- United States

- /

- Logistics

- /

- NYSE:ZTO

Will Upgraded EPS Forecasts And Efficiency Gains Change ZTO Express (Cayman)'s (ZTO) Narrative?

Reviewed by Sasha Jovanovic

- Brokers have recently lifted their earnings-per-share estimates for ZTO Express (Cayman) by more than 6% for both the current year and 2026, citing strong operational efficiency, solid liquidity, and healthy parcel volume growth in its core express delivery services business.

- This combination of upgraded profit expectations and improving productivity highlights how ZTO’s focus on efficiency and parcel mix quality is reinforcing confidence in its longer-term earnings power.

- Next, we’ll explore how these upward earnings revisions, underpinned by stronger express delivery revenue expectations, could shape ZTO Express’s broader investment narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

ZTO Express (Cayman) Investment Narrative Recap

To own ZTO Express, you need to believe that its efficiency gains, parcel mix improvements, and self operated network can offset competitive and macro pressures in Chinese express delivery. The recent 6% uplift in earnings per share estimates supports the near term catalyst of margin resilience, but does not remove the key risk that prolonged price competition and slower parcel growth could still weigh on profitability.

In that context, ZTO’s latest Q3 2025 results, showing higher sales and a modest uptick in net income year on year, are especially relevant. They offer some support for the upgraded earnings outlook, yet also underline how sensitive profit growth remains to pricing, parcel volume trends, and the pay off from heavy automation and digitalization spending.

But investors should also be aware that if intense price competition persists and parcel growth slows, then...

Read the full narrative on ZTO Express (Cayman) (it's free!)

ZTO Express (Cayman)'s narrative projects CN¥60.4 billion revenue and CN¥11.6 billion earnings by 2028. This requires 9.3% yearly revenue growth and an earnings increase of about CN¥2.9 billion from CN¥8.7 billion today.

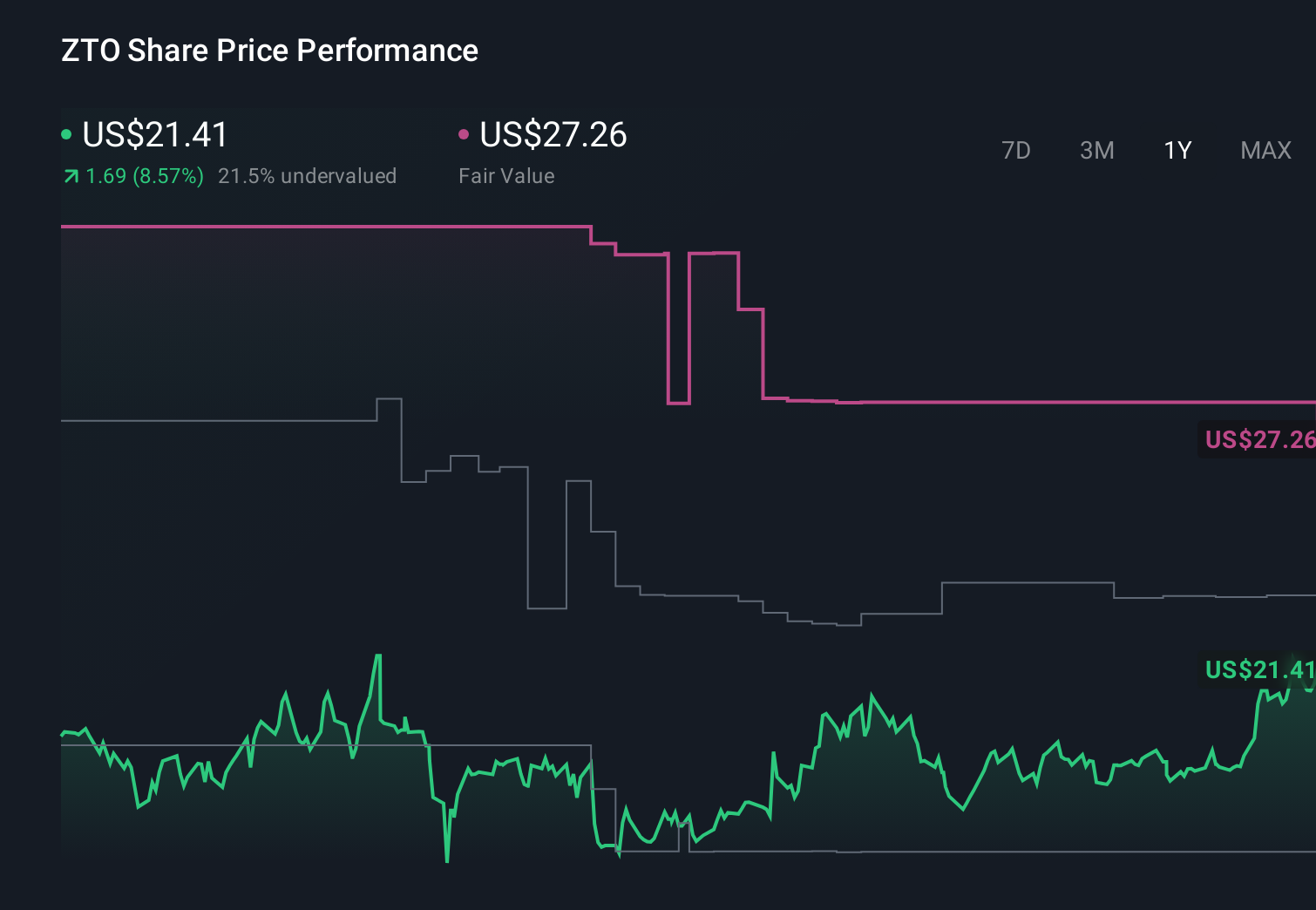

Uncover how ZTO Express (Cayman)'s forecasts yield a $23.29 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently value ZTO Express between US$20 and about US$44.67 per share, underscoring how far opinions can differ. You might weigh those views against the recent earnings estimate upgrades, which hinge on cost savings and parcel growth that could prove harder to sustain if industry price pressure lingers.

Explore 4 other fair value estimates on ZTO Express (Cayman) - why the stock might be worth over 2x more than the current price!

Build Your Own ZTO Express (Cayman) Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ZTO Express (Cayman) research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ZTO Express (Cayman) research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ZTO Express (Cayman)'s overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 13 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if ZTO Express (Cayman) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ZTO

ZTO Express (Cayman)

Provides express delivery and other value-added logistics services in the People's Republic of China.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion