationally.

Slightly overvalued with very low risk.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

38 followersusers have followed this narrative

6 commentsusers have commented on this narrative

10 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative